Extreme Caution Is Often the Rally's Best Friend

Extreme Caution Is Often the Rally's Best Friend

(Bloomberg) --

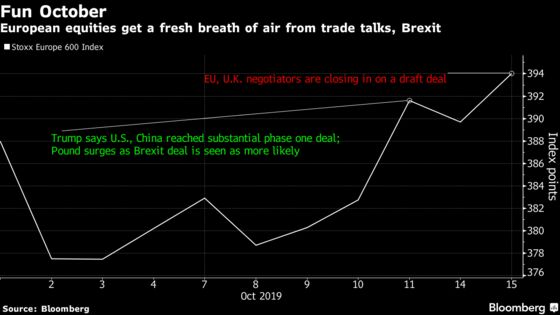

Just when the debate was heating up over whether the sell-off of early October was a correction or the start of a bigger rout, European equities are rallying again to year highs, boosted in part by mounting expectations of a Brexit deal. When negative market sentiment and positioning become extreme, contrarian investors take note.

That’s what happened in equity markets in the past few days: with so many investors sitting on cash and seeking a haven in bonds, a couple of friendly headlines about U.S.-China trade talks and Brexit negotiations caught most investors off guard and quickly fueled a recovery. And Tuesday’s news that the EU and U.K. negotiators are closing in on a deal gave even more fire to the bulls.

“There’s a really big bull market in pessimism at the moment,” says Joseph Little, global co-chief investment officer of multi-asset at HSBC Global Asset Management. “We see that all the time with our peers: cautious positioning, underweight in equities and risky credit. The odds of reaping rewards by taking the opposite view look very attractive right now.”

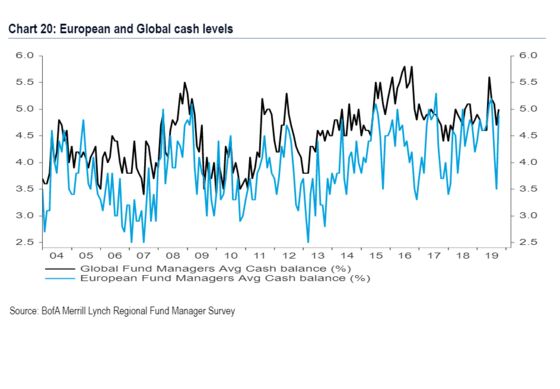

The latest fund manager survey by the Bank of America showed that their exposure to cash increased in October, continuing the influx of $322 billion into money market funds over the past six months, the largest flight to safe assets since the 2008 financial crisis. And to BofA strategists, just like HSBC AM, this extreme pessimism has been a contrarian buy signal for months.

HSBC AM’s Little is buying developed-market stocks, including cyclical companies that are sensitive to economic growth and “attractively” priced. He also says U.K. stocks are “very interesting” thanks to their high dividend yields and excessive investor anxiety, making them appealing to international buyers.

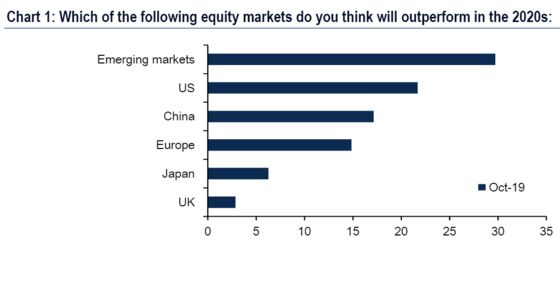

The fund managers surveyed by BofA this month didn’t share HSBC AM’s enthusiasm, with respondents forecasting U.K. stocks as having the lowest chances of outperformance among major equity markets over the next decade. But this sentiment may be changing now as traders on Tuesday embraced the optimism over the progress in Brexit negotiations by piling into the shunned region.

Read: Investors Praise Brexit Talks Progress by Buying Scorned Stocks

The FTSE 250 Index was the main beneficiary from the optimism, surging as much as 1.9% and closing at the highest level in a year. But the news also helped boost sentiment for European equities overall, with the Stoxx Europe 600 Index jumping to the highest since May 2018.

At a time when a single tweet can change the entire investment community’s mood, it’s important to maintain a cool head and a balanced portfolio, according to State Street Bank’s Ben Jones. There are still many thorny trade issues that the U.S. and China need to agree on and U.K.’s Boris Johnson is racing against the clock with just two weeks left until the Brexit deadline.

“Sentiment sits on a knife edge, it certainly has been a fickle beast this year,” said Jones, a senior multi-asset strategist at State Street Bank in London. “The stock market can do well but only if there is deliverance on the hope that Chinese-U.S. tensions ease further and tariffs are not escalated. It is not clear to me yet that everything is quite as rosy as the market is making out.”

In the meantime, Euro Stoxx 50 futures and S&P 500 contracts are down 0.3% ahead of the European open.

- Watch the pound and U.K. stocks as a Brexit deal is inching closer to being agreed to, with the U.K. said to have made a series of concessions in order to get on the same page as the European Union — yet as one has become acutely accustomed to, hurdles remain. U.K. assets have been jumping for joy so far.

- Watch stocks sensitive to U.S.-China trade tensions after China said it would retaliate with unspecified “strong countermeasures” if U.S. lawmakers enact legislation in support of Hong Kong protesters. Watch miners, steelmakers, semiconductors, autos and other cyclical segments like industrials and chemicals.

COMMENT:

- “European equities are back to YTD highs, but further upside is possible into year-end if trade and Brexit outcomes turn out to be successful,” Barclays strategist Emmanuel Cau writes in a note. “A prolonged tariff pause could help the bottoming out in manufacturing and provide a lift to cyclicals. A Brexit breakthrough seems increasingly likely and could boost sentiment towards domestic Europe, particularly financials. While headline risks remain elevated on both fronts, we think it is prudent to cut some of our defensive hedges and add to U.K. domestics.”

NOTES FROM THE SELL SIDE:

- H&M is in a positive feedback loop and the retailer’s dividend looks more secure, Handelsbanken says, upgrading the stock to hold from sell, and boosting PT to SEK210 from SEK135.

- Wacker Chemie’s guidance cut isn’t especially a shock, although the magnitude is quite substantial with it implying a reduction of about 10% to FY19 Ebitda consensus, Morgan Stanley (equal-weight) writes in a note.

- Soitec’s 2Q update was encouraging and growth remains strong for the French specialty electronics firm, though comparatives will get tougher in 2H, analysts say.

- Glaxo shares have probably found a floor and there is finally a path toward EPS growth, Intron Health says in note as raises to hold from sell.

COMPANY NEWS AND M&A:

- Woodford to Shutter Firm as Manager’s Ouster Caps Stunning Fall

- Signify to Buy Cooper Lighting From Eaton for $1.4 Billion

- ASML 4Q Sales View Beats Est., Revises Dividend Policy (1)

- Roche Narrows Sales Growth View to Upper Band of Prior View (1)

- Rio Lowers FY Alumina, Bauxite Targets; Iron Ore Unchanged (1)

- European Car-Sales Jump Masks Gloomy Outlook Blighted by Economy

- Credit Suisse Looks to Add More Advisers to Billionaire Clients

- Ipsen to License Blueprint Medicine for Up to $535 Million

- TomTom Boosts Full Year Adjusted EPS Forecast, Beats Estimates

- Atlantia Confirms Intention to Join Alitalia Rescue Group

- Wacker Chemie Lowers 2019 Ebitda, Sales Forecasts (1)

- UBS Chairman Axel Weber Criticizes Recent ECB Decisions: FAZ

- Mediaset Espana Says Withdrawal Rights Exercised on 39m Shares

- Telekom Austria Third Quarter Ebitda EU439 Mln, +13% Y/y

- Next CEO Wolfson Sells GBP10.1m Worth of Shares

- Casino Group Completes Sale of Assets to Apollo for EU465M

- Soitec 2Q Rev. EU139m, Organic Growth 40%

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 395.1 (July high); 397.9 (June 2018 high)

- Support at 381.6 (50-DMA); 377.8 (200-DMA); 365.5 (50% Fibo)

- RSI: 60.7

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,596 (May 2018 high); 3,687 (January 2018 high)

- Support at 3,519 (76.4% Fibo) 3,451 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 62.5

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Covivio raised to buy at SocGen; PT 110 euros

- Go-Ahead raised to buy at HSBC; PT 2,400 pence

- Munich Re raised to buy at Commerzbank; PT 265 euros

- Scor raised to buy at Commerzbank; PT 42 euros

- UCB raised to buy at Citi

- XXL raised to neutral at SpareBank; PT 17 kroner

DOWNGRADES:

- Brenntag Cut to Sell at ABN Amro Bank

- CaixaBank cut to hold at HSBC; PT 2.60 euros

- Encavis cut to hold at Berenberg

- Hugo Boss cut to hold at LBBW; PT 40 euros

- Immofinanz cut to sell at SocGen; PT 23 euros

- Infineon Cut to Sell at SocGen; PT 15.50 euros

- Magseis Fairfield ASA Cut to Neutral at SpareBank; PT 6 kroner

- XXL cut to sell at SEB Equities; PT 15 kroner

INITIATIONS:

- Beiersdorf re-initiated sell at Berenberg; PT 97 euros

- Cleanbnb rated new outperform at EnVent S.p.A.; PT 2.76 euros

- FinecoBank Rated New Buy at HSBC; PT 11.20 euros

- L’Oreal re-initiated hold at Berenberg; PT 237 euros

- Reckitt re-initiated buy at Berenberg; PT 7,420 pence

- Shop Apotheke rated new overweight at Barclays; PT 45 euros

- Spectris Reinstated Hold at Liberum; PT 2,400 pence

- Tritax Big Box rated new hold at Peel Hunt; PT 150 pence

- Zur Rose rated new overweight at Barclays; PT 120 Swiss francs

MARKETS:

- MSCI Asia Pacific up 0.5%, Nikkei 225 up 1.2%

- S&P 500 up 1%, Dow up 0.9%, Nasdaq up 1.2%

- Euro up 0.01% at $1.1034

- Dollar Index up 0.02% at 98.31

- Yen up 0.16% at 108.69

- Brent up 0.2% at $58.8/bbl, WTI up 0.2% to $52.9/bbl

- LME 3m Copper down 0.3% at $5756/MT

- Gold spot up 0.2% at $1483.8/oz

- US 10Yr yield down 3bps at 1.74%

ECONOMIC DATA (All times CET):

- 10am: (IT) Aug. Industrial Sales WDA YoY, prior -0.6%

- 10am: (IT) Aug. Industrial Sales MoM, prior -0.5%

- 10am: (IT) Aug. Industrial Orders NSA YoY, prior -1.0%

- 10am: (IT) Aug. Industrial Orders MoM, prior -2.9%

- 10:30am: (UK) Sept. CPIH YoY, est. 1.8%, prior 1.7%

- 10:30am: (UK) Sept. CPI MoM, est. 0.2%, prior 0.4%

- 10:30am: (UK) Sept. CPI YoY, est. 1.8%, prior 1.7%

- 10:30am: (UK) Sept. CPI Core YoY, est. 1.7%, prior 1.5%

- 10:30am: (UK) Sept. Retail Price Index, est. 291.5, prior 291.7

- 10:30am: (UK) Sept. RPI MoM, est. 0.0%, prior 0.8%

- 10:30am: (UK) Sept. RPI YoY, est. 2.7%, prior 2.6%

- 10:30am: (UK) Sept. RPI Ex Mort Int.Payments (YoY), est. 2.7%, prior 2.6%

- 10:30am: (UK) Sept. PPI Input NSA MoM, est. 0.2%, prior -0.1%

- 10:30am: (UK) Sept. PPI Input NSA YoY, est. -1.7%, prior -0.8%

- 10:30am: (UK) Sept. PPI Output NSA MoM, est. 0.1%, prior -0.1%

- 10:30am: (UK) Sept. PPI Output NSA YoY, est. 1.3%, prior 1.6%

- 10:30am: (UK) Sept. PPI Output Core NSA MoM, est. 0.1%, prior 0.2%

- 10:30am: (UK) Sept. PPI Output Core NSA YoY, est. 1.9%, prior 2.0%

- 10:30am: (UK) Aug. House Price Index YoY, est. 0.6%, prior 0.7%

- 11am: (EC) Aug. Trade Balance SA, est. 18b, prior 19b

- 11am: (EC) Aug. Trade Balance NSA, prior 24.8b

- 11am: (EC) Sept. CPI Core YoY, est. 1.0%, prior 1.0%

- 11am: (EC) Sept. CPI MoM, est. 0.2%, prior 0.1%

- 11am: (EC) Sept. CPI YoY, est. 0.9%, prior 1.0%

- 11am: (IT) Sept. CPI FOI Index Ex Tobacco, prior 103.2

- 11am: (IT) Sept. CPI EU Harmonized YoY, est. 0.3%, prior 0.3%

--With assistance from Michael Msika.

To contact the reporter on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh

©2019 Bloomberg L.P.