Dizzying Week Turns Tables on Stock Market’s New Buyers Alliance

Dizzying Week Turns Tables on Stock Market’s New Buyers Alliance

(Bloomberg) -- Behind the big recovery in stocks has been a loose consortium of new and old buyers, each responding to a distinct storyline. Traders banking on the Federal Reserve, market novices bent on picking the bottom, and people convinced megacap tech is invincible.

Whether they will be enough to sustain a lasting rally is the next urgent question for bulls, especially now, after a two-session sell-off erased a week’s progress. Friday’s 2.8% fall in the S&P 500 Index served notice that volatility remains an ever-present risk in a market that is flying blind on the economy.

April was the best month for the S&P 500 in 33 years, and each group -- Fed front-runners, retail newbies, Fang worshipers -- had a role in the rally, their influence felt in equal measure. Credit-challenged small caps, tech megacaps and the growth stars beloved by individuals surged by the same amount: 15%. Then, on Friday, each fell more than the S&P 500.

On the week, the S&P 500 slipped 0.2% and the Nasdaq 100 fell 0.8%. With forward valuations above their levels from February, it’s getting harder to feed a rally that has restored half of the crash’s decline, according to Michael O’Rourke, JonesTrading’s chief market strategist.

“They’ve had a nice rally and that’s good, but that’s not enough,” O’Rourke said by phone. “We hit very expensive levels, and we have all those headwinds to deal with ahead of us,” he said. “It won’t be a linear process.”

Measures of anxiety just surged. The Cboe Volatility Index, at one point down 50 points from its record of 82 in March, posted its biggest two-day gain in five weeks. While only a blip on a chart of the recovery, the pounding in the S&P 500 raised fresh questions about whether the current batch of bulls, who until now found solace in the dreariest of environments, will keep buying during what may be the worst recession in nine decades.

Here’s a rundown of where things stand:

Tech Talk

Throughout the coronavirus bust and boom, one thing has been constant: investors considered tech as a haven. The Fang titans especially, revered for their strong balance sheets and high growth, acted as a ballast, with some even posting double-digit gains this year. For a while, at least, it seemed it was enough to keep the market aloft.

“These companies have earnings, they’ve been resilient,” Katie Koch, co-head of fundamental equity at Goldman Sachs Asset Management, said by phone.

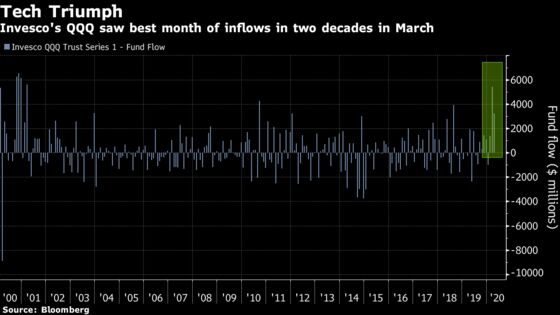

Exchange-traded funds tracking tech stocks saw their best two months of inflows in March and April since at least 2013, with about $12.5 billion added in total, according to data compiled by Bloomberg. And Invesco’s tech ETF, ticker QQQ, had its best month in about two decades in March, attracting almost $5.4 billion.

To Seema Shah, chief strategist for Principal Global Investors, it makes sense to gravitate toward the defensive. “Within that I mean assets like megacaps, which will tend to have stronger cash flow, stronger balance sheets and size to withstand a lot of the pressure this is creating,” she said.

That theory -- that the Fang block is better able to hold firm against virus-induced blows -- was tested this week. Netflix Inc., among the first to release earnings this season, added a record number of subscribers in the first quarter of the year, but Apple Inc. disappointed after failing to provide a forecast for the first time in more than a decade, sparking worries that performance could suffer. Alphabet Inc.’s advertising sales slowdown over the past two months wasn’t as severe as some analysts had feared, but Amazon.com Inc.’s Jeff Bezos warned his company is navigating “the hardest time we’ve ever faced.”

Debt Debate

This week also saw a changing of the guard as investors warmed to smaller-cap firms. Whereas those companies, whose debt burdens tend to be higher and balance sheets chancier, were disproportionately hit during the early innings of the crash, they’ve recuperated since, thanks to the Fed’s interventions and massive balance-sheet expansion, says Ed Campbell, managing director and portfolio manager at QMA.

To Greg Dean, portfolio manager at Cambridge Global Asset Management, which is owned by CI Investments Inc., their recent pummeling proved an opportunity. “If you can convince yourself to move down-cap but not lower your quality bar, I think you’re able to look at a bigger pond,” said Dean, whose firm bought shares of SiteOne Landscape Supply Inc. and home-furnishings chain RH (Restoration Hardware), among others.

Companies in the S&P 500 with the diciest credit rose 5% over the last week, compared with 0.4% for those with the best, according to data compiled by Bloomberg.

But “people are confusing liquidity and solvency,” said QMA’s Campbell. “If a company is fundamentally solvent and experiencing a liquidity issue, the Fed can solve that, but for companies that don’t have revenue during this lockdown and have balance sheet issues, the Fed is not going to be able to prevent or solve those solvency challenges.”

Nerves showed amid Friday’s sell-off, with Goldman Sachs basket of stocks with strong balance sheets besting an equivalent gauge of firms with weaker ones by more than 1 percentage point.

Retail Rush

While professionals continue to debate the staying power of the rally, small investors have been lured in -- in a big way. Many online brokerages -- which now offer zero-fee trading -- saw record account openings during the first quarter. E*Trade Financial Corp. saw more accounts opened and dollars invested in the first quarter than in any prior full-year period.

Last month, clients shifted away from historically defensive positions and into sectors associated with a growing economy, according to Rick Swope, senior director of investor education at E*Trade. Traders swooped in on pummeled cruise-line and airline sectors given their attractive valuations and potential for a future rebound, he said.

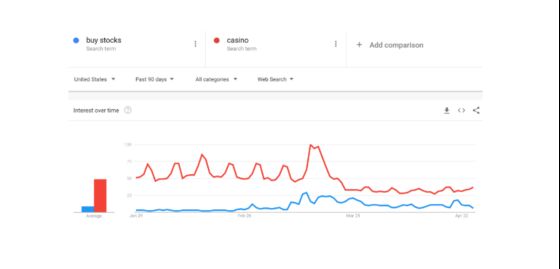

To Nicholas Colas, co-founder of DataTrek Research, the mom-and-pop rush into equities over the past eight weeks has been one of the most surprising features of the Covid-19 crisis. Typically, retail investors tend to sell sudden shocks that cause unemployment because many want liquidity in case they lose their jobs. But the recent trend can at least partly be attributed to the fact that casinos have been shuttered and sports-betting events canceled, with their foray into markets coinciding with a surge in Google searches for “buy stock,” he said.

“The dopamine rush of a full house is the same as holding a hat-sized stock into an up 3% open on the S&P,” Colas wrote in a note. “The human brain doesn’t know -- or care -- that one is gambling (a proven long run zero return) and one is investing (proven long run compounding).”

Alas, there’s evidence the populist uprising that lifted stocks from the bottom has run out of steam. Exchange-traded funds favored by buy-and-hold investors suffered an almost $4.5 billion exodus in April -- the first monthly drawdown in six years and the most since at least 2013, according to Bloomberg data.

©2020 Bloomberg L.P.