Europe’s Moment of Truth as Credit Investors Bid QE Farewell

Euro Zone's Moment of Truth as Credit Investors Bid QE Farewell

(Bloomberg) -- The days of quantitative easing in the euro area are long gone, according to signals from the region’s $3 trillion corporate bond market.

Investors are demanding ever-higher premiums for companies lower down the ratings spectrum over high-quality peers -- a turning point for a market long distorted by the European Central Bank juggernaut.

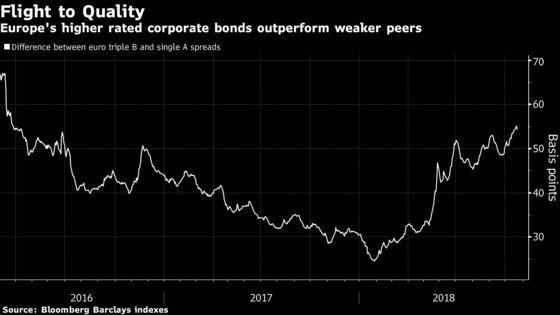

The gap between triple B and single A spreads -- the lowest and second-lowest in the high-grade tier -- is now the widest since the start of the ECB’s corporate bond purchase program, according to data compiled by Bloomberg.

In other words, portfolio managers are choosing to be selective with fresh urgency, potentially redrawing the credit landscape for Europe’s strongest borrowers along the way. It’s a sign of market health, but the latter’s capacity to absorb sell-offs is now being put to the test -- just as global stresses loom, according to money managers.

“Investors are starting to differentiate,” said Florence Barjou, head of multi-asset investment at Lyxor Asset Management, which oversees 143 billion euros ($164 billion). “There was less discrimination before because liquidity was ample. Now, people are restating their scenarios on interest rates, global growth and look more on fundamentals.”

Recent sharp losses in individual names such as Spanish supermarket chain Distribuidora Internacional de Alimentacion SA are an “unwelcome reminder” of name-specific risks, JPMorgan analysts led by Matthew Bailey wrote in a note.

Slipping Stimulus

The credit market has taken the oncoming withdrawal of stimulus largely in its stride, bolstered by the ECB’s well-telegraphed tightening plans and its pledge to reinvest maturing assets. But with spreads at the highest in more than six weeks, it comes at a challenging time for investors hit by Italian political risk, U.S.-China trade tensions and Brexit-related volatility.

One side-effect from the disappearance of an ECB backstop bid could be improved price discovery or, put simply, better interaction between buyers and sellers to determine the appropriate return of a bond. Price discovery has to some degree been distorted by the bank’s bond-buying spree, with investors having to guess the level of current or potential ECB support for an issuer.

The bid to price out the monetary backstop by year-end is also a new ball game for issuers, who’ve been lulled by ever-falling premiums in recent years, forcing buyers further down the risk spectrum.

“The transition out of the CSPP era has been accompanied by increased price dispersion and higher volatility,” Morgan Stanley strategists led by Srikanth Sankaran wrote in a note to clients. “We expect more of both.”

The monetary authority has amassed 2.5 trillion euros of bonds to anchor borrowing costs in a bid to revive growth. It’s already begun to slow purchases, snapping up some 700 to 800 million euros of corporate debt a week this month, the least since August when slumping primary sales reduced obligations available for sale.

As the market shakes off QE, active investors could emerge as winners if market participants become ever-more selective. Low dispersion in previous years encouraged inflows to low-fee exchange-traded funds. The reversal, in theory, may help this breed of fund manager outperform.

The new credit order in Europe may also have a butterfly effect for the dollar market. The prospect of more bargains closer to home might appeal to investors in the single-trading bloc, already faced with diminishing returns on U.S. securities thanks to elevated currency-hedging costs.

It all constitutes a more complex trading climate for global investors grappling with macro risks and weak returns across credit markets.

“There is a pick-up in idiosyncratic stories, risk factors like Brexit and trade, as well as fund outflows,” said Henrietta Pacquement, fund manager at Wells Fargo Asset Management.

To contact the reporter on this story: Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.