ETF Investors Are Rewriting the Rules for Interest Rate Hedging

ETF Investors Are Rewriting the Rules for Interest Rate Hedging

(Bloomberg) -- Investors are coming up with new ways to hedge credit risk as interest rates rise and the Federal Reserve appears to be on course for further tightening with minutes from its last meeting scheduled to be released Wednesday.

Amid a steep run-up in Treasury yields and the longest selloff in the S&P 500 Index since the 2016 election, traders are largely avoiding risk. But they’re ignoring the traditional yin-yang relationship between defensive and cyclical stocks, as well as between longer- and shorter-dated Treasury bonds.

Instead, many have taken more ambiguous routes to safety. Some have piled into utilities and long-duration Treasury hedges. Others bulked up their exposure to rate-sensitive banks and moved toward the ultra-short end of the yield curve. And a chunk did a bit of both.

For Ben Mandel, global strategist for JPMorgan Asset Management, the key question facing investors now is how far to lean into risk in multi-asset portfolios while also positioning for the inevitable challenges that come in the later stages of a market cycle. In a recent Bank of America survey, a record 85 percent of fund managers described the global economy as late cycle.

“The business cycle is by all accounts somewhere late in the current expansion, but in our assessment recession risk remains low,” Mandel said. “So the opportunity cost of becoming cautious at this point in the cycle is still actually quite high.”

In an environment where the economy is growing and the Federal Reserve is tightening, it’s expected that bond yields will drift higher and investors will become somewhat cautious going long Treasuries. But for anyone willing to take on some risk, longer-dated government debt is a solid internal hedge, Mandel said.

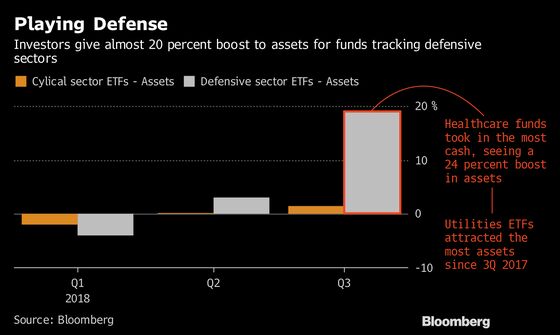

Defensive Turn

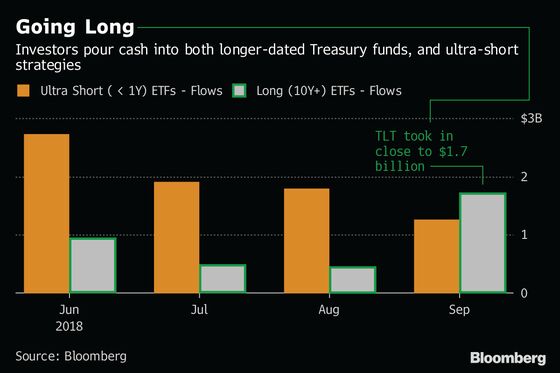

Credit investors appear to have turned more defensive, with strategies tracking short-term Treasuries luring in heaps of new cash. Flows into ETFs that buy government bonds climbed to $2.8 billion in September, the most since April, with those that own inflation-protected notes adding the most in three months. And the inflows have continued in October.

Buyers have turned to the Goldman Sachs Access Treasury 0-1 Year ETF, or GBIL, and the SPDR Bloomberg Barclays 1-3 Month T-Bill ETF, or BIL, both of which track short-term U.S. government debt. The Goldman fund’s assets soared past $4 billion for the first time on Oct. 10, as investors continue to pour cash into the ETF.

But the cautious tone didn’t extend to all shorter-dated debt, as ETFs holding bonds that come due in one-to-three years saw the least interest in September since June. Instead, money flowed to debt maturing in 10 years or more. Those funds added $1.7 billion, the most in six months, while three-to-10 year notes also brought in buyers.

Using Utilities

For equity ETFs, strategies tracking defensive sectors are seeing large inflows, far outpacing cyclical sector funds. Last week, State Street Corp.’s Utilities Select Sector SPDR Fund, the largest ETF tracking the classic defensive industry, brought in nearly $150 million. And last month, utilities funds had more than $290 million of inflows, the most in at least 12 months.

Utilities make a lot of sense to Aaron Clark, a portfolio manager at Boston-based GW&K Investment Management managing $36 billion. Clark examines ETF flows for potential anomalies or contrarian signals, and recently added utilities to his own portfolio. He said he’s gravitating toward companies that are “less cyclical” and have more certainty in their outlook.

But the broad interest in fixed-income isn’t necessarily new for this bull market, according to Yana Barton, an equity portfolio manager at Eaton Vance, who oversees more than $21 billion. Since 2009, for every $1 invested in equities via mutual funds and ETFs, $8 has been invested in bonds, she said.

“It drives me insane,” Barton said. “The Bloomberg Barclays AGG Index is down, yet money continues to flow into fixed-income.”

©2018 Bloomberg L.P.