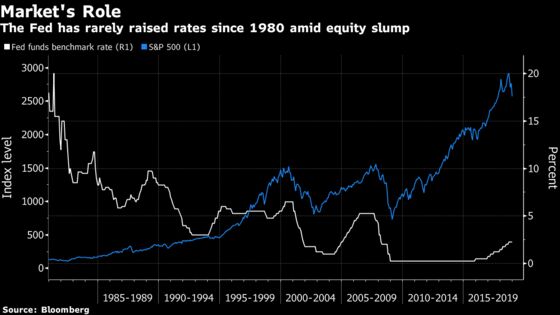

Fed Rate Hikes Are Extremely Rare When Stocks Are This Beat Up

While half the S&P 500 sits in a bear market and groups like banks and transports tumble day after day.

(Bloomberg) -- Donald Trump’s hectoring aside, it’s exceedingly rare the Federal Reserve raises interest rates when stocks are behaving this badly.

In fact, were policy makers to follow through with their widely expected hike Wednesday, it would be the first time since 1994 they tightened in this brutal a market. Right now, the S&P 500 is down over the last three, six and 12 months, a backdrop that has accompanied just two of 76 rate increases since 1980.

There’s no guidebook on how stocks should behave after a decade of easy money and an unprecedented run-up in equities. But the statistic is another lens into the divide between markets and the economy, a split that has beguiled forecasters trying to draw connections between the two.

While half the S&P 500 sits in a bear market and groups like banks and transports tumble day after day, some key economic data bolster the case of hawks. It’s one reason investors will be fixated on commentary about financial or market stability, looking for signs that the latest volatility is catching the eye of Fed officials.

“This presents an interesting dilemma for the Fed,” said David Rosenberg, chief economist and strategist at at Gluskin Sheff + Associates Inc. “Financial markets are telling them ‘no mas,’ but the economic data suggest that further tightening remains appropriate.”

While the role of markets in the Fed’s policy calculus is endlessly debated, the fact is, since 1980, rate hikes have almost always come amid equity buoyancy. On average, the S&P 500 is up 4.1 percent, 6.9 percent and 11 percent over the previous three, six and 12 months when tightening occurs. The exception was in the 1970s, when the Fed ignored market turmoil to combat inflation that was running at 7 percent a year.

Of course, the economy looks nothing like that now. Consumer prices have stayed below 3 percent for the past six years and at a growth rate of 3.5 percent, it’s hard to frame gross domestic product as overheating. The opposite concern seems to be driving equities, with recession mentions getting more numerous in professional commentary.

Stocks buckled again Monday, with the S&P 500 dropping 2.1 percent to its lowest close since October 2017. Futures fluctuated on Tuesday, adding 0.2 percent as of 7:45 a.m. in London.

While a Fed report earlier this month said it viewed financial-stability concerns as moderate -- citing commercial real estate, corporate debt and leveraged loans among the potential issues -- the rout that’s erased $3 trillion from American equity values has many calling for a pause.

Could stocks be sending a message that the data has yet to reflect? Some strategists think so. They’re convinced eight rate increases in three years have been enough for an economy threatened by everything from U.S.-China trade spat to Brexit and a global growth slowdown.

The Fed is scheduled to announce its decision on Dec. 19 at the conclusion of its two-day meeting. All but two of the 89 economists surveyed by Bloomberg predicted a rate increase.

“The Fed needs to deliver on a more dovish stance to avoid disappointing financial markets,” said Mark Haefele, chief investment officer for UBS Global Wealth Management. “A rate increase looks likely. But signs of flexibility from the Fed have caused markets to scale back the expected pace of tightening in 2019.”

You don’t have to go back too far for a time when market histrionics seem to have weighed on policy. In December 2015, Janet Yellen pushed ahead with the first rate increase of the cycle just two months after the S&P 500’s worst drop in four years. Stocks summarily slid into a 10 percent correction and the Fed chair delayed more hikes for a year.

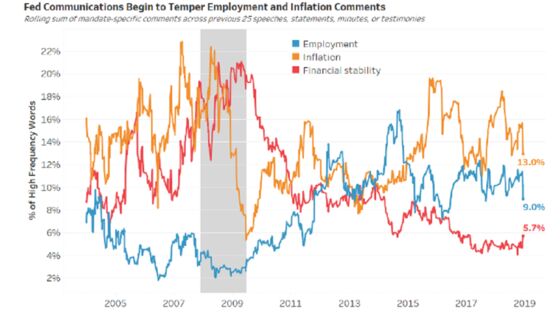

The latest equity sell-off has been bad enough for Fed officials to take notice. Mentions of “financial stability” have increased in Fed commentary to the year’s high of 5.7 percent while comments on inflation and employment dropped, according to data compiled by Bianco Research on speeches, statements, minutes or testimonies.

Last month, Fed chairman Jerome Powell dialed back his aggressive stance after his October remark on rates was blamed for the S&P 500’s worst month in seven years.

Still, the bloodletting in stocks probably hasn’t gotten to a pitch where the Fed would abandon tightening, according to Bank of America. That Powell went ahead with another increase right after the equity rout in February showed he’s less worried about financial markets than Yellen was in 2015, strategists led by Benjamin Bowler said.

“Partly this could be a difference in approach of the individuals and economic conditions,” the strategists wrote in a note. However, “With 200 basis points of rate hikes under the Fed’s belt today, they are in a better position and are more able to manage policy to the real economy (their job) rather than the market,” they said.

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, ;Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2018 Bloomberg L.P.