French Stock Market Renaissance Not Yet in the Bag

French Stock Market Renaissance Not Yet in the Bag

(Bloomberg) --

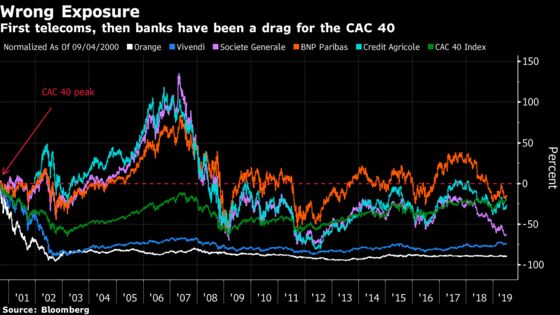

The last time French stocks hit a record high, Jacques Chirac was president, the Concorde’s future was in serious doubt after a crash near Charles de Gaulle Airport, and the country’s economy was growing at around 4%, a level not seen since.

While the CAC 40 Index still needs to gain 23% to surpass its all-time peak set in 2000, in the waning days of the internet bubble, the benchmark is closing in on a 12-year high, driven by stellar performances this year from luxury titan LVMH and planemaker Airbus, both up nearly 50%.

After outpacing the DAX, the FTSE 100, the IBEX and the FTSE MIB over the past 12 months, the CAC is back in fashion, in part because the index is more diverse than it used to be, with strong companies in several industries, says Matteo Brancolini, a fund manager at BPER Banca in Milan. LVMH, drinks maker Pernod Ricard, which this week touched a record high, and cosmetics giant L’Oreal are among the CAC 40 stocks that Brancolini says are “sexy.”

The French index took a hit when the Internet bubble burst, and companies such as Orange and Vivendi never really recovered. Then came the financial crisis, which hammered France’s banks. That’s another sector that is still struggling. In early July 2007, before the U.S. subprime storm, the sector, banks and insurers accounted for about 21% of the CAC’s weight, making finance the biggest sector. Today it accounts for only about 10%, while the industrial and consumer discretionary sectors each represent about a fifth of the CAC now.

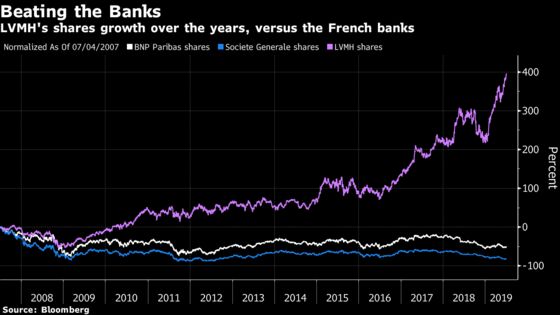

Since the beginning of 2008, Societe Generale shares have lost three quarters of their value while LVMH has quintupled. SocGen had a bigger market value than LVMH before the crisis; now, LVMH at 193 billion euros is 10 times larger.

“The banks’ weight on the index became bigger and bigger and then collapsed with the financial crisis,” Cedric Ozazman, head of investment and portfolio management at Reyl & Cie. in Geneva. “That’s the main reason for the CAC’s underperformance.”

Luxury has become the index’s biggest growth engine. Their growing weight in France’s equity benchmark has paid off in the past year as luxury-goods makers showed resilience amid global trade tensions. However, the CAC could quickly lose its glitter again if economic growth further slows in China, or if Hong Kong’s political turmoil lasts. Both are major markets for the sector.

But this year’s 19% gain in the CAC also reflects good breadth, according to Brancolini. Besides Airbus and LVMH, top gainers include technology consultant Atos, software maker Dassault Systemes and industrial companies Legrand and Schneider Electric.

“France has cool stocks and the CAC 40 is the most ‘beautiful’ index in Europe,” Brancolini says. “While Germany’s DAX is full of cyclicals and industrials, which are slowing down, and Italy’s FTSE MIB has many banks, the CAC is a well balanced index, with everything from luxury and utilities to pharma, industrials, food and banks too.”

The index’s developments mirror a wider dynamic between local players, which lost ground over the years, and global companies like LVMH and L’Oreal, which have been able to rely on the demographic trends in regions such as China and the U.S. for growth, Ozazman says.

BNP Paribas and Societe Generale may have a presence in the U.S. and other countries but their performance is still strongly linked to France, where economic growth is slower, he says.

Now, with the CAC around 5,621, traders are watching the 2018 peak of 5,640. A move above that level would put the index at the highest since late 2007, before the crisis hit fully. The all-time closing high of 6,922.33 from 2000 still seems like a long way off.

Of course, looking only at the CAC’s price change doesn’t tell the whole story for investors. Including dividends, the index has returned 47% since the peak. That works out to about 2.1% a year.

In the meantime, Euro Stoxx 50 futures are trading little changed ahead of the open.

- Watch chipmakers after Samsung reported its profit halved in the June quarter as an industry downturn and trade tensions hit demand for chips and smartphones. Watch Samsung suppliers including STMicroelectronics, Siltronic, ASML, Aixtron, Infineon and Dialog Semi.

- Watch miners and steelmakers after the iron ore price, which has rocketed in 2019, slumped after the top Chinese steel industry group called for a probe into the rally for the material. Watch miners with high exposure to iron ore, including Rio Tinto, BHP, Anglo American and Ferrexpo and watch for any impact in the steelmaking sector, including ArcelorMittal, Voestalpine and Evraz.

- Watch impact from plummeting bond yields German bund yields sank below the European Central Bank’s deposit rate for the first time on Thursday, a development likely to drive investors yet further into the realm of riskier debt from the likes of Italy and Greece, plus plenty of emerging market assets.

- Watch the pound and U.K. stocks as the future of the union of the United Kingdom is becoming a key battleground for the candidates aiming to be the next prime minister.

COMMENT:

- “(We) forecast a 3% gain in global equities to mid-2020,” Citi strategists write in note. “A sharp global economic slowdown remains the biggest risk to our optimistic view. We think this bull market will continue to narrow into U.S. equities, where we remain overweight. The U.K., where Brexit fears look overdone, is now our favorite value trade. Our global sector strategy has a mild cyclical/growth tilt.”

COMPANY NEWS AND M&A:

- Deutsche Bank U.S. Job Cuts May Go Deeper Than Equities, Rates

- Deutsche Bank Cuts Seen Sparing Jobs in ‘Integral’ Nordic Region

- Osram Boards Accept $3.8 Billion Offer From Bain and Carlyle

- IAG Reported to Plan New Norwegian Air Bid Within Two Weeks

- Germany’s FinTech Group Weighs Options Including Potential Sale

- Orange CEO’s Future Hangs in the Balance as Fraud Verdict Looms

- SocGen Is Said to Plan Sale of U.K. Private Banking Business (1)

- France’s Vial: Not Aware of Fresh Talks on Renault-Fiat

- Deutsche Post to Lift Letter Prices for Corporate Customers: FAZ

- Aroundtown Acquires EU900m Properties in Germany, Benelux

- Brookfield, Endesa Are Said to Weigh Bids for EDP Hydro Assets

- Shell Has Entered Japan’s Retail Electricity Market, Nikkei Says

- Bosch Is Said to Near $1B Sale of Packaging Unit to CVC

NOTES FROM THE SELL SIDE:

- Peel Hunt recommends buying Ocado and selling Just Eat, as the lines between takeaway and grocery delivery are blurring. Ocado is a technology company now and should be treated as such, while Just Eat could face new “pain point” in 1H results on higher marketing costs.

- Tullow Oil is seen having attractive risk/reward upside, Jefferies says in note, upgrading the stock to buy from hold while maintaining its 245p price target.

- Peel Hunt cuts Victrex to hold from add due to a weaker economic environment, notably in Germany, saying it could trim the thermoplastic maker’s pretax profit this year and next by 5%.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 397.9 (May 2018 high); 403.7 (2018 high)

- Support at 392.7 (July 2018 high); 385.7 (76.4% Fibo)

- RSI: 71.2

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,596 (May 2018 high); 3,687 (2018 high)

- Support at 3,519 (76.4% Fibo); 3,412 (50-DMA)

- RSI: 73.1

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Aareal Bank upgraded to hold at Kepler Cheuvreux; PT 25.50 Euros

- DSM upgraded to overweight at JPMorgan; PT 120 Euros

- Dufry upgraded to neutral at Goldman; Price Target 87 Francs

- Hoist Finance upgraded to buy at SEB Equities; PT 53 Kronor

- Iliad upgraded to hold at Kepler Cheuvreux; PT 105 Euros

- Nemetschek upgraded to neutral at Oddo BHF; PT 51 Euros

- Osram upgraded to hold at LBBW; PT 35 Euros

- Takkt upgraded to buy at Kepler Cheuvreux; PT 17 Euros

- Tullow upgraded to buy at Jefferies; Price Target 2.45 Pounds

- Wood upgraded to buy at Berenberg

DOWNGRADES:

- JM downgraded to sell at DNB Markets; PT 200 Kronor

- Victrex downgraded to hold at Peel Hunt

INITIATIONS:

- Ambea rated new buy at Handelsbanken; PT 75 Kronor

- Humana rated new hold at Handelsbanken; PT 62 Kronor

MARKETS:

- MSCI Asia Pacific up 0.3%, Nikkei 225 up 0.1%

- Euro down 0.04% at $1.128

- Dollar Index up 0.01% at 96.78

- Yen down 0.06% at 107.88

- Brent down 0% at $63.3/bbl, WTI down 1% to $56.8/bbl

- LME 3m Copper down 0.2% at $5906/MT

- Gold spot little changed at $1416.4/oz

- US 10Yr yield down 1bps at 1.94%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) May Current Account Balance, prior -800m

- 8:45am: (FR) May Trade Balance, est. -4.85b, prior -4.98b

- 9am: (SP) May Industrial Output SA YoY, est. 0.55%, prior 1.7%

- 9am: (SP) May Industrial Output NSA YoY, prior -2.0%

- 9am: (SP) May Industrial Production MoM, est. -0.5%, prior 1.77%

- 9:30am: (UK) June Halifax House Price 3Mths/Year, est. 5.7%, prior 5.2%

- 9:30am: (UK) June Halifax House Prices MoM, est. -0.4%, prior 0.5%

- 10:30am: (UK) 1Q Unit Labor Costs YoY, prior 3.1%

- 11am: (IT) Istat Releases the Monthly Economic Note

* For a daily wrap on developments in European equity capital markets, click here

--With assistance from Michael Msika.

To contact the reporter on this story: Albertina Torsoli in Geneva at atorsoli@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Phil Serafino

©2019 Bloomberg L.P.