For Two Huge Deals, Arbitrage Goes Out the Window

For Two Huge Deals, Arbitrage Goes Out the Window

(Bloomberg Opinion) -- T-Mobile US Inc., the wireless carrier, and drugmaker Bristol-Myers Squibb Co. have something in common: Investors are more interested in them than the companies they’re trying to acquire. That’s unusual as far as M&A goes and creates a conundrum for traders who bet on deals.

T-Mobile is awaiting regulatory approval for its controversial $59 billion takeover of smaller rival Sprint Corp. to grab hold of its wireless spectrum and millions of customers. Bristol-Myers agreed last month to buy Celgene Corp. for about $88 billion to gain a blood-cancer treatment and other drugs in development. (Both totals include net debt.) They’re two of the largest and most closely watched transactions of the year, and if completed will create ripple effects throughout their respective industries.

Normally when a takeover is announced, investors pile into shares of the target company. That’s the one at the center of the deal excitement and whose stock price will theoretically rise as its shareholders get closer to receiving their payment. Risk arbitrageurs take it a step further by shorting the acquirer’s stock to hedge out general market risk that could affect both companies during the time it takes for the merger to close (such as the late December sell-off in the U.S.). But some are afraid to bet against shares of T-Mobile or Bristol-Myers — or get stuck holding Sprint’s.

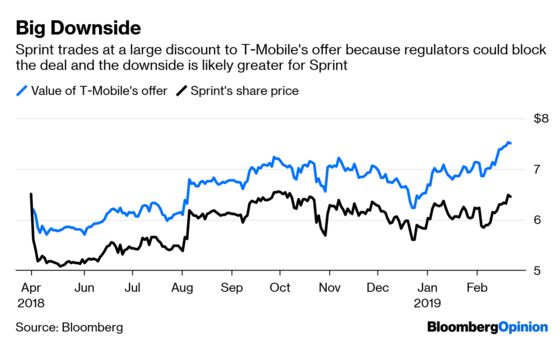

T-Mobile’s growing business is far more attractive than that of the financially less healthy Sprint. Without the merger, Sprint would most certainly struggle, but T-Mobile would probably be fine on its own. A stand-alone T-Mobile could even get scooped up by another acquirer.

The Sprint deal is also fraught with regulatory issues. As I’ve written before, not only would it reduce the number of major national wireless carriers from four to three, it would also leave T-Mobile with a tremendous lead in the prepaid market. Prepaid service is most commonly used by lower-income Americans, and so competitive pricing is crucial. There’s a significant chance that government officials will block the transaction, which would send Sprint’s stock into a downward spiral.

“We like T-Mobile better as a stand-alone,” Roy Behren, co-portfolio manager of the $3 billion Merger Fund at Westchester Capital Management, said in a phone interview. He thinks the odds of a deal are long.

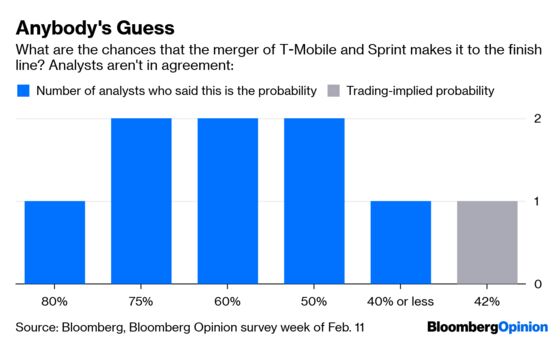

Behren’s not alone. On Friday, Sprint shares traded at a 14 percent discount to the value of T-Mobile’s all-stock offer, signaling trader apprehension. The spread implies a less than 50 percent probability of the merger being completed. Earlier this month I surveyed equity analysts about where they see the odds. Eight who have varied recommendations on the two stocks responded, and while they were generally more optimistic than the trading probability, their predictions varied widely:

In the case of Bristol-Myers, there’s unfounded speculation that the company could become a takeover target itself, derailing its purchase of Celgene. Fueling some of that is the sudden involvement of activist hedge fund Starboard Value, which this week nominated five directors to the Bristol-Myers board. While Starboard has had some activist victories in the past, it’s unclear what value it brings to the esoteric business of developing drugs. And after years of megamergers sweeping through the pharma industry, why would Bristol-Myers attract bids only now? My colleague Max Nisen has also explained why the Celgene deal suits Bristol-Myers, eye-popping price and all.

Nevertheless, “people are nervous about being short Bristol,” Behren said. For those who see the deal going through, though, it’s a welcome wide spread to trade — meaning there’s a large gap between the takeover offer value and the seller’s stock price, which can produce a robust return. Risk-arb investors have been grappling for years with narrow merger spreads, he said, meaning the opportunity to make money seizes up almost immediately when a deal is announced. I wrote about this phenomenon in 2013, and it’s still going on.

They don’t call it risk for nothing. But scanning the list of Big Pharma CEOs, I’m not convinced any will move to break up Bristol-Myers’s deal by launching a bid for the $83 billion giant. And as for Sprint, just keep the Pepto-Bismol handy.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.