Energy Stocks Show How to Lose Friends and Alienate People

Energy Stocks Show How to Lose Friends and Alienate People

(Bloomberg Opinion) -- If coming last in a popularity contest stings, consider how it feels to come first in an unpopularity contest. In Tuesday’s mass defriending of stocks, the energy sector managed to stand out in the worst possible way:

The whiplash here is incredible. In early October Nymex crude oil was trading at more than $76 a barrel and the S&P 1500 exploration and production index was at its highest level in more than three years. Since then, they’re down 28 percent and 20 percent respectively. In relative terms, E&P stocks are trading at their lowest level on forward Ebitda multiples since Christmas 2008, another holiday season not noted for its bounding optimism, you may recall:

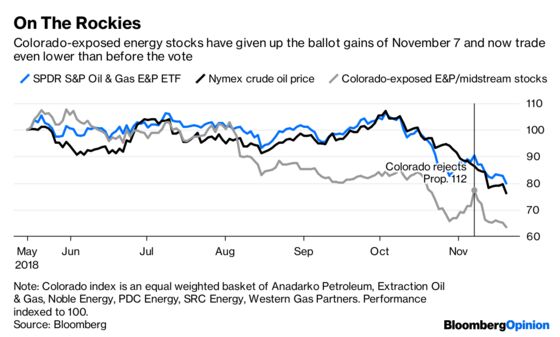

Explanations for this sudden lack of affection have tended to focus on President Donald Trump’s unexpectedly generous use of waivers with regards to renewed sanctions on Iranian oil exports. Yet in truth the E&P sector had been steadily de-rating for a year or so before this latest wash-out. Even unabashedly good news has failed to stick: Look at what’s happened to a basket of Colorado-exposed E&P stocks including Anadarko Petroleum Corp. that bounced after the state’s voters rejected a measure to severely limit fracking:

E&P stocks face a tough crowd partly because investors bear scars from the legacy of the pre-2015 boom. Once energy prices crashed, it became abundantly clear how much money had been spent (much of it debt-financed) on poor assets. Since then, the industry has made huge progress in cutting costs, and many prominent producers have also reset strategies away from growth and toward returns.

This hasn’t provided absolute shelter from the latest storm; Anadarko, for instance, has undergone one of the more obvious Damascene conversions but is still down 24 percent from early October. Still, better that than the experience of, say, California Resources Corp., a highly levered oil-price play that has fallen by more than half.

The lesson here, if any, is that the process of regaining investors’ trust in energy will likely be a long one. So E&P companies should either stick with the returns-over-growth strategy or adopt it immediately, especially as they set drilling budgets for 2019.

As they do so, they should consider the other reason oil prices have backtracked so quickly. Signs of weakening in oil demand have been building in the gasoline market for at least six months, and have become obvious in recent weeks as refining margins for that fuel have collapsed. The wider sell-off in financial markets and industrial metals, along with a sprinkling of weak economic indicators such as U.S. housing and Chinese auto sales, mean producers shouldn’t count on 2019 oil-demand forecasts holding up. The International Energy Agency’s projection for growth to actually be slightly higher next year than in 2018 looks particularly subject to revision.

For their part, one set of big producers — OPEC and its partners — are all but pre-announcing that their meeting early next month will result in a supply cut to shore up prices. Secretary General Mohammad Barkindo said last week the group will do “whatever it takes” to deal with any imbalance of supply and demand. The echo of a certain European central banker may have been an intentional warning to the oil bears. But the historical parallel can’t help also sounding a certain note of panic.

What’s more, taking OPEC barrels off the market, which tend to be heavier grades, could exacerbate the widening gap between gasoline and distillate pricing that is bedeviling the oil market. One possible reason the prospect of this OPEC meeting isn’t inspiring confidence is that, if demand is the problem, then the group’s cuts may amount to pushing on a string.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.