Stock Quant Tremor Is a Field Day for Geeks

Stock Quant Tremor Is a Field Day for Geeks

(Bloomberg) -- For a stock market that has sat almost completely still for days, this one is proving an irresistible laboratory for a brand of geeky equity analysis that has been gaining influence over the past decade.

You wouldn’t know it from benchmarks, but beneath a tranquil surface violent swings are lashing traders along obscure fault lines. Companies like real-estate firms that rose the most in 2019 are plunging, and some that have trailed are being pushed out front. It’s been a mild reckoning for hedge funds and others who have bet on the status quo persisting.

Amid all the churn has been a renewed focus on a quantitative concept known as factor investing, which groups companies not by industry but traits such as how fast their prices move or profits rise. A question gaining currency in the past few days is whether these categories are just handy descriptions of twists in the market -- or are at some level guiding them.

“It seems very mechanical right now,” said John Swarr, investment specialist at Penn Mutual Asset Management, which has $27 billion under management. “If you look within some of these stocks that are being hit the hardest, some are in much better shape than others and yet they’re all being affected similarly,” he said. “It does feel like it’s a rules-based rotation.”

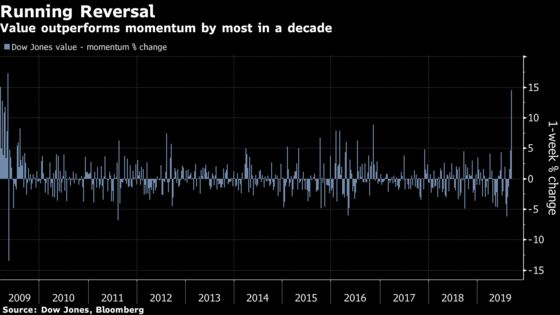

Whatever the cause, some of the moves approach the historic and have cast an interesting lens on how the 2019 market evolved. Take the momentum factor, which collects stocks that are rising the fastest. Right now, that means owning groups like REITs and utilities that shone brightest amid a protracted Treasury rally, while betting against oil explorers and banks that have fallen behind.

Both those trends reversed this week. A Dow Jones market neutral momentum index fell more than 4% two days in a row, notching its biggest plunge in a decade. On the flip-side, a similar index tracking value or cheap stocks just registered its best two-day streak since at least 2002, when the gauge was created.

All of it happened while benchmark indexes barely budged. The S&P 500 moved less than a point on Monday and Tuesday. Futures on the gauge rose 0.2% as of 7:57 a.m. in New York.

The popularity of factor investing has exploded since the turn of the century as firms like AQR Capital Management and Dimensional Fund Advisors built empires on the proposition that groups selected by traits like size and value would beat the market over time. Assets devoted to the strategy’s public-facing incarnation, smart-beta exchange traded funds, have risen 10-fold from 2009 to almost $900 billion.

So much money is tied to the strategies that a cottage industry has formed on Wall Street to analyze how changing tastes for factors are affecting institutional investors and even the path of individual stocks.

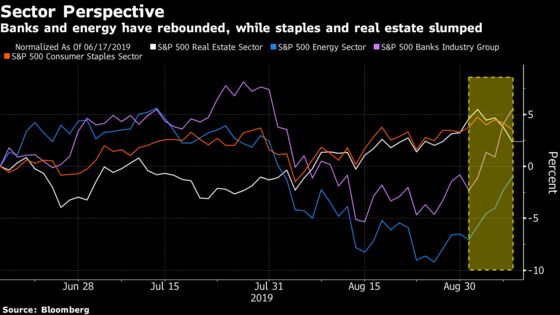

But distinguishing the dog from its tail is hard because every time factor preferences are used to explain a swing in shares or groups of companies, a simpler, more fundamental explanation tends to exist alongside it. Sure, industries like real estate, utilities and healthcare may suddenly be falling because people turned sour on “momentum” -- or simply because Treasury yields are up. Banks and energy companies may be getting lifted by a rotation into their cheap-stock “value” cohort -- or it may just be people betting on a stronger economy.

“It’s an odd set of bedfellows,” Sameer Samana, senior global market strategist for Wells Fargo Investment Institute, said by phone. “You’ve got a sell-off going on, but defensives like utilities and REITs are underperforming. Best I can tell is there’s this rotation from, call it growth stocks, high-momentum stocks, to more value-oriented parts of the market that were left behind.”

To be sure, the danger of a stock or industry moving because it has fallen in or out of favor with big investors has always existed, but any time quants get mentioned, concern will be voiced in certain quarters that correlated trades will amplify swings. It doesn’t usually play out. One episode that routinely -- many would say lazily -- gets trotted out in times of factor duress is a period in late 2007 when many systematic firms got caught on the wrong side of momentum trades and the market briefly buckled.

Most professionals say drawing the parallel now is misguided.

“Bonds were just so overbought that the backup in bond yields and investors probably taking some profits in Treasuries has caused ripple effects in markets,” said Matthew Miskin, co-chief investment strategist at John Hancock Investment Management. “So financials, regional banks all are getting a bid, which is really a catalyst for value rotation, the lack of sustained rally out of momentum. So bond yields likely are the largest factor that is causing all this market rotation to develop.”

--With assistance from Brendan Walsh.

To contact the reporters on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net;Vildana Hajric in New York at vhajric1@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.