Fixed-Income ETFs Are Trapped in Bond Market’s Liquidity Crunch

Fixed-Income ETFs Are Trapped in Bond Market’s Liquidity Crunch

(Bloomberg) -- As fixed-income markets buckle under wild swings and scarce liquidity, the strain is starting to show in bond exchange-traded funds.

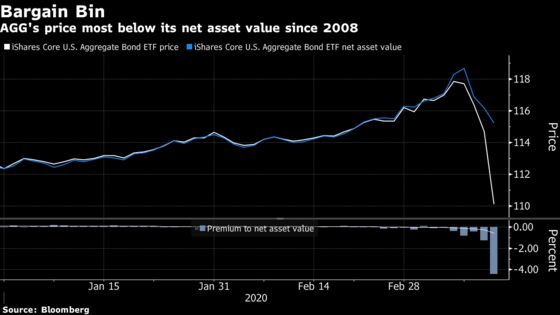

Cash prices in some of the most actively traded bond funds are now at steep discounts to the value of their underlying assets. The largest debt ETF -- the $74 billion iShares Core U.S. Aggregate Bond fund -- closed at a 4.4% discount to its net asset value on March 12, the largest divergence since 2008, according to data compiled by Bloomberg. Meanwhile, the $31 billion iShares iBoxx $ Investment Grade Corporate Bond ETF’s price fell 5% below its net-asset value on Thursday, also the largest discount since 2008.

The havoc is reigniting arguments around fixed-income ETFs, which trade much more liquidly than the assets they hold. Critics have long warned the products were a pressure point that would crack in volatile times, as investors rush to redeem their holdings during a sell-off. But just as many arguments exist that ETFs give participants in less-active markets better prices in times of stress -- and an exit route.

“The ETF at least gives you some way to get out if you need to. you’re going to pay up for it, but if you have to get out, at least there’s liquidity somewhere,” said Eric Balchunas, senior ETF analyst at Bloomberg Intelligence. “The distance between the ETF and the NAV provides a great measure of the liquidity in the underlying market.”

Rampant turbulence across bonds markets is souring appetite for the arbitrage opportunity that normally keeps ETF prices in lockstep with a fund’s value. Normally, middlemen known as authorized participants will buy shares of a falling ETF in order to exchange for the underlying bonds with the fund’s issuer. That market maker will then sell those securities to pocket a virtually risk-free profit. The ETF’s price usually snaps back to the fund’s net-asset value as the supply of ETF shares is reduced.

But fear over the coronavirus’s economic fallout has unleashed historical volatility in fixed income, making it harder to unload the underlying bonds. As a result, the ETFs are trading at persistent discounts as thin liquidity sidelines market makers.

“If the authorized participants felt that they could buy an ETF at a 15% discount and then turn around and sell those components to the cash market 15% higher, they would,” said David Schawel, chief investment officer at Family Management Corp. “But clearly they feel like there’s not enough activity in the cash market, therefore they can’t do that.”

The carnage is notable across the risk spectrum. A combined $14.4 billion exited from investment credit, high yield and leveraged loan funds this week, the largest withdrawal on record. And even Treasuries -- regarded as the ultimate safe haven asset -- have suffered this week as investors sold their most liquid securities in order to raise cash.

The stress in fixed-income ETFs is a stark contrast to the landscape in equities, where the sell-off has been rather orderly. The price of the $227 billion SPDR S&P 500 ETF Trust -- the largest ETF -- dropped just 0.13% below its net-asset value on March 12. The second-biggest ETF, the $164 billion iShares Core S&P 500 fund, ended Thursday with just a 0.14% discount.

And the cracks are widening. The $3.6 billion VanEck Vectors High Yield Municipal Index fund’s price fell a record 19% below its net-asset value on Thursday, the largest discount in the $4.4 trillion ETF market. And even the early success stories are starting to feel the strain. The iShares iBoxx High Yield Corporate Bond ETF’s price has dropped over 1% below its net-asset value, after ending Monday with a modest half a percentage point discount amid its worst day since 2009.

Some are spying opportunity as fixed-income ETFs become further ensnared in the bond market’s liquidity crunch. The rapid plunge in prices creates a “unique” entry point for funds trading at a discount, according to Schawel, who pointed to investment-grade corporate bond ETFs as an example.

“There’s a leap of faith if you think that you’re buying a discount because the cash markets aren’t functioning very well,” Schawel said. “If these are assets that you’re wanting to own anyway, then I think it’s a very unique opportunity to buy things at an even greater discount.”

To contact the reporter on this story: Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Rita Nazareth, Chris Nagi

©2020 Bloomberg L.P.