Treasury Yields Flirt With 2019 Lows Amid Doubts on Trade Deal

Treasury Yields Flirt With 2019 Lows Amid Doubts on Trade Deal

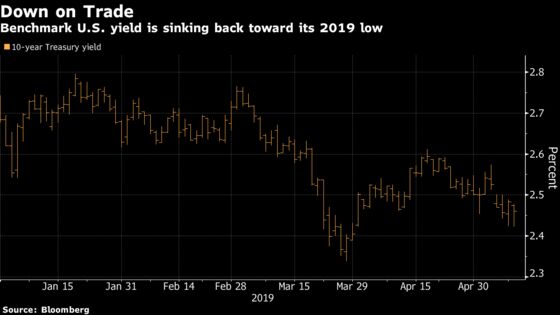

(Bloomberg) -- A breakdown in U.S.-China trade talks could mean a break out for the Treasury market, with yields homing in on this year’s lows.

The prospects are looking bleak for a deal to prevent the U.S. from slapping higher tariffs on Chinese imports on Friday. Hanging in the balance, according to some investors, is the positive global growth scenario that many have been anticipating would guide yields higher in the second half of 2019.

“Today we have to rethink that thesis,” said Jim Caron, fixed-income portfolio manager at Morgan Stanley Investment Management. “It leaves me questioning where the next upside impulse is” in yields, as slower-than-expected growth puts the long-awaited inflation rebound even further out of reach.

Without a deal, Caron says the 10-year benchmark can easily sink past the 2.34% level that marks the 2019 low in late March, to close in on 2.25%. The yield slid around 3 basis points on Thursday to 2.45%, steadying when U.S. President Donald Trump said he received a letter from Chinese President Xi Jinping and that the two would probably speak by phone.

Even with the heightened tension, Caron said he’s remaining neutral on Treasuries and favoring high-quality credit until he sees more evidence of deterioration in global growth.

Related Treasury Market Stories |

| U.S. Yield Curve Inverts for the First Time Since March Treasury Inversion Adds to Emerging-Market ‘Worry Mode’ Treasury Bond Auction Tails Slightly, Fares Better Than 10-Year |

An agreement on trade probably won’t threaten the upper bound of the 10-year yield’s range this year, says Neil Sutherland, fixed-income portfolio manager at Schroder Investment Management.

He expects a successful negotiation would drive the benchmark yield only as high as it was when a trade deal looked more secure, above 2.50%. He says 2.70% would be a more reasonable level to buy. But in his view, a trade setback isn’t a game-changer for the rates market, much less a cause for a high-conviction position in Treasuries. It would take a shift in Federal Reserve policy for that.

“Until you get the Fed to actively start cutting interest rates, you’re not going to get a significant move lower,” Sutherland said. “And I think that’s probably not realistic over the next three to six months, so I think we’ll probably remain in this rather sort of pedestrian range.”

For the time being, markets will focus on headlines out of Thursday’s meeting in Washington between U.S. and Chinese negotiators.

And BMO rates strategist Jon Hill notes that the 10-year benchmark is close to hitting the bottom of its recent range, “an outcome that may occur in short order if trade talks deteriorate further” and Friday’s consumer-price report underwhelms.

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Vivien Lou Chen

©2019 Bloomberg L.P.