Europe Banks Are ‘Hostage’ to ECB’s Dovish Stance

Europe Banks Are ‘Hostage’ to ECB’s Dovish Stance

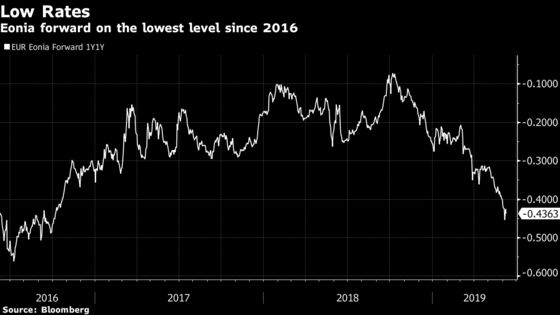

(Bloomberg) -- With Europe’s economic growth showing more cracks and inflation not moving in the desired direction, the ECB once again opened the door to further easing last week. Investors are worried it will continue to suck out any brightness from the banking sector’s outlook like a black hole.

After a disappointing May that saw bank stocks retreat to the levels of early January, the ECB’s commentary on Thursday -- that rates will stay lower for longer -- put pressure on the lenders’ stocks once again. What’s more, a new round of cheap funding for banks might not change the big picture.

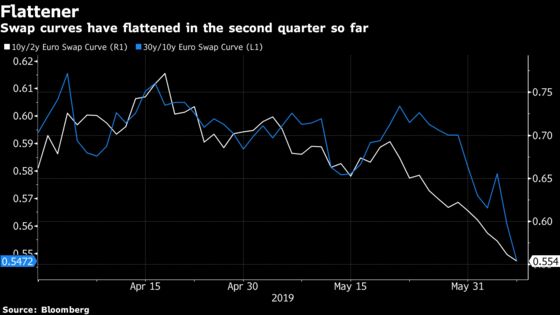

Analysts at JPMorgan led by Kian Abouhossein see the sector as a “hostage” to the central bank’s dovish stance and expect a 2% negative earnings per share impact with every 25 basis points additional rate cut. And don’t forget the ever flattening yield curve in the second quarter, implying another 2% to 3% of earnings per share are gone, according to JPMorgan.

The central bank didn’t provide clear guidance on the chances of introducing so-called tiering, or the exemption of some lenders’ deposits at the ECB from the impact of negative rates. The message was that it remains possible, but not at present, analysts at BNP Paribas concluded. Bloomberg economist Maeva Cousin wrote that the re-calibrated rates guidance “increases the likelihood of the ECB unveiling some form of reserve tiering system soon.”

Yet, the idea that tiering will be the game changer for banks remains debatable. JPMorgan argues that a shift to even lower rates would be bad for valuations, even with tiering. They calculate a 5% positive impact on the system if all of banks’ excess reserves are exempt from negative rates, thereby merely offsetting the impact of lower rates. That said, the effects may vary from country to country and could be relatively good for German banks.

While the terms of the ECB’s new TLTRO program, designed to ensure credit flows to the economy, is considered favorable for lenders it does “not change the outlook for European banks materially,” Credit Suisse analysts led by Jan Wolter said. Still, some companies like Santander, UniCredit, BBVA or CaixaBank may benefit from continued low funding costs.

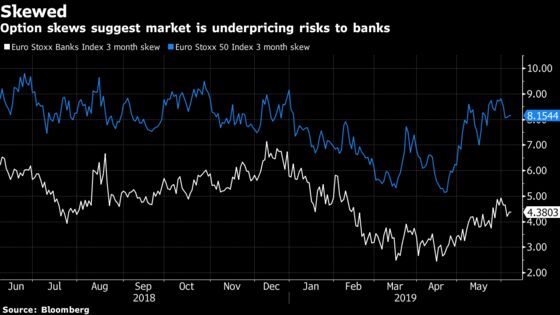

The broader sector is seen as likely to continue trading in a range, BNP Paribas said. It recommends investors look at option skews as the market is underpricing the downside risks to the banking sector.

In the meantime, Euro Stoxx 50 futures are trading 0.5% higher ahead of the open today.

SECTORS IN FOCUS TODAY:

- European stocks exposed to Mexico are likely to gain on Monday after U.S. President Donald Trump said he would drop plans for tariffs which had been planned to go into effect on Mexico on Monday. Watch automakers including Volkswagen and BMW, brewers including AB InBev and Heineken and Spanish companies including BBVA, Santander and Telefonica.

- The European defense sector is likely to be in focus following news that U.S. giants United Technologies and Raytheon are planning to merge. The news may lead to M&A speculation in the European defense industry, so watch for any read-across in shares of BAE Systems, Dassault Aviation, Rolls-Royce, Leonardo, Thales and Saab.

COMMENT:

- “Whether or not the U.S. has entered a ‘Twilight Recession Zone’ is certainly unclear but it should be remembered that every U.S. recession has been accompanied by the yield curve inverting and the curve shifting upwards,” Jefferies strategists write in a note. “It is interesting to note that the U.S. yield curve has shifted downwards, thereby easing policy quite dramatically. Hence there has been little or no evidence of credit distress to date. Real interest rates are close to zero.”

COMPANY NEWS AND M&A:

- Nissan Says Renault Plan to Abstain From AGM Vote ‘Regrettable’

- PSA Is Always Open to New Deals, CEO Tavares Tells Expresso

- Eurofins Says No Evidence of Unauthorized Theft in Cyberattack

- Roche and Spark Get FTC Request for Extra Info on Spark M&A

- Husqvarna CEO Aims for Record Operating Margin This Year: DI

- Addiko Bank Intends to Float in Vienna as Advent Sells 50%

- Cosmo Says FDA Accepts NDA Filing of Remimazolam for Review

- Deutsche Bank to Hire up to 50 Senior Traders, Bankers: FN

- Renesas, SAIC Volkswagen Open Joint Laboratory in China

- Poland’s CD Projekt to Release New Cyberpunk Game Next April

- Helical Confirms in Recent Past Got Unsolicited Approaches

- Autogrill to Spend EU1.5b on Growth Abroad: CEO to Corriere

NOTES FROM THE SELL SIDE:

- Allianz, Prudential and RSA are upgraded to buy from neutral, with Generali and Aegon lifted to neutral from sell by Citi in a note on the European insurance sector.

- A positive re-rating for Playtech is in the cards and the story is simplifying, Jefferies says, initiating coverage of the stock with a buy rating and a 570p price target that has more than 35% upside.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 382.2 (50-DMA); 385.7 (76.4% Fibo)

- Support at 374.5 (61.8% Fibo); 368.4 (200-DMA)

- RSI: 50.7

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,408 (50-DMA); 3,515 (May high)

- Support at 3,309 (50% Fibo); 3,267 (200-DMA)

- RSI: 52

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Aegon upgraded to neutral at Citi

- Allianz upgraded to buy at Citi

- Generali upgraded to neutral at Citi

- Neste upgraded to buy at Citi

- Prudential upgraded to buy at Citi

- RSA upgraded to buy at Citi

- S4 Capital upgraded to buy at HSBC; PT 1.80 Pounds

- Saipem upgraded to hold at Jefferies; PT 4.65 Euros

- Vesuvius upgraded to top pick at RBC; Price Target 7 Pounds

DOWNGRADES:

- FirstGroup downgraded to reduce at HSBC; Price Target 90 Pence

INITIATIONS:

- Playtech rated new buy at Jefferies; PT 5.70 Pounds

MARKETS:

- MSCI Asia Pacific up 0.9%, Nikkei 225 up 1.2%

- S&P 500 up 1%, Dow up 1%, Nasdaq up 1.7%

- Euro down 0.26% at $1.1305

- Dollar Index up 0.3% at 96.83

- Yen down 0.41% at 108.64

- Brent up 0.4% at $63.6/bbl, WTI up 0.5% to $54.3/bbl

- LME 3m Copper up 0.6% at $5831/MT

- Gold spot down 1% at $1327.2/oz

- US 10Yr yield up 4bps at 2.12%

ECONOMIC DATA (All times CET):

- 10am: (IT) April Industrial Production MoM, est. 0.0%, prior -0.9%

- 10am: (IT) April Industrial Production WDA YoY, est. -0.5%, prior -1.4%

- 10am: (IT) April Industrial Production NSA YoY, prior -3.1%

- 10:30am: (UK) April Monthly GDP 3M/3M Change, est. 0.4%, prior 0.5%

- 10:30am: (UK) April GDP (MoM), est. -0.1%, prior -0.1%

- 10:30am: (UK) April Industrial Production MoM, est. -1.0%, prior 0.7%

- 10:30am: (UK) April Industrial Production YoY, est. 0.9%, prior 1.3%

- 10:30am: (UK) April Manufacturing Production MoM, est. -1.4%, prior 0.9%

- 10:30am: (UK) April Manufacturing Production YoY, est. 2.0%, prior 2.6%

- 10:30am: (UK) April Construction Output SA MoM, est. 0.5%, prior -1.9%

- 10:30am: (UK) April Construction Output SA YoY, est. 3.3%, prior 3.2%

- 10:30am: (UK) April Visible Trade Balance GBP/Mn, est. £13b deficit, prior £13.7b deficit

- 10:30am: (UK) April Trade Balance Non EU GBP/Mn, est. £4.48b deficit, prior £4.36b deficit

- 10:30am: (UK) April Trade Balance, est. £4.7b deficit, prior £5.41b deficit

- 10:30am: (UK) April Index of Services MoM, est. 0.1%, prior -0.1%

- 10:30am: (UK) April Index of Services 3M/3M, est. 0.2%, prior 0.3%

To contact the reporter on this story: Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.