Enormous De-Leveraging in Bond Market Smacks of Margin Calls

Enormous De-Leveraging in Bond Market Smacks of Margin Call Rush

(Bloomberg) -- A sell-off in the supposedly safe government bond market this week has unnerved investors looking for a haven amid the risk-asset storm. A slump in open positions in bond futures suggests a rush to meet margin calls may be partly responsible.

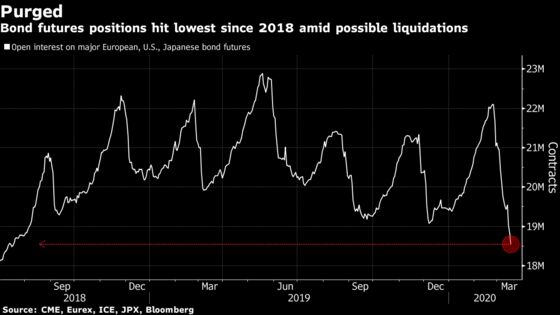

Calculations by Bloomberg show bond futures positions equivalent to $150 billion in 10-year Treasuries were sold Friday through Tuesday, with total outstanding contracts dropping to the lowest since 2018. This week saw a gauge of global stocks slump around 11% amid the worsening coronavirus outbreak, while an equivalent index of government bonds tumbled over 3%, wiping out gains from earlier in the month.

“The concomitant sell-off in both the risk-free asset, bunds, as well as in credit and equities can either mean that markets are pricing in unrealistic bond-supply shocks and/or, more likely, mean that markets are de-leveraging,” wrote Erjon Satko, a strategist at Bank of America Merrill Lynch. “Times are exceptional.”

Leveraged investors often see margin calls as volatility spikes and can be forced to sell liquid securities, including bond futures, as a result. The change in positions across German, French, Italian, U.S. and Japanese bond futures suggests an enormous de-leveraging has taken place.

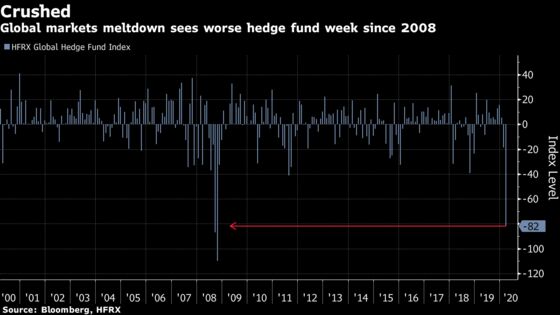

While the evidence may be circumstantial, leveraged investors such as hedge funds have been under enormous pressure given the volatility in equity and commodities markets. HFRX’s Global Hedge Fund Index, which measures performance in the broader industry, saw its largest one-day loss since the financial crisis on March 16. The gauge is down over 6% this month.

That suggests it’s likely some hedge funds have struggled with margin calls during the rout which has led to a shedding of liquid assets.

There are signs of “asset managers raising cash to face redemptions in their funds,” Jaime Costero, rates strategist at UBS Group AG, wrote in emailed comments. For these investors it “makes more sense to liquidate sovereign bonds and core bonds than credit exposures because these are more illiquid.”

Investors looking for further proof can check out February’s international capital flows report from the U.S. Treasury, due mid-April. Caribbean-domiciled investors are seen as a proxy for leveraged investors, and have been shown to shed Treasuries in the past to pay margin calls or repay clients after draw-downs.

Algorithm, retail and high-net-worth investors have capitulated while longer-term investors are holding on, Danny Yong, Dymon Asia Capital (Singapore) Chief Investment Officer, said in an interview with Bloomberg Television. There may also have been some redemptions of hedge fund holdings from sovereign wealth funds as the collapse in oil prices prompted them to shore up reserves, he added.

Gold Dilemma

Gold, another traditional haven, has also been pummeled lately. Prices have dropped about 13% from a peak set early last week, and are going through wild swings with investors caught between the need to free up cash and insurance against the faltering economy.

Aggregate open interest, a tally of outstanding contracts, dropped this week on the Comex to the lowest since July.

“Many market players have closed long positions and have probably not opened short ones,” said Commerzbank AG analyst Daniel Briesemann. “You’re closing longs to raise cash, but you don’t want to bet on falling gold prices because gold is still seen as a safe haven in such a market environment.”

©2020 Bloomberg L.P.