Eye-Popping Returns Lure Hedge Funds to Japanese Startups

Eye-Popping Returns Lure Hedge Funds to Neglected Japan Startups

(Bloomberg) -- Hedge funds and asset managers are increasingly turning to Japanese startups, attracted by some eye-popping past returns in the long-overlooked sector.

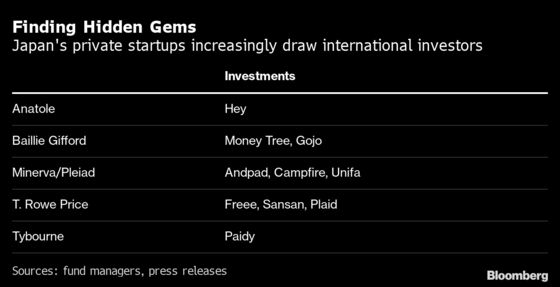

Asian hedge fund firms including Pleiad Investment Advisors and global investment giants like T. Rowe Price Group Inc. and Baillie Gifford are providing late-stage growth capital to the nation’s most promising ventures, according to fund managers at the companies.

They’re emboldened by surging share prices of startups that went public in recent years, along with renewed government efforts to promote digitalization and entrepreneurship. With just six unicorns, the world’s third-largest economy has struggled to produce new companies that have global ambitions like Alibaba Group Holding Ltd. and Tesla Inc.

“There was a real lack of institutional investors that were focused on late-stage, pre-IPO opportunities,” said Michael Yoshino, formerly of Soros Fund Management and TPG Capital, who is Pleiad’s co-chief investment officer. “More foreign investors are starting to look into Japan and look at this space. That’s because the competition is less intense, and therefore valuations are more compelling.”

Hong Kong-based Pleiad, which oversees $3 billion, last year started a private equity arm headed by two former bankers at Wall Street firms. Known as Minerva Growth Partners, its mission is to help Japanese startups reach a scale that can draw money from global institutions.

Minerva has so far raised 15 billion yen ($135 million) for its maiden fund and plans to back at least eight companies over two years, said Yoshino.

T. Rowe Price has invested in more than three such deals, starting with a 2018 private financing round for cloud accounting and human resources software provider Freee K.K., said Archibald Ciganer, Japan equity strategy fund manager who oversees $6 billion at the U.S. firm. It plans to make one or two private investments in Japan each year.

Praveen Kumar, who oversees Baillie Gifford’s more than $2.5 billion in small Japanese stocks, has made two investments and recently held a call with two U.S. peers curious about such opportunities.

Baillie Gifford and T. Rowe Price have been looking at startup deals in Japan for at least five years. Ciganer’s mandate allows him to invest in private companies that will ideally go public within 18 months and reach at least $300 million in market value once listed.

Kumar, based in Edinburgh, has no such constraints. Still, even larger private financing rounds in Japan tend to seek only $10 million to $20 million, hardly justifying the costs of due diligence work, he said.

Japan’s government has been encouraging the development of new technology companies to counter the effects of an aging and shrinking population. Progress has been slow.

The Asia-Pacific region has minted more than 200 private firms now valued above $1 billion, out of 729 globally, according to CB Insights. The largest of Japan’s six unicorns ranks 291st. Indonesia, with an economy just over one-fifth the size of Japan’s, is home to four unicorns, all ranking higher.

Historically, a small venture capital industry and Japanese banks’ reluctance to lend to fledgling companies have hamstrung startups, said Ciganer. Japanese ventures also mostly focus on the domestic market, in part because of a lack of English proficiency, he added. That caps their growth potential, capital needs and appeal to international institutions.

The language and cultural barriers also make it difficult for overseas investors to do research on startups and guide them in business development, said Yoshino.

Given the shortage of pre-IPO funding, many Japanese ventures have gone public on the Mothers market of the Tokyo Stock Exchange at an early stage. The small-company board is known for its low entry barriers, but also a retail-dominated investor base.

Once listed, companies often get stuck with a market value below $300 million and limited trading volume -- too small to attract global investors, said Kensuke Murashima, an ex-Morgan Stanley banker who heads Minerva alongside former Goldman Sachs Group Inc. technology deal-maker Kei Nagasawa.

The duo speak from experience. Nagasawa became chief financial officer of Mercari Inc., Japan’s first unicorn. At Morgan Stanley, Murashima advised on landmark mergers and IPOs, including those of Line Corp. and Mercari.

In the past five years, big Japanese corporations’ search for growth, technology and ways to fend off potential competition have spurred the domestic venture capital industry, according to Kumar and Ciganer.

Other market entrants include Hong Kong-based hedge fund firm Anatole Investment Management, which joined an August 2020 financing round for e-commerce and payment company Hey Corp. Another payment services provider, Paidy, raised money in 2019 and earlier this year from investors including Soros family offices and Hong Kong-based Tybourne Capital Management.

Investors have been enticed by past successes. Raksul Inc., a printing company that raised money from investors including Fidelity, has tripled its share price since going public in May 2018. Mercari’s shares have more than doubled from the end of 2019. Freee has jumped five times since its December 2019 IPO.

The groundswell of promising companies got an extra push from Covid-19. The pandemic heightened how far the country has fallen behind in areas including e-commerce, cashless transactions and work-from-home infrastructure. Prime Minister Yoshihide Suga set up a Digital Agency to implement top-down reform.

“Certainly with Covid and the digitalization policies that the government is looking to implement from this fall, it is really putting Japan on the map for a lot of investors,” said Yoshino.

©2021 Bloomberg L.P.