Extinction of Bond Vigilantes Spurs Risk Bulls Around the World

Extinction of Bond Vigilantes Spurs Risk Bulls Around the World

(Bloomberg) -- Deep in the underbelly of the nearly $16 trillion Treasury market, you’ll find the secret behind the rally sweeping risk assets across the globe.

It’s opaque, notoriously hard to measure and right now it means everything for markets.

Known as the term premium, the compensation investors demand to hold long-term government bonds over short-term debt has fallen close to levels last seen in the Brexit bloodbath of 2016 -- when fierce haven demand sent U.S. Treasury yields to record lows.

Its latest collapse lies at the heart of the resurgence of the bull market even as Wall Street frets a brewing economic downturn: Investors don’t think bonds, the Federal Reserve nor inflation are their enemy.

Whatever the exact reason behind the return to an ultra-negative premium, it’s juicing stock valuations and refueling the hunt for yield along the way.

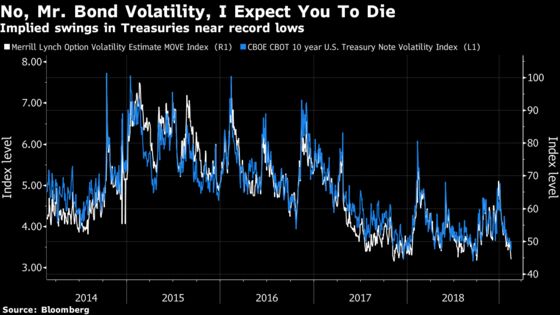

To cap it off, the implied volatility of U.S. Treasuries, across the curve and at the 10-year tenor in particular, are close to record lows -- crimping cross-asset price swings.

“Seeing bond market stability on a consistent basis is the equity market’s best friend,” said Michael Purves, chief global strategist at Weeden & Co. “Bond-market stability facilitates risk appetite when whatever fear factor embedded in owning a long-dated Treasury is eroded.”

The sluggish economic backdrop, the dovish shift by major central banks, and lack of momentum or volatility in inflation across advanced economies have left money managers more willing to buy longer-duration Treasuries.

With the resulting rally spurring fewer rewards from holding long-term safe assets, investors are being forced to seek out riskier income streams. Substantial inflows in recent weeks into mortgage-backed securities, credit, emerging-market bonds, and real-estate investment trusts “show ‘yield’ the investment theme winner of 2019,” write Bank of America Merrill Lynch strategists led by Michael Hartnett.

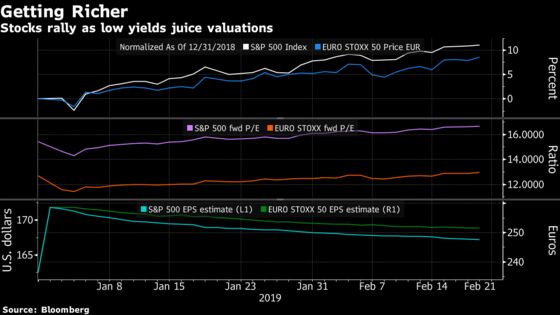

Juiced Valuations

A drop in the term premium, all else equal, pushes Treasury yields downwards. It also means a lower rate at which future corporate earnings are discounted -- fuel for higher price-to-earnings ratios.

Stephane Barbier de la Serre at Makor Capital Markets points to European equities as an example. Outflows from the region have picked up, with Bank of America Merrill Lynch noting the second-largest weekly outflow on record this month. And yet that hasn’t stopped the market from edging higher. The answer is higher valuations, supported by persistently low rates, the strategist said.

Indeed, the new-year bull advance in the S&P 500 Index and Euro Stoxx 50 are functions of a rising price-to-earnings multiple that more than offsets the decline in expected earnings per share -- a rally that has the term premium’s fingerprints all over it.

Falling corporate borrowing costs also help support companies’ firepower for debt-fueled buybacks to support share prices.

No Permanent Panacea

It’s obviously not all good news. A low term premium may bolster valuations, but it also reflects relative pessimism about nominal growth.

“A consistently higher multiple, with lower earnings growth, is the logical outcome of a deeply negative term premium,” said Dennis Debusschere, the head of portfolio strategy at Evercore ISI in New York. “So total return profile of the market might not be meaningfully different than the past. It could even be lower, which I suspect it will be.”

But higher-than-normal valuations seem fair given this backdrop, he reckons.

And the market may have the outlook for inflation and monetary policy all wrong. The severely depressed levels of the term premium and interest-rate volatility suggest that a reversal would be unexpected and most likely painful.

Danger Zone

Look no further than 2018’s two major equity drawdowns as a reminder. The biggest one-day jump in volatility on record in February was preceded by a report showing U.S. wage growth was beginning to heat up -- with fiscal stimulus in the pipeline poised to further stoke price pressures. The fourth-quarter stock rout also had its genesis in Fed Chair Jerome Powell’s remark that policy rates were a “long way” from neutral.

It’s not hard to see hazards out there.

“Inflation proxies are on the move,” according to Nomura Securities cross-asset strategist Charlie McElligott. Green shoots from China, like record new credit creation and Caterpillar Inc.’s comment that it’s seeing “strong” demand from the world’s second-largest economy, “risk ‘tipping over’ the market’s consensual belief in ‘the death of inflation,’” he added.

And even if the world remains locked in a slow-growth, lowflation regime, it’s doubtful the term premium can serve as an enduring panacea for equity bulls.

“Does it mean the markets can only go higher?” said Francois Savary, chief investment officer at Prime Partners SA in Geneva. “There’s a kind of complacency building.”

To contact the reporters on this story: Luke Kawa in New York at lkawa@bloomberg.net;Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Sid Verma, Samuel Potter

©2019 Bloomberg L.P.