Fresh Blow to Hedge Funds as Software Darlings Start to Crumble

Fresh Blow to Hedge Funds as Software Darlings Start to Crumble

(Bloomberg) -- A favorite strategy of hedge funds that splits technology stocks into hardware and software makers has been sputtering for months. It finally blew up.

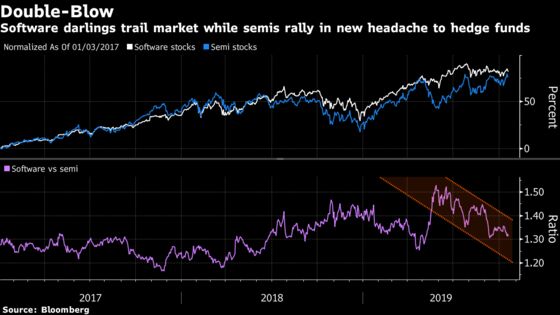

The smart money piled into software shares such as Microsoft and Atlassian while cutting stakes in the likes of AMD and Intel for almost two years. The split created a dichotomy in exposure not seen since at least 2010, according to primary brokerage data from Morgan Stanley. Avoiding chips has burned fund managers since January as the group rallied 38%. And now, the outsize bet on software firms has stopped working, with some erstwhile high-flyers mired in declines exceeding 20%.

The downturn in software stocks, particularly those focused on areas with high growth potential like the cloud or workplace productivity, is part of a trend that’s seen investors grow reluctant to pay high valuations for companies that aren’t yet profitable. The bet against chipmakers was partly predicated on their being in the crosshairs of the trade war with China, though they’ve rallied virtually all year.

“It’s a difference between buying an old-economy kind of stock and something newer,” Michael Vogelzang, chief investment strategist at Captrust Financial in Boston, said by phone. “Hedge funds tend to have shorter time frame than most long-only managers. They look at sector growth and say, ‘let’s make sure we buy something that’s going to grow, as opposed to something that could get cyclically smoked.”’

The rally in software stocks came to a stop as WeWork withdrew its initial initial public offering, shifting investor focus on valuations and profitability. A Goldman Sachs index tracking the industry’s fast-growing yet richly valued shares last month dropped the most on record, halting a surge that amounted to eight times the market’s gain during the previous two years.

The gauge slumped more than 10% this week as a pair of investor events hosted by Workday Inc. and Zoom Video Communications Inc. reignited concerns about growth and valuations while Atlassian’s results failed to sooth valuation concerns.

“The combination of high multiples and somewhat tepid comments like we saw recently with Workday is causing the group to show a little cracking in the armor,” said Mark Lehmann, president of JMP Securities. “The question going into the quarter is if they can keep their growth intact.”

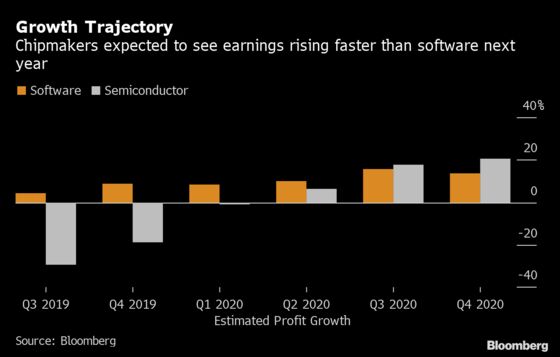

At first glance, the surge in chipmakers seems to make little fundamental sense. With the reporting season under way, the superiority in software’s earnings power is hard to miss.

Dragged down by trade uncertainty and sagging demand from electronics manufacturers and data center owners, profits from chipmakers in the S&P 500 are expected to fall 29% in the third quarter. By contrast, software companies will probably report an increase of 4.5%, analyst estimates compiled by Bloomberg showed.

Digging a little deeper and one can see the forecast trajectory of growth shifts in favor of semi bulls. The third quarter likely marked a bottom of the industry’s down cycle, with profits seen starting to rise six months from now. Growth will then continue to accelerate. By the third quarter of 2020, semi earnings are expected to expand faster than software.

Amid the backdrop, hedge funds remained skeptical on semis, with net exposure sitting at 15th percentile since 2010, Morgan Stanley data showed. While they sold software stocks in September, their positioning still hovered near the highest level over the stretch.

“The key is going to be earnings,” said Michael Gibbs, director of portfolio and technical strategy at Raymond James. “When the key companies in the software space report, you’re either going to see validation of this trade if the numbers are weak or you’re going to see a regression to the mean.”

--With assistance from Melissa Karsh.

To contact the reporters on this story: Lu Wang in New York at lwang8@bloomberg.net;Jeran Wittenstein in San Francisco at jwittenstei1@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Jeremy Herron, Dave Liedtka

©2019 Bloomberg L.P.