Fed’s Historic Step Into Credit Market May Cure ETF Dislocations

Fed’s Historic Step Into Credit Market May Cure ETF Dislocations

(Bloomberg) -- The Federal Reserve’s foray into corporate bonds and certain credit exchange-traded funds is helping restore order between the two markets.

After becoming unmoored in recent weeks as bond-market liquidity dried up, ETFs that stand to benefit from Fed buying are now rallying. That’s reuniting the price of those funds with the value of their underlying assets.

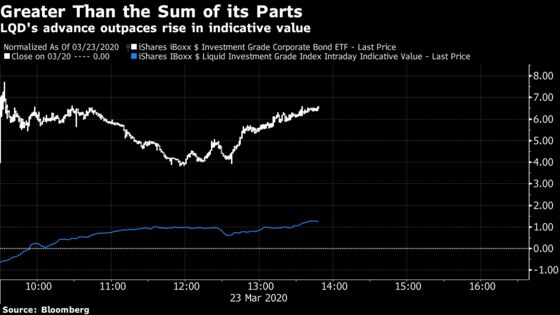

The $29 billion iShares iBoxx Investment Grade Corporate Bond ETF, ticker LQD, is on track for its biggest surge since September 2008. Cash prices on the largest corporate-bond ETF are now trading at a 1% premium to the fund’s indicative intraday net-asset value. Last week, it slumped to a discount of 5% relative to the presumptive value of its bond holdings. The $22 billion Vanguard Short-Term Corporate Bond ETF, ticker VCSH, is also trading at a premium amid its biggest rally on record.

The moves are early indications that the Fed’s support may help repair price inconsistencies that have plagued fixed-income ETFs in recent weeks. The U.S. central bank announced Monday that it would create a Secondary Market Corporate Credit Facility, one of several new measures aimed at cushioning the economic blow from the coronavirus. The terms of the facility allow for the purchase of up to 10% of an issuer’s outstanding bonds and up to 20% of the assets of any ETF “whose investment objective is to provide broad exposure to the market for U.S. investment grade corporate bonds,” a primer accompanying the Fed action said.

“This should help bring in ETF discounts as well as potentially save outflow-ridden active mutual funds from having to enter the illiquidity hell that ETFs have been living in for the past month,” said Eric Balchunas, an ETF strategist with Bloomberg Intelligence. “It was about to get really ugly for them.”

Rampant volatility in bond markets has soured appetite for the arbitrage trade which keeps prices in line with net-asset values. In normal market conditions, middlemen known as authorized participants will purchase shares of a falling ETF in order to exchange for the underlying bonds with the fund’s issuer. That market maker will then sell those securities to pocket a virtually risk-free profit. The ETF’s price usually snaps back to the fund’s net-asset value as the supply of ETF shares is reduced.

That trade has become less attractive for those authorized participants -- typically market-making firms -- as those underlying bonds become more difficult to unload. Corporate bonds have been in the cross-hairs as investors assess the potential for credit stress as the coronavirus brought economic activity to a standstill.

Building concerns over solvency likely factored into the Fed’s decision, according to Greenwich Associates.

“I think the reason they’re choosing ETFs and they’re ‘financing facilities’ rather than straight buying corporate bonds is that they don’t want to be at the end of the default cascade,” said Ken Monahan, a senior analyst covering market structure and technology at Greenwich. “They can lose money on ETFs but they won’t become litigants in a bankruptcy.”

On Friday, roughly 32 fixed-income ETFs ended the week with a discount of at least 5% to their net asset value, while 5 funds traded at a discount of 10% or more. While the Fed’s purchases will help close those gaps, it won’t be an immediate fix, according to WallachBeth Capital.

“If the market remains strong, that should slowly start collapsing, but it won’t be overnight. Some of these discounts are huge,” said Mohit Bajaj, WallachBeth’s director of ETFs. “Liquidity is a major problem at the moment. The Fed was going to buy Treasuries too, but that still hasn’t entirely loosened up the Treasury market.”

©2020 Bloomberg L.P.