Foreign Investors Dream of a World With China Bond Futures

Foreign fund managers want access to more hedging products.

(Bloomberg) -- Foreign fund managers are pretty clear about what they want now that China’s bonds are joining a key global index: a better way to manage risk.

While hedging products like interest rate swaps are available to some overseas firms through the onshore interbank market, most instruments either aren’t accessible to foreigners or are rarely traded. The dearth of hedging tools is a deterrent for many global pension funds, insurers or banks that need them to manage risk when they take positions.

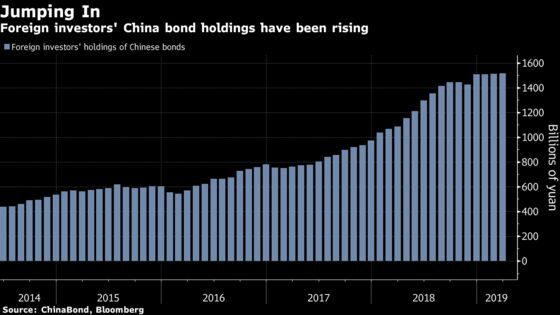

Some $100 billion is expected to flow into the world’s third-largest bond market in the year after China’s sovereign and policy-bank notes joined the Bloomberg Barclays Global Aggregate Index. Most onshore bonds are currently bought and held by banks, rather than traded in a liquid secondary market. Developing a better hedging market onshore is one way of addressing that issue.

Opening access to the existing onshore government bond futures market would be ideal, fund managers said, though it’s unclear whether they’ll get their wish any time soon. Contracts on 5-year and 10-year sovereign notes are among the most liquid hedges, with 910 billion yuan ($136 billion) traded in March. Bond futures were launched less than six years ago and remain unavailable to foreign investors and domestic commercial banks. Trading is limited to securities firms and futures companies.

“If there’s one instrument that we would like the regulators to open up for foreigners as soon as possible, that would be the bond futures because they’re the cheapest and most efficient hedge,” said Edmund Goh, an Asia fixed-income fund manager at Aberdeen Standard Investments in Shanghai.

The yield on China’s 10-year government bond was little changed at 3.39 percent, near the highest level since November, after first-quarter economic data exceeded analyst estimates.

Here’s what fund managers say they need to manage risk as they buy China’s bonds:

AMP Capital Investors Ltd. (Nader Naeimi)

- There are challenges like the lack of liquidity, lack of a liquid derivatives market; the lack of hedging ability makes it hard for us to allocate significantly

- The toolkit to manage interest rate risks is also limited

- As a start for a macro investor, futures will be the most useful tool. Onshore is preferred, but HKEX will be a good start, as long as they track the onshore bonds. But ultimately, investors will want to go deeper into the onshore market

Fuh Hwa Securities Investment Trust Co. (Huang Yuanchun)

- The main demand for hedging tools will come from actively managed funds

- Overseas institutional investors definitely want to participate in the bond futures market to actively manage interest rate risks

- At the moment, there are few participants in the onshore IRS market. For overseas investors, it’s just not as convenient as hedging risks with bond futures would be

China Securities International (Gary Zhou)

- We would be more willing to participate in the onshore market if the access to products like derivatives and repos was liberalized

- Trading the cash bond market itself has comparably low returns, and investors usually use leverage to increase yields; that’s not convenient without interest rate swaps to manage related risks

- There’s still definitely a gap between non-deliverable IRS available in Hong Kong and interest rate hedging products in the domestic market; the participants, price trends and volatility are all different

--With assistance from Miaojung Lin, Qizi Sun and Tian Chen.

To contact the reporters on this story: Livia Yap in Singapore at lyap14@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Philip Glamann, Magdalene Fung

©2019 Bloomberg L.P.