Europe May Not Want to Go Where the Sun Rises

Europe May Not Want to Go Where the Sun Rises

(Bloomberg) --

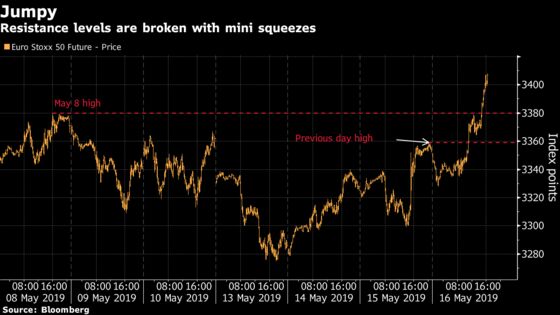

In a short-sighted market, macro news, tweets and technical levels regularly trigger little sell-offs and short squeezes. We just had a lot of examples in the past few weeks. When taking a step back from the noise and fluctuations however, like it or not the big picture keeps pointing toward the “Japanification” of Europe -- with a few twists.

Macro-economic similarities between Europe and Japan are well-established: low growth, low inflation and low yields to name a few. Demographics have been converging too. Whether the situation will become structural remains to be seen, but the impact on the equity market has already materialized in some aspects.

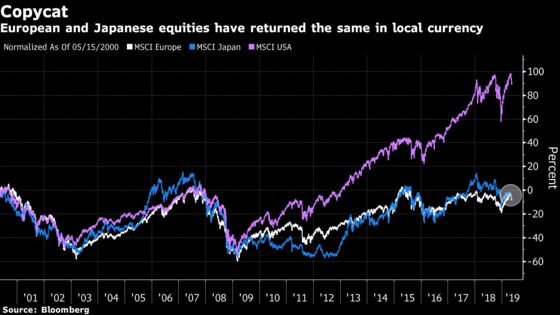

European and Japanese equities have roughly returned the same in price over 20 years, as outlined by Bloomberg Intelligence analysts Laurent Douillet and Tim Craighead, marking a stark contrast to the U.S. However, in total return and dollar terms at least, European equities materially outperformed Japan.

Of course, there are a few differences. If Europe is vulnerable to Japanification, it’s not there yet, according to BNP Paribas strategists. Wage and core Consumer Price Index growth are still above 1% in the euro area, and its prospects for inflation are better than Japan’s were in the early 1990s. The ECB expansionist policy has certainly helped, but there is little wriggle room left, especially in the event of a negative shock. The key could lie with further EU political integration and fiscal convergence, as an additional tool to monetary policy, BNP Paribas says.

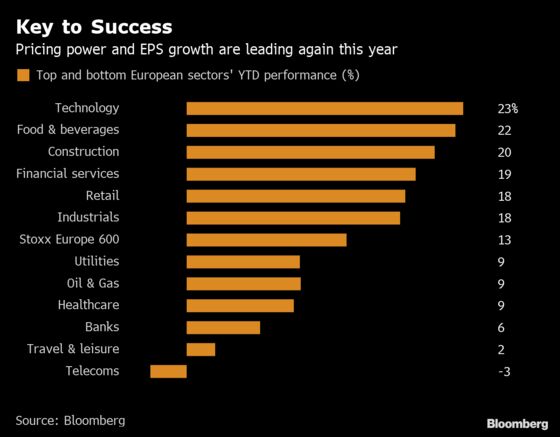

For equities, this is part of the reason why sectors like food & beverages or technology are more attractive than banks for most investors. As long as inflation expectations, interest rates and bund yields stay low, banks are unlikely to outperform. Defensive features and superior growth are more appealing than depressed valuations. Looking at the chart below, this year has been no exception.

“During the last 11 years, health care and food and beverage companies were able to increase prices above the EU core CPI, leading to earnings-per-share growth of 68% and 94%, respectively, while sectors with no pricing power (utilities and telecoms) have seen an EPS decline,” Bloomberg Intelligence strategists write. The exception was technology, which managed high earnings growth despite low pricing power.

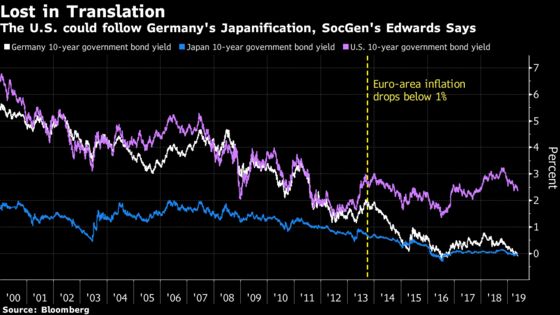

As for what could come next, Societe Generale strategist Albert Edwards sees the U.S. moving on the same path as Japan and Europe, with all three 10-year yields converging to -1% in the next recession. The U.S. will be hit hard, with new cyclical lows in both U.S. P/Es and bond yields, in a similar way to Japan, according to Edwards.

It’s something to monitor in the longer run. In the meantime, Euro Stoxx 50 futures are trading down 0.5% ahead of the open this morning, following a mixed session for equities in Asia.

- Watch takeout delivery companies after Amazon confirmed it will lead a new funding round for Deliveroo. Watch Just Eat, Delivery Hero and Takeway.com along with U.K.-based pizza delivery firm Domino’s Pizza.

- Watch miners after iron ore prices in Singapore and China surged as investors expect a supply crunch. Watch BHP, Rio Tinto, Anglo American and Ferrexpo among miners and keep an eye on steel stocks including ArcelorMittal, Tenaris and Evraz.

- Watch semiconductor makers and chip-equipment firms following relatively upbeat results from U.S. firms Nvidia and Applied Materials. On the chipmaker side, watch the likes of Infineon, AMS, STMicroelectronics and Dialog Semi for any read across; on the chip equipment front, watch the likes of ASML, ASM International and BE Semiconductor.

- Watch the pound and U.K. stocks after Boris Johnson, the Brexit-backing former U.K. foreign secretary and mayor of London, was named favorite by bookies to replace Theresa May as prime minister.

COMMENT:

- “Global equity markets continue to under-estimate the relentless expansion of the U.S.-China trade dispute,” Jefferies strategists write in a note. “The progression from tariffs to direct actions against single Chinese companies and their inter-linked supply chains has a wide-ranging impact on profitability that investors will find difficult to quantify.”

COMPANY NEWS AND M&A:

- Amazon Confirms Leading $575M Funding Round in U.K.’s Deliveroo

- Total Eyed Anadarko Assets for a Year Before $8.8 Billion Deal

- Richemont Full Year Operating Profit Misses Estimates

- ADP, FDJ Privatization Approved by French Constitutional Court

- Cevian Selling $614 Million Stake in Logistics Firm DSV

- Vallourec CFO Says Company Doesn’t Need Capital Increase

- Vallourec 1Q Ebitda Beats Avg. Est., Keeps Target

- Atlas Copco CEO Says M&A Needed to Reach Growth Target: DI

- European Bank Consolidation Could Provide Stability: Buba’s Buch

- Metro Bank Intends to Raise GBP350m in Placing at 500 Pence/Shr

- EDP First Quarter Net Income Misses Lowest Estimate (1)

- D’Ieteren Raises View, Sees Pretax Profit Growth at Least 25%

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 382.9 (50-DMA); 385.7 (76.4% Fibo)

- Support at 374.5 (61.8% Fibo); 369.2 (200-DMA)

- RSI: 49.7

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,516 (76.4% Fibo); 3,596 (May 18 high)

- Support at 3,404 (50-DMA); 3,309 (50% Fibo)

- RSI: 53

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- ALD Upgraded to Buy at Deutsche Bank

- Anglo American Upgraded to Buy at Liberum

- Atresmedia upgraded to overweight at JPMorgan; PT 6.10 Euros

- DWS Upgraded to Buy at Commerzbank; PT 35 Euros

- Mediaset upgraded to neutral at JPMorgan; PT 2.90 Euros

- Rio Tinto Upgraded to Buy at Liberum

- Schibsted upgraded to buy at Kepler Cheuvreux; PT 260 Kroner

- SEB Upgraded to Buy at Deutsche Bank

- TF1 upgraded to overweight at JPMorgan; PT 12.60 Euros

DOWNGRADES:

- Bankia downgraded to add at AlphaValue

- Carmila downgraded to reduce at Kepler Cheuvreux; PT 18 Euros

- Generali downgraded to hold at Kepler Cheuvreux; PT 17.50 Euros

- Informa downgraded to neutral at JPMorgan; PT 8.11 Pounds

- PostNL downgraded to hold at Jefferies; PT 2 Euros

- Ubisoft downgraded to hold at Midcap Partners; PT 90 Euros

- Umicore downgraded to hold at ABN Amro Bank; PT 30 Euros

- Wendel downgraded to hold at SocGen; PT 135 Euros

- Wolters Kluwer cut to underweight at JPMorgan; PT 57 Euros

INITIATIONS:

- BASF rated new hold at Pareto Securities; PT 65 Euros

- Beazley rated new overweight at Morgan Stanley; PT 6.51 Pounds

- Buzzi Unicem rated new buy at Citi

- Hannover Re rated new overweight at Morgan Stanley

- Hurricane Energy rated new equal-weight at Barclays; PT 75 Pence

MARKETS:

- MSCI Asia Pacific down 0.5%, Nikkei 225 up 1%

- S&P 500 up 0.9%, Dow up 0.8%, Nasdaq up 1%

- Euro down 0.01% at $1.1173

- Dollar Index down 0.03% at 97.83

- Yen up 0.19% at 109.64

- Brent up 0.1% at $72.7/bbl, WTI up 0.2% to $63/bbl

- LME 3m Copper down 0.8% at $6053/MT

- Gold spot up 0.1% at $1287.9/oz

- US 10Yr yield down 1bp at 2.38%

MAIN MACRO DATA (all times CET):

- 11am: (EC) March Construction Output MoM, prior 3.0%

- 11am: (EC) March Construction Output YoY, prior 5.2%

- 11am: (EC) April CPI Core YoY, est. 1.2%, prior 1.2%

- 11am: (EC) April CPI MoM, est. 0.7%, prior 1.0%

- 11am: (EC) April CPI YoY, est. 1.7%, prior 1.7%

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.