Equal Opportunity Recovery Weaning S&P 500 of Its Megacap Habit

As stock rebounds go, this one has been big, sudden, and decidedly broad.

(Bloomberg) -- As stock rebounds go, this one has been big, sudden, and decidedly broad, with signs megacap titans are relaxing the stranglehold in which they’ve held the S&P 500 for two years.

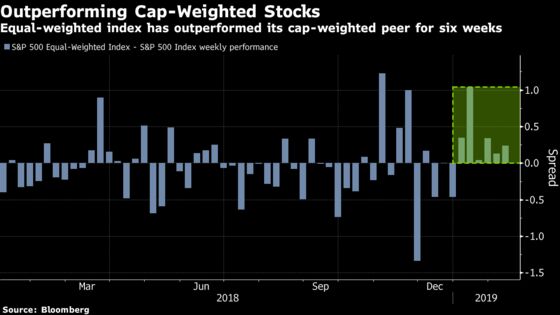

While the rally took a breather last week, it remains the best annual start for U.S. equities in almost three decades, with $1.7 trillion added to share values. Notable in the surge has been the role of smaller companies -- or less-gargantuan ones, anyway. An equal-weighted version of the S&P 500 that strips out market-cap biases is beating the regular gauge by 2.3 percentage points.

A small advantage, to be sure, but a sign of breadth that has been absent as market leadership got squeezed into a narrower cohort over the past few years, alarming analysts. At present, the equal-weighted S&P 500, which gives a relatively small company like H&R Block Inc. the same influence as Apple Inc., has beaten the cap-weighted gauge for six consecutive weeks, the longest streak since 2016.

“When we have a healthy market environment, that’s something that tends to happen -- a rising tide lifts all boats,” said Jack Ablin, Chief Investment Officer at Cresset Wealth Advisers. “Maybe the market has decided that the outperformance of the Nvidias of the world isn’t going to continue.”

Eight of the 10 biggest gainers in the S&P 500 this year are companies with market capitalization of less than $30 billion. Driving that has been the Federal Reserve’s dovish stance on rate hikes, a potential tailwind for companies with more leverage, and a rotation away from technology and into industrials and real estate, where fewer giants reside.

In a week when U.S. stocks failed to rise past their 200-day moving average, the gauge of equal-weighted stocks provided a cushion. Broader market participation and a break-out in small and medium-sized stocks is generally welcome by analysts and is good for stock pickers, too.

It hasn’t been a clean sweep for the size factor. Four Fang megacaps -- Alphabet Inc., Amazon.com Inc., Netflix Inc and Facebook Inc. -- continue to surge. But a gauge of the 100 largest stocks is trailing the broader market, rising 9.2 percent this year, compared with a 11 percent gain in the S&P Midcap 400 and a 12 percent advance in the Russell 2000 Index. Last month, the equal-weighted index outperformed the S&P 500 by the most since 2011.

Broader market participation at least begins to assuage concern about the market’s uneven bounty, in which it has sometimes seemed like five or six stocks account for the entire return. Between the 2016 presidential election and the market peak in September, Nvidia Corp., Netflix Inc. and Amazon.com Inc. were among the 20 biggest gainers.

In 2019, Xerox Corp., with a market value of $6.7 billion and Mattel Inc., the $5.3 billion toy manufacturer, have spearheaded the advance. The Fed’s about-face on rate increases mitigates smaller firms’ concerns about cost of debt and could be one reason for the rally. Optimism that growth in the U.S. isn’t slowing as fast as some predicted in December is another. Whatever the reason, a broader advance is a good thing for markets, according to Miller Tabak + Co.’s Matt Maley.

“It’s always concerning when so few stocks are making up such a big portion of the outperformance,” Maley said by phone. “Large-caps have performed in-line with the broader stocks, but the fact that we’re not seeing investors piling back in probably means they don’t have the confidence they are going to outperform.”

The lag in megacap performance is coming amid a broad exit from exchange-traded funds in the first part of the year, in which about $30 billion was pulled in the first six weeks of the year, according to EPFR data, the worst start to a year since the company started tracking exchange-traded fund flows in 2000. It may not be a coincidence. Withdrawals from index-tracking funds create a disproportionate drain on larger companies since a majority of them are cap-weighted.

“There’s no one absolute smoking gun here but rather a variety of factors, like cooling sentiment toward the rest of the year and uncertainty about what’s happening next in terms of the rate hikes,” said Cameron Brandt, director of research at Emerging Portfolio Fund Research. “There is also a general rotation at the moment out of the U.S. stocks. People who are interested in finding value don’t really see it in the U.S.”

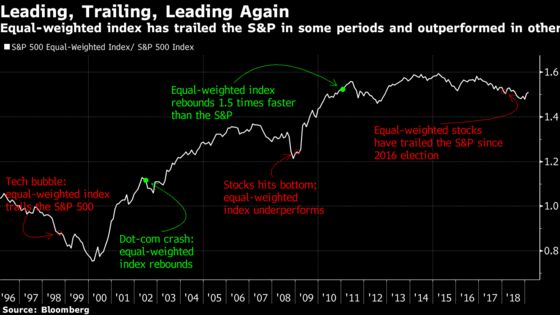

It remains to be seen whether the equal-weighted index is merely catching up to its capitalization-weighted peer after trailing it since late 2016. The S&P 500 outperformed the equal-weighted index during the tech boom, only to trail the gauge after the dot-com bubble crashed. Between March 2009 and March 2013 when the U.S. stocks breached their pre-crisis high, the S&P 500 Index added 62 percentage points less than the equal-weighted gauge. The rally between the 2016 election and the Sept. 2018 high reversed the trend again.

“When the tide goes out and the best-performing tech and consumer discretionary sectors start to fall, you can see the situation where the equal-weighted index holds in better than the cap-weighted,” said Sameer Samana, senior global market strategist for Wells Fargo Investment Institute. “The equal-weight is kind of the anti-momentum strategy, and for much of the cycle, people tried to play the momentum factor.”

To contact the reporter on this story: Elena Popina in New York at epopina@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.