Fed Has Big Decision to Make About Giving More Guidance on Rates

Powell and his colleagues on the Federal Open Market Committee still have an important decision to make.

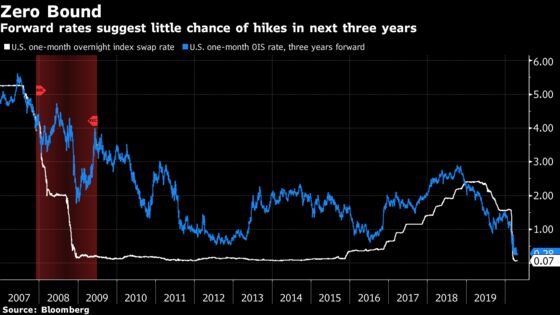

(Bloomberg) -- Federal Reserve Chair Jerome Powell has already cut interest rates to nearly zero, but he still has to decide if more should be said about how long they will stay there.

U.S. central bankers have been busy rolling out emergency lending facilities to provide liquidity to an economy largely shut down by the coronavirus pandemic. It’s taken them away from the primary object of their attention in more normal times: deliberating over where to set borrowing costs.

Powell and his colleagues on the Federal Open Market Committee still have an important decision to make on that front. A big lesson from the last time rates were this low is that it’s just as pressing to be clear with the public about how long they plan to stay there if they want to get the maximum boost for the economy.

That’s why the guidance they’ve issued about the future path of interest rates will probably be part of the conversation at the FOMC’s two-day meeting starting Tuesday -- even if it’s too early in the debate to yield much change in the committee’s policy statement when it is released at 2 p.m. Wednesday.

“It is urgent that the Federal Reserve should provide strong forward guidance commitments as soon as possible to strengthen expectations for a strong recovery, lower real interest rates by shoring up inflation expectations and convince businesses to take on the additional debt its credit market programs are making available -- rather than reduce costs and wait-and-see,” said Krishna Guha, vice chairman at Evercore ISI in Washington.

When the FOMC announced March 15 it was cutting overnight borrowing costs to almost zero, it said it would hold rates there “until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.”

Surging Unemployment

Since then, millions of people have lost their jobs as large swathes of the economy went into lockdown to limit the spread of the virus. The latest data suggests unemployment may have risen to 20% this month, twice as high as it went in the aftermath of the 2008 crisis.

Guha and Simon Potter, both former New York Fed officials, say the wording of the March 15 statement leaves too much room for interpretation. They co-authored a proposal suggesting the FOMC commit publicly to keeping its benchmark rate at zero at least until the unemployment rate is back to 4%. But they take it a step further, saying the Fed should also commit to zero rates until inflation since the beginning of 2020 rises to 2.5% on average.

All of that would anchor longer-term interest rates by sending a message to the public that the central bank won’t prematurely tighten policy, helping it avoid the kinds of policy mistakes that plagued the long, slow expansion that followed the last downturn.

When the Fed cut rates to zero in 2008 and began pumping cash into the financial system through massive bond-buying, policy makers quickly turned to the prospect of an eventual exit strategy. They were worried about inflation even though unemployment was very high. Investors knew this, and as a result, long-term borrowing costs stayed high throughout the early years of the recovery even though the federal funds rate was pinned near zero.

Evans Rule

In December 2012, the FOMC issued guidance stating it would keep rates low until either the unemployment rate fell below 6.5%, or inflation rose above 2.5%. It was dubbed the “Evans Rule,” named after Chicago Fed President Charles Evans, who had been pushing his colleagues to adopt such a strategy.

At the time, the unemployment rate was still 7.9%. But by and large, Fed officials didn’t believe they would be able to return the economy back to the 4.5% unemployment rate that prevailed before the crisis without stoking inflation, because their estimates of the so-called natural rate of unemployment had risen.

The idea was that the deep recession had opened up a structural mismatch between the skills employers were seeking and those the unemployed possessed. It’s part of the reason the Fed raised rates several times between December 2015 and December 2018, even though inflation wasn’t taking off.

Fears Unfounded

The fears about skills mismatches giving rise to inflation proved unfounded. Unemployment fell as low as 3.5% in February, on the eve of the pandemic. Employers invested in training to equip new hires with the skills they needed, and even began dipping into previously-shunned pools of labor, like those with criminal records or who couldn’t pass a drug test. Meanwhile, inflation remained below the Fed’s 2% target, as it mostly had been since 2012.

It’s an error Powell and his colleagues have been open about addressing. They launched a review of their policy-making framework in 2018. They held “Fed Listens” events around the country in 2019 to gather feedback from community leaders. And one of their big takeaways from the process was the power of offering strong guidance on interest rates to support the economy in tough times.

This week’s meeting may be too soon for the committee to come to an agreement on what to say. There may still be concerns about how to address fears that low rates contribute to financial instability -- an issue they discussed extensively in January, according to minutes of that meeting.

Press Conference

But even if it is too soon to issue stronger guidance now, the question will probably come up when Powell speaks with reporters 30 minutes after Wednesday’s statement is released, which would allow him to set the stage for an update at the next FOMC meeting in June.

That would give the public a better understanding of the Fed’s aims and its commitment to pursuing them, according to Claudia Sahm, director of macroeconomic policy at the Center for Equitable Growth, a Washington think tank.

“What does ‘victory’ look like? That’s a good discussion,” Sahm, a former Fed economist, said.

“It could have a positive effect on how the Federal Open Market Committee approaches their decision-making. It gives them a framework,” she said. “In the years before the coronavirus, in some sense, they became unmoored.”

©2020 Bloomberg L.P.