Fear, Loathing and the Best Quarter for Risk Assets in a Decade

After riding the best Q1 in at least a decade across assets, a growing chorus of investors has a new mantra: Don’t look down

(Bloomberg) -- After riding the best first quarter in at least a decade across assets including stocks, credit and crude, a growing chorus of investors has a new mantra: Don’t look down.

It’s the yin to this rally’s yang, the conclusion of the adage about things that keep going up. It also reflects growing unease that risk assets are running on little more than the fumes of a dovish turn by central banks.

As the sun sets on a remarkable quarter, discomfort is on display in the dash to bonds that pushed yields on the world’s safest debt to the lowest in years.

It’s in bunds that are bought at any price -- even when you lose money by holding them. It was in the inverted U.S. yield curve and subsequent blast of market volatility, and the deluge of hand-wringing that followed. The flight from exchange-traded stocks sensitive to cyclical downturns. The under-positioning across major assets -- including among the year’s biggest winners.

“Markets are worried,” said Sophie Huynh, a cross-asset strategist at Societe Generale in London. “The lack of conviction is clear.”

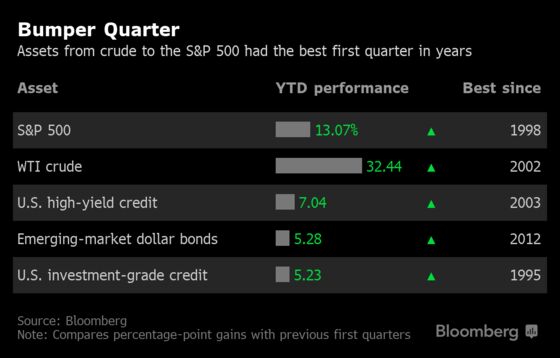

Add up all the green and the nervousness makes sense: A rebound of 13 percent in the S&P 500 Index, a jump of 7 percent in U.S junk bonds and an eye-watering 32 percent surge for oil are among the stand-out statistics.

These kind of gains, at this kind of pace, by their nature sow the seeds of instability and doubt.

For Pacific Investment Management Co., the rally in risk assets has gone too far. The $1.7 trillion fund manager is now “slightly underweight corporate credit” and “cautious” on equities, according to global economic adviser Joachim Fels.

“We would like to fade this rebound in the markets,” Fels said in an interview with Bloomberg TV. “We’re a little bit cautious on risk assets at this stage particularly given how well they have done since the beginning of the year.”

A glance at the bond market offers more reasons for caution. This was the quarter in which the Federal Reserve and other policy makers around the world veered away from tightening, forcing investors to rethink the outlook for economic growth and inflation.

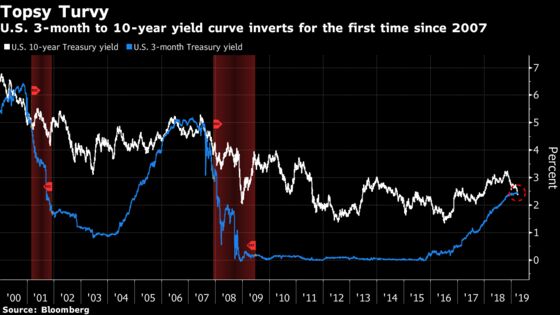

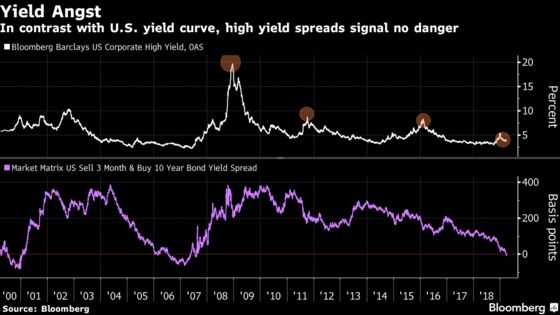

In the ensuing rush to the safety of government debt, the 10-year and three-month Treasuries spread turned negative for the first time since 2007 -- in doing so generating even more angst about growth.

Yet the accommodative stance of central bankers is also a primary catalyst for the cross-asset gains in 2019. Policy makers have shown they’re ready to rush to the aid of markets, and that in itself is a reason for many investors to ignore their misgivings and keep buying.

Federal Reserve officials slashed their projected interest-rate increases this year to zero from two, while the European Central Bank extended its pledge on record-low rates. Policy makers in China are doling out fiscal and monetary stimulus to revive growth laid low by trade tensions with the U.S.

“Policy makers want to prevent a slide, and they’ll succeed -- at least for a while,” said Charlie Morris, head of multi-asset at Atlantic House Fund Management in London. Morris is buying 30-year bonds, and is fully-invested in gold and equities. “Investors are sitting on huge cash piles. They see a bearish consensus, and, there’s no alternative, they have to buy because the economy will be supported by policy.”

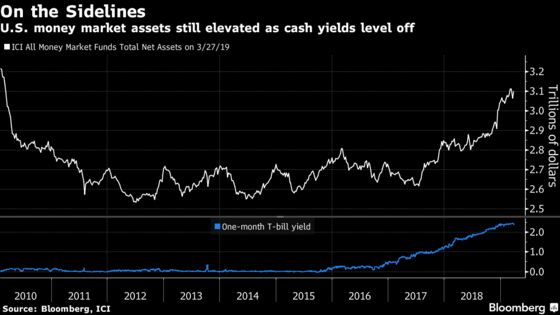

There’s a lot of dry powder. Total assets in money-market funds remains at about $3 trillion, according to data compiled by Bloomberg. That’s near the highest since 2010, even though the yield on one-month Treasury bills appears to be topping out.

That cash hasn’t done an awful lot in 2019, with U.S. three-month T-bills returning just 0.6 percent. And there are signs it may come back into play. The latest global fund manager survey from Bank of America showed cash levels fell to 4.6 percent from 4.8 percent a month earlier.

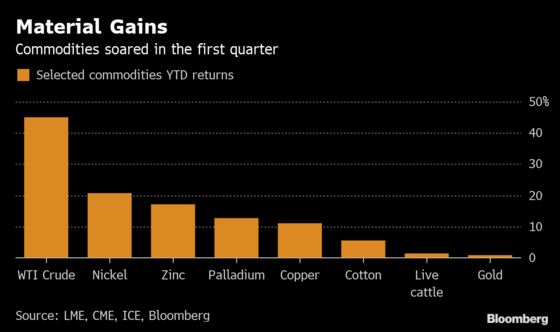

Meanwhile, the rally in commodities, from oil to copper, suggests investors are betting on a policy-spurred recovery in China, at the very least. The nation is the world’s biggest buyer of many raw materials.

A revival in the country is at the heart of the investment strategy favored by Christophe Donay, head of asset allocation and macro research at Pictet Wealth Management. He expects both a detente in trade tensions and the effects of stimulus to percolate through the world’s second-biggest economy, and is selling bonds even as they rally in favor of riskier, illiquid assets.

“All the engines of the Chinese economic policy are on,” said Donay, who’s cut allocation to government bonds in his multi-asset portfolios to 10 percent from as much as 30 percent in recent years. “We’re looking for a rebound after a deterioration which was temporary because of the impact of trade war. We expect a truce in trade by April and that could help the rebound in the euro zone and U.S.”

Any global trade truce won’t come soon enough to stave off the threat of a rough earnings season. Slowing profit growth played a role during the market meltdown in the fourth quarter of 2018, and investors are on guard for further signs of weakness when the results for the first quarter roll in.

It’s muting enthusiasm for equities. Even as a gauge of global stocks posted the best quarter in seven years, investors pulled $79 billion from equity funds, according to Bank of America. An MSCI index of so-called quality companies -- those with strong balance sheets -- has gained more than 14 percent this year, versus about 9 percent for those with a weaker financial profile.

That kind of investor caution stands out in particular, because the moves across credit markets this quarter have looked pretty favorable for any companies carrying debt. Borrowing costs seem to be falling across the board, even for junk-rated issuers. U.S. high-yield corporate bonds have enjoyed one of their best first-quarters in at least two decades.

While some of the demand for such securities is no doubt a result of investors searching for returns in a negative-rate world, the appetite for risky assets is in stark contrast to the economic concern that’s driven the collapse of government bond yields. Once again, some may conclude the rally has gone far enough.

It’s all enough to sideline money managers like Ricardo Gil, who helps oversee 4.6 billion euros ($5.2 billion) at Trea Asset Management in Madrid.

“We’re holding back on increasing equity positions again until the first-quarter earnings season," said Gil, who’s also been paring risk in corporate credit since February. “We’re rather defensive in both fixed-income and equities.”

--With assistance from Todd White, Jonathan Ferro, Lu Wang, Ksenia Galouchko, Jan-Patrick Barnert and Sarah Ponczek.

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Eddie van der Walt in London at evanderwalt@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.