Fasten Your Seatbelts for a Bumpy Earnings Ride

Fasten Your Seatbelts for a Bumpy Earnings Ride

(Bloomberg) -- We’re entering the results season after a 15% equity rally in Europe and with U.S. shares at an all-time high. This puts the market at risk of a pullback if corporate profits disappoint, so it’s just as well expectations are low. But with strong divergence between the industry sectors, there’s always the potential for a few shocks.

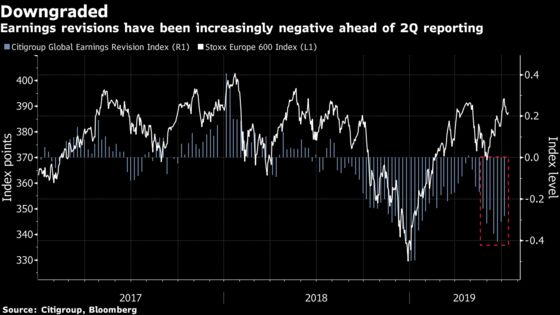

Generally speaking, analysts have downgraded their views on equities since early May, as shown by the Citigroup earnings revisions index. This translated into lower estimates for European companies, with 0.9% year-on-year EPS growth predicted for the second quarter, down from 6% in January, according to Barclays.

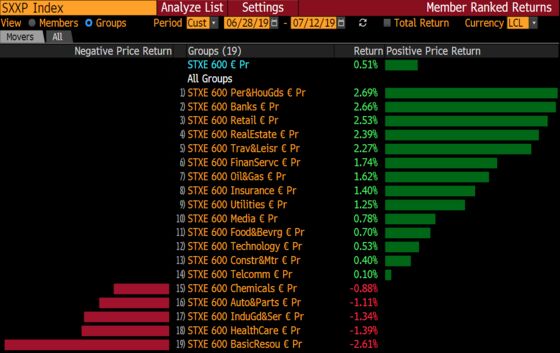

It gets more interesting when you look at industry groups. Most have seen downward EPS revisions since January, according to Goldman Sachs strategists. Value sectors, particularly autos, telecoms, basic resources and financials have been heavily cut, while defensive growth stocks such as healthcare, food & beverage and some industrials have shown resilience.

Daimler couldn’t wait for its scheduled announcement on July 24 to issue its fourth profit warning in just over a year. Although it doesn’t bode well for other carmakers, the reaction of stocks in the sector was muted as expectations for autos have already been cut severely.

Metal and mining stocks could offer some surprises. At current commodity prices, this year’s EPS should be 34% above 2018, according to JPMorgan analysts, noting that consensus only expects 4% growth. They see shares of the sector as likely to receive substantial upgrades, particularly given their attractive valuations.

Barclays warns investors about growth stocks that are “priced for perfection.” They see professional services, consumer durables, food & beverage, capital goods, transport, technology and leisure as expensive with stretched earnings.

So far, the broader rally has been more the result of expectations for the easing of central bank policy than anything else, according to strategists at Bank of America Merrill Lynch. Indeed, hopes of a trade truce didn’t have much effect on stocks. Interestingly, most commerce-sensitive sectors underperformed since talks restarted at the G-20 summit, until they moderately bounced back on Friday. At some point, the market will need some tangible earnings growth for the rally to continue.

In the meantime, Euro Stoxx 50 futures are trading up 0.2% ahead of the open.

- Watch luxury goods makers, miners and steelmakers after data over the weekend showed Chinese economic growth slowed in the second quarter but with signs emerging that the economy is stabilizing. China’s GDP growth in the April-June quarter slowed to 6.2%, the weakest pace since quarterly data started back in 1992.

- Watch the pound and U.K. stocks as the battle between the two contenders to be Britain’s next prime minister is getting messy. Boris Johnson admitted that he doesn’t know all the details involved in the plan B, should the U.K. leave without a deal. Johnson also said it would be “insane” to suggest the October 31 deadline could not be met. Separately, pro-EU campaigner Gina Miller said that if the government were to suspend Parliament to push through a no-deal Brexit, she’ll sue.

- Watch European beverage stocks including Heineken and Carlsberg, which could be active after AB InBev decided to scrap a planned Hong Kong IPO of its Asian business, citing market conditions.

COMPANY NEWS AND M&A:

- AB InBev’s Shelved Listing Cuts Hong Kong IPO Volume in Half

- Why Budweiser and Its Bankers Failed to Sell the King of IPOs

- Gilead to Pay $5.1 Billion, Raise Stake in Biotech Galapagos

- Bayer Loses Bid for a New Trial in $80 Million Roundup Case

- Deutsche Bank to Boost Asian Corporate Bank, Wealth Mgmt: SCMP

- SocGen Is Cutting Jobs in London as Oudea Revamp Takes Hold

- Alitalia Rescue Plan Could See Delta Boost Initial Stake

- Porsche, Ferarri to Recall Cars in China to Replace Faulty Parts

- Axfood Reports Second Quarter Earnings That Beat Estimates

- Telenor Grameenphone 2Q Revenue NOK3.68B; Negative Impact

- LafargeHolcim to Buy Romanian Concrete Maker Somaco; No Terms

- Balfour Beatty Starts Probe Into Corruption Allegations: FT

NOTES FROM THE SELL SIDE:

- AB InBev’s decision to scrap a planned IPO for its Asia business is likely worth ~EU3-EU4 per share on a sum-of-the-parts calculation, according to Jefferies (underperform).

- Gilead’s agreement to raise its stake in Galapagos de-risks the Belgian biotech’s story, and marks a “significant step toward establishing itself as an independent specialty pharma company,” Citi (buy, EU140) says in note.

- Morgan Stanley downgraded Schroders to underweight, with its premium multiple difficult to justify, broker says in asset manager note in which it highlights a widening divergence of flows within the sector.

- Jefferies cut Adecco to underperform from hold and lowered price target by 22% to Street-low CHF43, with momentum seen set to stay subdued in 3Q.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 397.9 (May 2018 high); 403.7 (2018 high)

- Support at 385.7 (76.4% Fibo); 380.8 (50-DMA)

- RSI: 54.8

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,520 (76.4% Fibo); 3,596 (May 2018 high)

- Support at 3,413 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 59

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- ADO Properties upgraded to buy at HSBC; PT 50 Euros

- P2P Global Investments upgraded to hold at Jefferies

- SMCP upgraded to buy at Jefferies; PT 18.50 Euros

- Solvay Upgraded to Hold at Kepler Cheuvreux; PT 95 Euros

- TLG Immobilien upgraded to buy at Baader Helvea; PT 30 Euros

DOWNGRADES:

- Adecco downgraded to underperform at Jefferies

- Elisa downgraded to neutral at JPMorgan; Price Target 41 Euros

- UBS cut to underperform at Mediobanca SpA; PT 11.40 Francs

INITIATIONS:

- None reported.

MARKETS:

- MSCI Asia Pacific up 0.1%, Nikkei 225 up 0.2%

- S&P 500 up 0.5%, Dow up 0.9%, Nasdaq up 0.6%

- Euro up 0.02% at $1.1272

- Dollar Index up 0.02% at 96.83

- Yen down 0.09% at 108.01

- Brent down 0.2% at $66.6/bbl, WTI down 0.4% to $60/bbl

- LME 3m Copper up 0.7% at $5975.5/MT

- Gold spot down 0.1% at $1414/oz

- US 10Yr yield up 1bps at 2.13%

ECONOMIC DATA (All times CET):

- 10:30am: (IT) May General Government Debt, prior 2.37t

* For a wrap on developments in Europe’s equity capital markets, click here.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon, Celeste Perri

©2019 Bloomberg L.P.