Fed ‘Put’ Lacks Key Ingredient Bulls Dare Not Ignore

Fed ‘Put’ Lacks Key Ingredient Bulls Dare Not Ignore

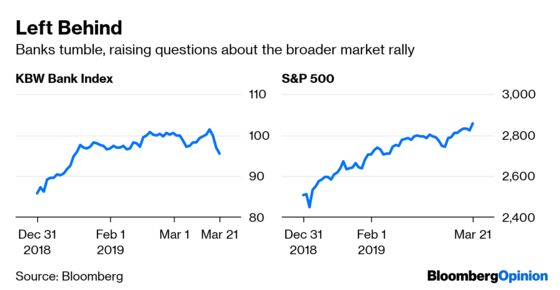

(Bloomberg Opinion) -- Just one day after the Federal Reserve said the economic outlook was such that it couldn't support even one interest-rate increase this year, the S&P 500 Index responded by setting a new high for the year. Clearly, investors were overjoyed with the prospect that the Fed had their backs. Maybe the party would have been less ebullient if anyone bothered to check in on the banks.

Rather than joining in the fun, the benchmark KBW Bank Index fell for a third straight day, closing at its lowest level since mid-January. Its decline Wednesday was the worst on the day of a Fed announcement since 2011. The concern here is that the Fed’s moves will only serve to suppress market rates, putting further pressure on the already razor-thin difference between the short-term rates banks pay on their own borrowings and the long-term rates they charge lenders. In the banking business, this is known as the net interest margin. With the trajectory for net interest margins set to get tougher, the "party’s over" for banks, Robert W. Baird & Co. senior research analyst David George wrote in a research note. “Bank valuations are tempting – especially relative to the broader market – but given higher odds that NIMs grind flat-to-lower into the end of the cycle, investors should remain disciplined with bank exposure,” George wrote.

This isn’t just a sector-specific issue: It’s almost impossible to have a healthy economy without a healthy banking system. That’s because a steepening yield curve and normalized rates give banks an incentive to lend rather than hoard deposits. And banks have been doing a lot of hoarding of cash. U.S. banks have about $2.83 trillion in surplus liquidity, little changed over the past five years and up from less than $500 million before the financial crisis, Fed data show. Just take a look at the trouble that banks in the European Union have been having as the European Central Bank has decided it’s best to keep rates at zero. Put another way, the banks may have just become the important sector in the global market for equities. For stock investors, that shouldn’t be a comforting thought.

DOLLAR’S DEATH EXAGGERATED

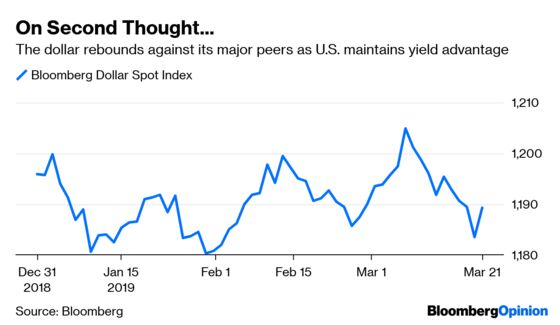

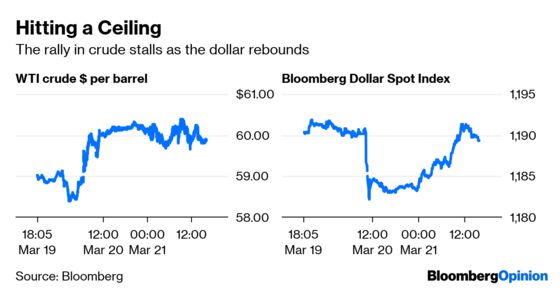

Fed Chairman Jerome Powell hadn’t even finished explaining at Wednesday’s press conference why no rate increases are warranted this year before many in the foreign-exchange market were declaring the death of the dollar. After all, without the prospect of higher rates any time soon and with the economy decelerating, why own the dollar? The Bloomberg Dollar Spot Index promptly fell 0.5 percent to its lowest since the start of February. But on Thursday, the gauge recovered all those losses and then some, rising as much as 0.68 percent. It seems there are plenty of reasons to like the greenback. For one, rates in the U.S. are still very attractive relative to what investors can get anywhere else, even with the big drop in U.S. Treasury yields. On average, Treasury yields are about 2 percentage points higher than the rest of the global government bond market, according to the ICE bond indexes. As recently as 2013, U.S. yields were lower than those found in almost any other government bond market. Also, the dollar is relatively attractive by default. The euro has no appeal after the European Central Bank said this month that it’s in no rush to raise its key rate from zero, rates are still negative in Japan, and the pound is too risky, given the political turmoil surrounding its planned exit from the European Union. “The dollar is still the most attractive currency in the G-10,” Bloomberg News quoted Daragh Maher, the U.S. head of FX strategy at HSBC Securities, as saying.

BOND MARKET MYSTERY

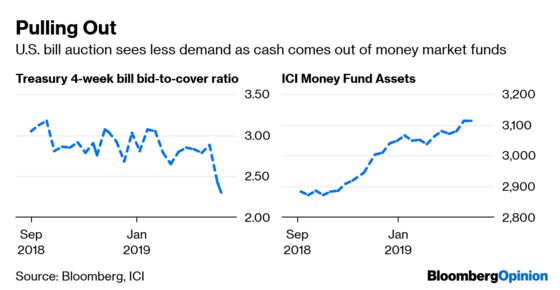

Would you rather lend money for four weeks at a rate of 2.47 percent or take on a lot more risk and lend money for 10 years at a rate that’s just a few basis points higher, at about 2.51 percent? This isn’t a trick question and the answer would seem to be obvious, but it seems many bond traders opted for the latter. That was seen in the Treasury Department’s auction Thursday of $60 billion of four- week bills. Investors submitted bids for just 2.30 times the amount offered, the lowest so-called bid-to-cover ratio since August 2007. Why the demand was so tepid for relatively high-yielding cash equivalents is hard to say. It may have something to do with the mechanics of the opaque world of money markets. Another explanation is that perhaps some of the cash that has been steadily building in money funds – which are prime buyers of Treasury bills – is being pulled out and put to work in equities and other riskier assets in the wake of the Fed’s surprisingly dovish turn. Money-fund assets stood at $3.06 trillion as of Wednesday, up from $2.88 trillion at the end of October, according to the Investment Company Institute. The build-up in money-fund assets during the last four months are the most since the period spanning the last three months of 2008 and January of 2009. Many-stock market bulls have pointed to this accumulation of cash as a potential source of demand for equities once investors got a clearer picture of the Fed’s intentions, which they got this week.

BRAZIL POLITICS STRIKE AGAIN

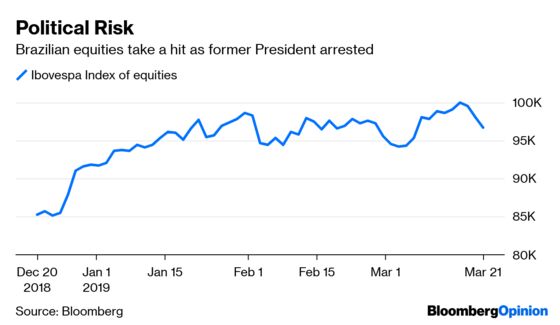

Brazil’s “Bolsonaro Boom” is starting to crack. Brazil’s Ibovespa index of stocks surged about 40 percent between mid-June and the end of January as new president and populist Jair Bolsonaro brought big plans for reform. But since then, the Ibovespa has largely moved sideways, mainly due to concern that Bolsonaro might not be able to push through his various market-friendly economic proposals, such as easing environmental restrictions and boosting mining production through reforms, in the wake of the Vale dam disaster. Plus, the economic data has come in on the soft side. On top of that, Michel Temer just became the second former Brazilian president to be arrested as part of a sweeping corruption probe that has brought down top business executives and politicians and continues to stir political uncertainty. Investors responded by pushing the Ibovespa down as much as 2.64 percent Thursday. The real was the worst performer among major currencies, falling as much as 1.58 percent in early afternoon trading. Foreign investors haven’t really bought into the Bolsonaro Boom: They pulled the equivalent of $112 million from Brazilian stocks this year through mid-March, extending a 2018 exodus that marked the biggest annual outflow since the global financial crisis, according to Bloomberg News.

OIL’S COMPLICATED DOLLAR RELATIONSHIP

One thing that a strong dollar may do is help temper the rebound in oil prices. Despite a “risk-on” day in markets, oil was little changed at right around $60 a barrel for West Texas Intermediate crude. Commodities such as oil are largely traded in dollars, so a rising greenback tends to make them less affordable. As this space pointed out Wednesday, higher oil prices have the potential to take a toll on manufacturers as well as consumers because the economy has decelerated greatly this quarter, and they may not easily be able to absorb the increased cost. That wasn’t really the case last year when oil surged above $70 a barrel because companies were basking in double-digit earnings gains brought on by the cut in corporate tax rates. But those benefits are going away, and earnings this quarter and next are forecast to be flat to lower in the aggregate. It remains to be seen whether slower growth restrains oil prices or whether tighter supplies forces prices higher. U.S. government data Wednesday showed that nationwide stockpiles fell by the most since July. The 9.59 million-barrel decline in American oil stockpiles confounded all 10 forecasts from analysts in a Bloomberg survey.

TEA LEAVES

The Fed justified its decision Wednesday to keep rates on hold this year by pointing to a deteriorating economic outlook. The central bank backed that up by slashing its forecast for real gross domestic product growth this year to 2.1 percent, a full percentage point below last year’s pace. What this means is that any bit of positive economic data that comes in will open the Fed up to criticism that its sudden dovishness is solely to please the White House and underpin financial markets. The carping could start as soon as Friday, when Markit releases its monthly manufacturing index and the National Association of Realtors reports on existing home sales for February. Forecasts call for both to be solid. Markit’s manufacturing index for March is expected to be little changed at 53.5 compared with 53 in February. The drop in mortgage rates has given housing a small boost, with existing home sales expected to rise 3.2 percent in February after January’s 1.2 percent drop.

DON’T MISS

Bond Traders Have 3 Choices in 'Fed End’ Market: Brian Chappatta

Why the Fed Committed to Its Policy U-Turn: Mohamed A. El-Erian

Hard Brexit Means a Hard Border for 6,000 Stocks: Lionel Laurent

The Investment Case for Real Estate Just Improved: Tyler Cowen

India's Stocks Rally Clouded by Fog of War: Anjani Trivedi

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.