Fate of Leveraged Loans Won't Be Decided by ‘Cov-Lite’ Alone

Fate of Leveraged Loans Won't Be Decided by ‘Cov-Lite’ Alone

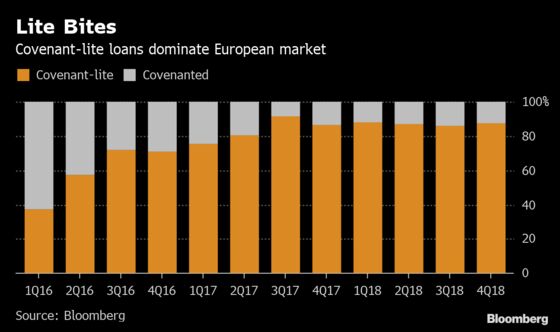

(Bloomberg) -- The lack of covenants on leveraged loans has become regulators’ favorite stick to beat the market with when they warn of overheating, but where companies run into trouble there are other risks impacting how much money lenders will lose.

Also of critical importance is how aggressively private equity sponsors use the increased flexibility now found in loan terms, and how good a job investors do in managing credit stress in their loan portfolios without the early warning signal of a formal leverage test.

“Underlying documentation is also where investors and regulators should be focusing rather than just the current one-dimensional focus on covenant-lite,” Ranbir Singh Lakhpuri, a senior portfolio manager at Insight Investment Management Global Ltd., said by telephone, calling the attention to this one characteristic “simplistic.”

The outcome of all this means highly-indebted companies will likely experience lower and more dispersed recovery rates in the next downturn of the credit cycle than they did 10 years ago, and the proliferation of “cov-lite” loans will only be one of the contributing factors.

Value Out

Current loan documentation often allows for the addition of incremental debt that can push leverage higher. Private equity sponsors, which drive most leveraged loan issuance in Europe, also have more freedom to move valuable assets out of the lenders’ security package, and to inject new debt that could go in at a more senior level than the original first-lien term loan.

“What drives lower recoveries is the rise in senior leverage,” Edward Eyerman, head of European leveraged finance at Fitch Ratings Ltd., said by telephone. “Covenant-lite’s role is misconstrued because it’s the restricted payment covenants that give the company the ability to move value out of lenders’ reach. That’s the real issue.”

A London-based manager for a global asset management firm said he finds it difficult to argue with the consensus view that recovery rates in the next downturn will be around 60 percent of par not 70 percent as previously, since without maintenance covenants lenders won’t get to the negotiating table until later in the process. But given the range of other influences, recoveries will more dispersed with some at just 10 to 20 percent, and others up at 80 to 90 percent, he added.

Eyerman also noted that documentation allows shareholders to be “very aggressive via loopholes” in loan terms, and points to ongoing court cases in the U.S. where lenders are contesting such moves such as PetSmart Inc.

Another difference that may drive more variation among recoveries in future restructurings is that CLOs, which make up about half of the investor base, could be in a stronger position than they were a decade ago. In theory, it’s now easier for them to inject new “rescue” money into a troubled credit and so benefit from any future increase in value, whereas previously they were barred from doing so.

“Recovery rates will be more volatile this time because of the increasing flexibility and optionality in the documentation and uncertainty over new-money needs and its ranking," said Eyerman.

Bad, Worse

Recovery rates emerge after a credit has actually defaulted, but before they reach that point the investors that lent at par won’t be sitting by and helplessly watching bad turn to worse.

Many fund managers say that although maintenance covenants were valuable negotiation triggers in the past, they never relied on them to provide a warning of credit stress. Instead, managers have their own internal monitoring processes, which require analysts to regularly reaffirm or “re-underwrite” their confidence in a given credit if it’s to stay in the portfolio.

“Whilst recovery rates are expected to fall in a cov-lite world it shouldn’t be the ‘Armageddon-type’ of situation that some present,” said Insight’s Singh Lakhpuri, emphasizing the importance of being highly selective on sectors and credits.

If these processes are sound, loan managers ought to be able to dodge credit trouble spots by selling, or they may take a view that the sponsor will manage through a tough period, perhaps even aided by not having formal restrictions on leverage.

But there are difficulties here that could also feed into varied experiences around distressed situations.

Loan documentation now commonly includes restrictions on which type of funds can buy a loan. Until the borrower defaults, the original lenders may be banned from selling or quietly transferring risk to a distressed fund. However, the language that governs this aspect of a leveraged loan may be open to interpretation and difficult to enforce -- and it’s broadly untested in Europe. High-yield bonds meanwhile are similarly covenant-lite but are freely transferable.

Another obstacle to lenders’ ability to manage risk before default and so keep their portfolios healthy is that they are getting fewer and less-detailed updates on how companies are performing.

The Long Wait for Numbers Could Cost Leveraged Lenders Dearly

Fund managers must also decide how much weight to give to sponsors’ assertions that they won’t use all the flexibility available to them in loan documentation. It might seem naive to imagine a private equity firm not taking full advantage, but reputation could possibly play a role in their decisions. Lenders continue to be mindful of sponsors’ past behavior during previous restructurings.

Over time -- as the next generation of recovery rates emerge from covenant-lite credits that fall into distress -- leveraged lenders will be able to judge how fair the accusations were that the market has run amok in an era of easy-money policy from central banks.

‘Considerable Debate’

- Recovery rates will be “materially lower” in the next downturn, according to Standard & Poor’s Global Ratings, forecasting about 58 percent for first-lien loans, versus the historical average of 73 percent.

- There is “considerable debate” around what impact the lack of covenants will have on recoveries, S&PGR said in a Feb. 8 report

- It’s “logical to assume that a delay in default” will lead to value being destroyed during that time and hence a lower enterprise value at default

- However the “magnitude of this value erosion is difficult to determine”, and incremental facilities could have the “largest, and least well-understood” impact on a borrower’s recovery outcome

- Read More: Lack of Covenants, Maturity Pressure to Keep 2019 Defaults Low

(Ruth McGavin is a leveraged finance strategist who writes for Bloomberg. The observations she makes are her own and not intended as investment advice.)

--With assistance from Marianna Aragao and Sarah Husband.

To contact the reporter on this story: Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Tom Freke at tfreke@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.