Fed's Pivot Kills Yield-Curve Inversion Risk for Pimco, Vanguard

Fed's Pivot Kills Yield-Curve Inversion Risk for Pimco, Vanguard

(Bloomberg) -- The overseers of about $10 trillion say it’s finally time for markets to move the risk of an inverted U.S. yield curve off their radar.

For more than a year, professional money managers -- and even some individual investors -- have focused on the prospect of short-end rates lurching above their long-term counterparts, and the recessionary signal that would send. Now, firms such as Pacific Investment Management Co. and Vanguard Group Inc. say the Federal Reserve’s pivot to pausing its tightening cycle has upended the flattening trade. These investors expect the curve to move sideways and then steepen in earnest.

The spread between 2- and 10-year rates -- the most closely watched section of the curve -- dwindled to 9 basis points in December (the day after the Fed last lifted rates and projected more hikes in 2019). That was the narrowest since 2007, which was also the last time the gap was negative. It’s gone sideways since, and is currently about 17 basis points.

“We are out of the danger zone in terms of the curve, because at this point the Fed has fully pivoted and no longer committed to anything,” said Jurrien Timmer, director of global macro at Fidelity Investments, which has $2.4 trillion under management. He doesn’t foresee inversion or a U.S. recession ahead.

The Fed signaled in January that it’s done raising rates for a while. Chairman Jerome Powell on Wednesday said the U.S. economy is “in a good place.” In his media briefing after last month’s meeting, he cited headwinds to U.S. growth, such as slowing output in China and Europe, Brexit, trade negotiations and the effects of the U.S. government shutdown.

On Thursday, the Bank of England warned that the impact on the economy from Brexit has increased as it cut its growth forecast.

History as Guide

The curve usually slopes upward as investors typically demand higher returns for locking up money for longer. Six decades of market history show that when it inverts a recession has eventually followed.

Granted, some shorter-maturity slices of the curve, specifically the gap between 2- and 3-year yields and their 5-year counterpart, have already inverted. But most market observers don’t see that segment as having the predictive powers of the 2- to 10-year spread.

“The risk-reward now is for moderately higher rates and a steeper curve,” said Mark Kiesel, chief investment officer of global credit at Pimco, which oversees $1.66 trillion. He holds that view even as he still sees the Fed lifting rates again, in the second half of 2019.

“The main driver is that you will see the Fed be patient and continued deficits, which is going to get more investors to start to price in credit-risk premium,” he said. “We also think the risk is for inflation to surprise a little bit on the upside.”

Yield Pressures

Even as the deteriorating federal deficit and the Fed’s balance-sheet run-off led the Treasury to double net issuance in 2018 to $1.34 trillion -- around what Wall Street expects again this year --- the government hasn’t had to pay up much via higher yields.

That won’t last, says Kiesel, in part as greater currency-hedging costs and the prospect of a weaker dollar will dim foreign demand.

The 10-year yield will swing from 2.5 percent to 3.25 percent for the time being, Kiesel said. At 3.25 percent, he said he’d look to buy, while wagering against it at a 2.5 percent yield. It was last at around 2.67 percent.

“This Fed pause substantially reduces the risk of curve inversion, at least for the first half of this year,” said Evan Brown, head of macro asset-allocation strategy at UBS Asset Management, which oversees $781 billion. “You usually see an inversion when the market thinks the Fed has gone too far. The Fed’s pause and outlook that they are going to be patient suggests they are not going too far too fast.”

Hike Recipe

Not everyone says the inversion risk is gone. BMO Capital Markets strategists, among the first to call the flattening trend, say a move below zero could still happen -- though only if the Fed hikes again. Futures show traders see little chance of a rate hike this year.

“The FOMC removed any directional forward guidance,” said BMO’s Jon Hill. “Still, all else equal, the unemployment rate is below neutral, growth is above potential; and if these things continue and inflation stays around 2 percent it’s reasonable to expect another hike.”

The Fed has raised rates nine times since December 2015. It started allowing debt on its balance sheet to roll off in October 2017 according to a schedule it laid out. Last month, policy makers said they’re open to taking a more flexible approach to reducing the portfolio.

“If the Fed is on perma-pause, or they signal that they maybe have one or maybe two more hikes and are close to being done, what will typically happen is the curve begins to trend sideways,” said Gemma Wright-Casparius, a senior money manager at Vanguard, which manages $4.9 trillion. “And if you look at previous cycles it then begins to steepen. Over time, the yield curve could be steeper.”

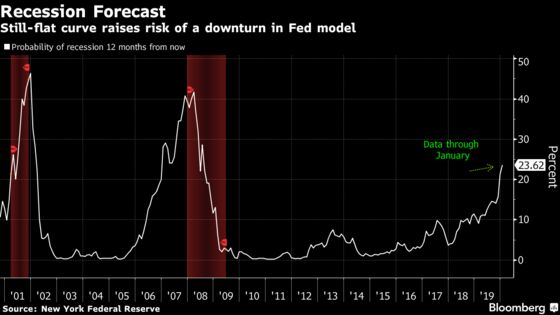

Wright-Casparius considers curve inversion unlikely. But she does see the risk of a recession in about a year, given that some Fed models show a growing probability of a downturn.

Dan Fuss, vice chairman of Loomis Sayles & Co., with about $250 billion in assets, says the curve will move to the back burner for a while as it trends sideways. And he doesn’t expect it to invert with the Fed on hold.

“The curve didn’t get all the way flat, but you certainly can’t go skiing on that slope,” Fuss said.

--With assistance from Alex Tanzi.

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Vivien Lou Chen

©2019 Bloomberg L.P.