ADVERTISEMENT

Fall in VIX's Relationship With S&P 500 Leaves Vega Underperforming

Fall in VIX's Relationship With S&P 500 Leaves Vega Underperforming

21 Nov 2018, 08:10 PM IST

(Bloomberg) -- An aggressive implied volatility storm has not developed amid the recent declines in global stock market indexes.

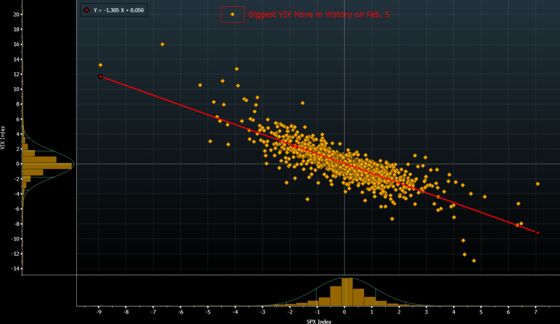

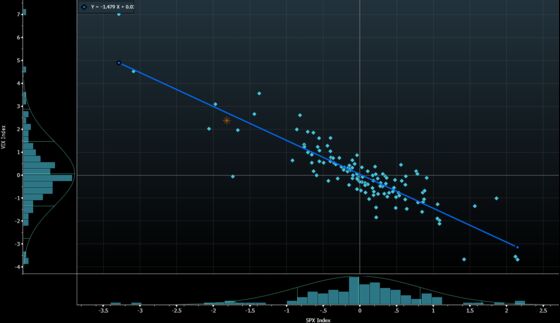

The relationship between S&P 500 and VIX has flattened, leaving put spreads on the index outperforming volatility call options. SPX realized volatility remains historically elevated (10-day at the 80th-percentile of the 5-year range) but there’s no sign of extreme downside hedging panic on short-dated skews.

- The blow-up in short-VIX exchange-traded products (ETP) in February was a unique liquidity event that saw the beta historically high to SPX and convexity options outperform given the acceleration in volatility gains as tail risk repriced

- VIX calls funded by SPX puts create cost-efficient long convexity exposure, given VIX call options tend to outperform SPX puts during sharp sell-offs; however, basis risk needs to be managed where, for example, the market exhibits a slow decline with limited volatility or the beta of SPX and VIX diminishes

- Hedging via rolling SPX put spreads may continue to outperform, with inverse VIX ETP rebalancing on vol spikes needing only a fraction of the vega buying seen in February

- Still, liquidity holes and brutal deleveraging pose a threat and may be the story of 2019 as a defensive stance grows amid quantitative tightening and growth concerns, with volatility a function of the business cycle

- NOTE: Tanvir Sandhu is a global interest-rate and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2018 Bloomberg L.P.