Exxon’s Billions Could Spawn a Permian Monster

Exxon’s Billions Could Spawn a Permian Monster

(Bloomberg Opinion) -- Exxon Mobil Corp. took four hours on Wednesday morning to tell investors: “Hold on a bit, we got this.”

But investors aren’t in a patient mood with high-spending oil and gas companies, and Exxon’s capital-expenditure budget — summary: not much change from $35 billion a year — drew the unsurprising response. Yet, looking beyond the next couple of years, Exxon provided a lot for everyone, investors and competitors, to chew on.

Exxon is doing nothing less than an overhaul of the portfolio, as might be expected after a few years of setbacks. When you’re this big — the size of an OPEC producer — that costs money. Exxon projects it will generate $190 billion of free cash flow through 2025, equivalent to almost 60 percent of its current market cap and implying $90 billion after dividends potentially available for buybacks. However, eyeballing the fuzzy bars on Exxon’s deck, that capacity doesn’t start coming through in earnest until 2021.

The fact that Chevron Corp., which held its own analyst day on Tuesday, is already buying back stock and yielding more on near-term payouts is where much of the interest in Exxon ends in the current environment. But there are implications from Exxon’s numbers that shouldn’t be ignored.

Exxon’s guidance implies cash from operations almost doubling by 2025 to $60 billion. Coincidental or not, that would match the peak reached in 2008. Production is projected to be higher; the fuzzy bars suggest annual increases of 3 to 4 percent through 2025. Even so, that level of cash flow would be astounding at a $60 oil-price assumption compared with the $100-a-barrel that prevailed in 2008 (don’t forget U.S. natural gas averaged almost $9 per million BTU that year, too).

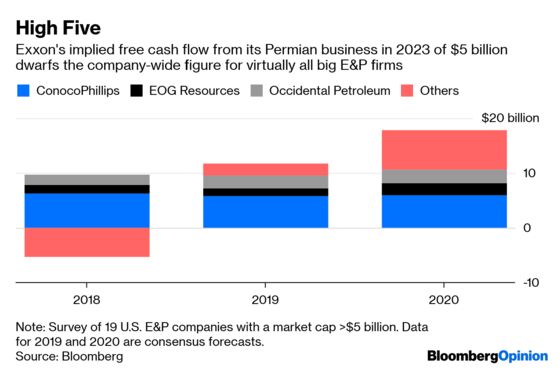

The most striking detail beneath these headline projects concerned, of course, the Permian basin. As with Chevron, Texas is at the center of Exxon’s strategic plan. The biggest question hanging over the majors is whether they can take shale, the preserve of the smaller E&P companies, and make it generate the free cash flow needed to fund dividends. Exxon says its Permian position will fund its capex by 2021 and actually generate $5 billion of free cash flow after capex in 2023.

That was far from being the biggest number in Exxon’s presentation. Consider this, however: Only one U.S. E&P company makes $5 billion of free cash flow across its entire business today (ConocoPhillips). The next two biggest generators of free cash flow — Occidental Petroleum Corp. and EOG Resources Inc. — made less than $2 billion each in 2018. Screening E&P companies with a market cap of $5 billion or more on the Bloomberg Terminal, Exxon’s projected $5 billion of free cash flow from its Permian business alone in 2023 would be almost as big as all 18 companies other than Conoco. It is just a huge number.

Is it a realistic number? If Exxon hits its projected production of somewhere around 1.1 to 1.2 million barrels of oil equivalent per day by 2023 (according to the fuzz-o-scope) then ... maybe (see the math below). But that depends a great deal on Exxon’s contention that its upfront investment in infrastructure in the Permian basin and Gulf Coast, as well as a dollop of experience-curve benefits, proves right.

It would be foolish to discount Exxon’s ability to bring its “machine” to bear. However, the company’s track record with production-growth targets is spotty at best. And, as with its peers, the performance of the past decade or so has put a big dent in Exxon’s reputation for discipline and rock-solid returns. That’s why four hours of explaining that big upfront check left the market unmoved on Wednesday morning. But it’s also why other stakeholders — frackers and OPEC, say — should lace their skepticism with a healthy dose of nervousness about what could be coming down the pipe.

Assume output of 1.15 million barrels-equivalent a day, at 60 percent oil and 40 percent natural gas. Assume $60 oil and $3 gas for a blended price of $43 per barrel-equivalent. Assume $20 per barrel of cash operating expenses and royalties.This generates cash from operations of about 9.7 billion (in line with Exxon's fuzzy bar chart on slide 51). Then assume 40 rigs operating at $120 million each per year, and that leaves just under $5 billion. All of these numbers are, like Exxon's fuzzy bars, subject to change/adjustment/scathing criticism.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.