Europe's Beleaguered Banks: Five Things to Monitor Into 2019

Europe's Beleaguered Banks: Five Things to Monitor Into 2019

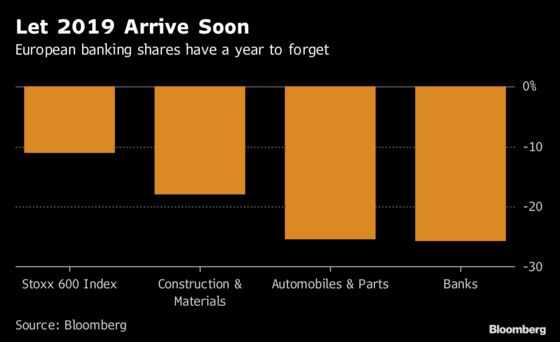

(Bloomberg) -- European banks shares are about to close a year most investors would be happy to have skipped. With a 26 percent drop, the biggest in seven years, the Stoxx 600 Banks Index is the worst-performing sector in the region.

A combination of political woes, emerging-market uncertainties, company-specific issues, and the lack of interest rates hikes have been the perfect cocktail to wipe out more than 300 billion euros ($340 billion) of shareholders’ money from January. Here are five things for investors to watch going into 2019 to decide whether or not to sit the sector out:

Regulation

New rules have increasingly affected financial institutions over the decade since the financial crisis and 2019 will be no different. With Basel III’s implementation in 2022, banks are already preparing for any potential inflation of risk-weighted assets that may affect their ability to return capital to shareholders. And as we enter the second year of MiFID II regulation, some say the full impact of those rules is still to come.

While politicians reassure markets they’re prepared for a deal or no-deal Brexit in terms of financial oversight, the U.K.’s divorce from the European Union is set cause more friction in regulation either way. Already, international differences and gaps in rules are consuming executives’ time and costing capital amounting to an average of 5 percent to 10 percent of annual turnover, according to the International Federation of Accountants and Business at OECD.

Meanwhile, time is running out for the overhaul of Eonia and Euribor as the life of the money market benchmarks is set to be restricted at the start of 2020. Banks are lobbying for extra time because their chosen replacement rate may not be up and running until next October. A smooth transition is critical to financial markets with trillions of euros in derivative contracts and intra-bank lending tied to the benchmarks.

Finally, any word from the regulator regarding more restrictions or supervision following the money-laundering scandal at Danske Bank A/S should be on the watch list.

Mergers

Deutsche Bank AG and Commerzbank AG, as well as a possible cross-border merger of Italy’s UniCredit SpA and France’s Societe Generale SA, are two high-profile combinations that have constantly been speculated upon this year -- and that chatter is likely to continue in 2019.

Big mergers are seen by some as a last resort to improve bottom-lines and cut costs on a larger scale, while analysts also question whether a merger can really solve the problems of bad assets or the lack of a sustainable business model.

Chances for smaller scale mergers look better, and the highly fragmented German banking market may experience some consolidation in the new year. Spanish medium-sized banks Unicaja Banco SA and Liberbank SA are already in talks on a possible tie up and smaller U.K. lenders, striving to challenge bigger competitors, may combine as margins come under pressure.

New Banks

Banks will continue to feel the heat of competition from fintechs as many of the startups may be able to steady their business model and expand into new markets and business areas. While payment transaction companies have become an established sub-sector with market valuations going into the billions, other areas like current accounts, brokerage or asset management are still relatively small -- for now. Banks will need to spend billions to invest in their older infrastructure to keep up.

Some fintechs like Berlin-based Solarisbank AG or N26 are mulling plans for listings or additional finance rounds next year and those funds will probably used for expansion. However it also opens the chance that larger banks may consider deals to buy into a technology leader.

It might also be worth keeping an eye on Asia where 13 fintechs have accumulated a total valuation of $217 billion, a recent study found. While entry barriers mainly in the form of domestic regulation aren’t to be underestimated, it’s likely that viable business models will rapidly gain the financial backing to compete.

Credit Risk and Costs

Historically low provisions helped drive the profitability of companies in 2018. But with the economic outlook dimming, there’s a risk this may be about to turn. In November, Morgan Stanley analysts said that a slowing economy and the credit cycle are key into 2019. “We are selective and look for structural resilience to a downturn and dividend underpin,” analysts including Magdalena Stoklosa said.

Meanwhile although lenders need to invest in technology, many will try to keep their costs in check. The gap between revenue growth and cost growth, the so-called operating jaws, should widen in 2019, Bloomberg Intelligence analyst Georgi Gunchev said in November. Barclays Plc, Danske, Credit Suisse Group AG and Royal Bank of Scotland Group Plc should deliver comfortably, which could lead to some positive earnings surprises, according to Gunchev.

ECB & Rates

Lending remains one of the main activities for most European banks and with interest rates at zero, margins for that part of the business are being squeezed. The European Central Bank has repeatedly said there will be no hikes before the end of next summer and President Mario Draghi said last week that the ECB is monitoring how low rates affect banks’ profitability.

Interest rates hikes would be more than welcome for banks such as Spain’s CaixaBank SA, which last month raised its profitability targets for the next three years based on an assumption that the Euribor 12-month rate will rise 90 basis points to 0.7 percent by 2021.

Meanome market participants expect the central bank to hold still even longer. Commerzbank said it expects the ECB to only make a move in the first quarter of 2020, while Fitch Ratings Ltd. has said that “downgrades to the euro-zone growth outlook and stubbornly low core inflation now look likely to persuade the ECB to hold off from raising interest rates until 2020.”

Meanwhile about 722 billion euros of longer-term loans granted to banks by the ECB start maturing from 2020, and some replacement funds may be needed next year. To support lending to households, new rounds of the central bank’s targeted longer-term refinancing operation could be in the cards.

On Wednesday, we’ll take a look at five things to watch out for in European consumer stocks.

To contact the reporters on this story: Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net;Macarena Munoz in Madrid at mmunoz39@bloomberg.net

To contact the editors responsible for this story: Beth Mellor at bmellor@bloomberg.net, Jon Menon, Celeste Perri

©2018 Bloomberg L.P.