Farewell, Transitory: Markets Heed Central Banks’ Inflation Call

The end of 2021 swept away the idea of surging inflation being transitory...

(Bloomberg) -- The end of 2021 swept away the idea of surging inflation being transitory, setting the stage for markets to game the pace of central bank tightening next year.

A string of central bank meetings in recent days saw policy makers overlook economic risks from the omicron strain in favor of damping price pressures that they had brushed off as temporary a matter of months ago. That led traders to price in more interest-rate hikes, sending ripples through currencies, bonds and stocks.

For investors it offers a playbook for what might come next year. The dollar has been buoyed by the prospect of multiple Federal Reserve hikes in 2022, the pound recovered as the Bank of England unexpectedly raised rates, while knee-jerk gains in the euro and bond yields suggest traders are focusing on the European Central Bank’s view of upside risks to inflation.

“Throughout 2021, the debate was whether soaring inflation is transitory -- this debate is now over,” said Nigel Green, chief executive of deVere Group, which has $12 billion under advisement. “From the U.K. to the U.S., China to Europe and amongst most other economies, inflation risks are real. And they’re building.”

The collapse of the transitory rhetoric has been swift. Three weeks ago BOE official Catherine Mann said it was “premature to even talk about timing” of a rate hike, only to vote for the U.K. central bank’s surprise increase on Thursday. Fed officials removed a prior reference to inflation reflecting factors that were “expected to be transitory” on Wednesday, a stance it held for most of 2021.

“Global central banks have provided investors with an important toolkit to position for what lies ahead in 2022,” said ING Groep NV currency strategist Francesco Pesole. “If we were to find a common denominator of the G3 central bank messages this week it is the centrality of inflation in the policy discussion.”

Here are some charts of how that’s playing out across markets:

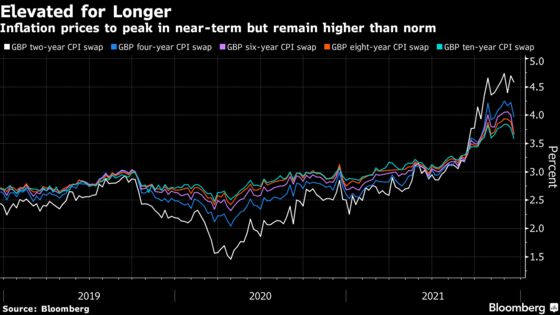

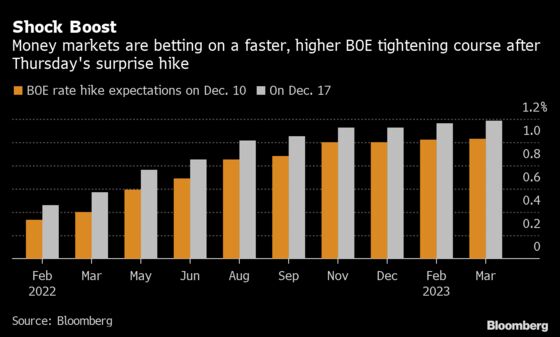

Rates Reprice

The BOE’s November meeting, where officials comfortably voted to keep rates on hold despite markets mostly pricing in a hike, made traders reassess their outlook for central bank tightening in 2022. Thursday’s decision turned the outlook on its head again, boosting bank shares, hurting U.K. gilts and sterling corporate bonds.

Money markets are now pricing a more aggressive hiking sequence, with traders betting on the BOE rate getting to 1% by August.

Credit Change

Euro-area corporate bond market spreads have widened more than 10% in the past month on expectations of ECB asset purchases being tapered, even after recovering from the omicron shock. Investors are increasingly pricing in less support for assets eligible for quantitative easing from next year.

“Credit purchases feel on borrowed time,” Bank of America Corp. strategists led by Barnaby Martin wrote in a note to clients on Friday. “We think this will drive a clearer underperformance of eligible corporate bond spreads as we approach the second half next year.”

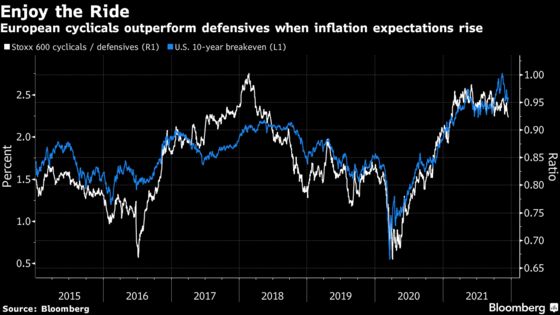

Taking Stock

European cyclical stocks, from automakers to miners, tend to outperform their defensive peers in sectors such as health and utilities when inflation expectations rise. Their relative performance has been stalling this year as the U.S. 10-year breakeven stabilized.

If the hawkish pivot from the Fed starts to tame inflation expectations, defensive stocks could start outperforming. Bank of America has an underweight view on cyclicals versus defensives.

“Tightening monetary policy is a key reason to be bearish on asset prices,” said Bank of America strategists led by Sebastian Raedler.

Next Week

- There are no major debt auctions, while the ECB will pause its QE program from Dec. 22 to Jan. 3

- Data is mostly second-tier and backward looking, while ECB’s Kazimir and Holzmann, who are scheduled to speak on Tuesday and Wednesday respectively, may provide some insight into the last policy decision

- On Dec. 24, euro-area cash bond trading and the Eurex exchange are closed and ICE will operate a shortened day

©2021 Bloomberg L.P.