Europe’s Markets Go Into Meltdown After ECB Stimulus Disappoints

Euro Fluctutates After ECB Holds Rates in Defiance of Markets

(Bloomberg) --

Investors dumped Europe’s bonds and stocks after Christine Lagarde did little to show that the region’s central bank can stop economies from sliding into recession.

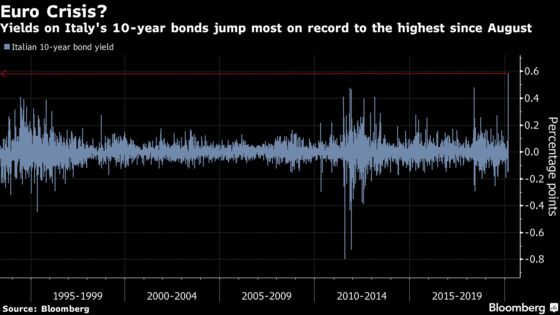

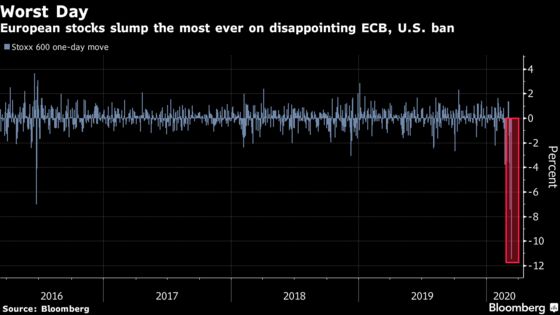

European stocks tumbled the most on record and Italian bonds plunged to send yields up the most ever, after the European Central Bank held off on cutting interest rates. The bonds of Portugal, Spain and France also slid as a boost to quantitative easing fell short of expectations, and the euro headed for its worst three-day drop since 2016.

The ECB is not here to close bond spreads, President Lagarde said in the press conference after the decision. The gap between Italian yields and their German peers, seen as a barometer of risk, climbed to the most since June.

“I didn’t realize the ECB’s primary mandate was to cause a bond market crisis,” said Peter Chatwell, head of European rates strategy at Mizuho International Plc. “This is very reminiscent of 2011, when the ECB hiked rates and were the catalyst for the peripheral debt crisis.”

Europe’s peripheral bond markets -- and France -- were expected to be the biggest beneficiaries from any boost to the ECB’s bond-buying program given their large amount of outstanding debt. While the institution announced a “a temporary envelope” of 120 billion euros ($135 billion) until the end of the year, the purchases will be focused on the private sector.

“They know they can’t do much to support the economy and they signaled that they are not here to bail out the market,” said Antoine Bouvet, senior interest-rate strategist at ING Groep NV. “Literally everything sells off when central banks do that.”

The yield on Italy’s 10-year bonds jumped as much as 72 basis points and the euro fell 1.2% to $1.1132 as of 4:55 p.m. in London. Risk-sensitive currencies plunged, with the Norwegian krone weakening past 10 per dollar for the first time as crude tumbled. The Stoxx Europe 600 Index slid 11%, with investors dumping all 19 industry groups.

The ECB decision paled in comparison to the action taken by the Bank of England and the U.S. Federal Reserve.

“After the bold action from the Fed and Bank of England, expectations were running high that the ECB would follow suit and deliver a rate cut,” said Chris Attfield, a fixed-income strategist at HSBC Holdings Plc. “This was a disappointment to a market that had already discounted more than the ECB delivered, and creditized bond markets like Italy are the place this is felt most keenly.”

No Cut

Global credit markets also came under renewed strain. The cost to insure against defaults of Europe’s riskiest companies surged to the highest since 2012 and spreads on euro investment-grade bonds widened, adding to a surge this week.

Even German bonds, the region’s main haven asset, struggled to hold on to early gains, with yields rising slightly across the curve. Earlier this week, benchmark yields touched record lows, suggesting that investors were bracing for an economic contraction and perpetually-low inflation.

There were signs that Germany may be willing to abandon its long-held commitment to a balanced budget. Minutes before the ECB decision, bunds pared their rally on a report that Chancellor Angela Merkel’s administration would be willing to accept deficit spending.

“The ‘whatever it takes’ moment didn’t come,” said Tanvir Sandhu, chief global derivatives strategist with Bloomberg Intelligence. “A temporary, big upsizing in QE would have helped Italy.”

--With assistance from Namitha Jagadeesh, Celeste Perri, Molly Smith, Hannah Benjamin, Ameya Karve and Greg Ritchie.

To contact the reporters on this story: John Ainger in Brussels at jainger@bloomberg.net;William Shaw in London at wshaw20@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Neil Chatterjee

©2020 Bloomberg L.P.