Feeling All the Feels in Energy Stocks

Feeling All the Feels in Energy Stocks

(Bloomberg Opinion) -- If there’s any sector that wishes numbers were meaningless and feelings were currency, it’s energy. On second thought, maybe even feelings wouldn’t be much help.

Brent crude is below $60 a barrel; West Texas Intermediate is under $50. And this after OPEC and its entourage announced renewed supply cuts. Now the entire stock market is in a funk (hence President Donald Trump’s Tuesday morning appeal to emotion over numbers). When you consider that energy stocks didn’t buy into oil’s brief rally in late summer and early fall anyway, and you survey the wreckage in gasoline refining margins, it’s hard to escape the thought that demand may deserve more attention than supply.

The chart above actually understates just how unloved energy stocks are. The index is at its lowest level since March 2016, when Brent was treading water around the $30 mark. Its weighting in the S&P 500 is just 5.5 percent, which is even lower than back then (it was about 11 percent before the oil crash began in 2014).

I ran a screen of North American integrated and exploration and production companies with a market cap of $500 million or more on the Bloomberg Terminal, yielding 83 stocks. I then measured their stock price performance over two periods: year-to-date and since the end of September, which is roughly when oil peaked this year (everything that follows is measured as of Monday’s close, although stocks and oil were mostly down again Tuesday morning). Here are some observations:

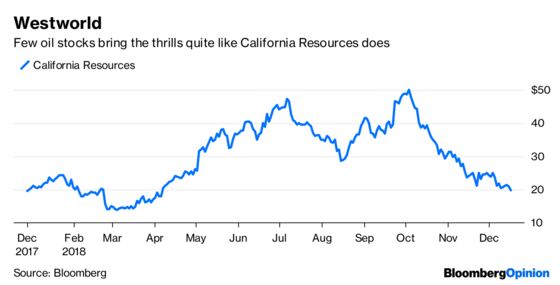

- Only nine stocks are in positive territory for the year. W&T Offshore Inc. leads with a gain of 44 percent, although this can mostly be attributed to it entering 2018 after a shellacking last year, when it dipped below $2 during that summer. Similar dynamics explain why California Resources Corp. also makes it into the nine despite a 59 percent plunge since September, making its stock feel like the lovechild of oil and bitcoin.

- Close runner up: MEG Energy Corp., mainly because fellow Canadian Husky Energy Inc. launched a hostile bid for it in early October (the day before oil prices peaked for the year, curiously enough). Indeed, that bid explains why MEG is the only one of the 83 stocks surveyed that has beaten the S&P 500 both year-to-date and quarter-to-date.

- Only one large-cap stock is positive for the year: ConocoPhillips, up 15 percent. Conoco was one of the first oil companies to capitulate in the oil crash and overhaul its strategy in favor of disposals, paying off debt, reducing unit costs and promising high distributions of any free cash flow. It reiterated that message earlier this month, holding its budget for 2019 flat and raising its payout target. That’s as sound an approach as you can get in this oil market, but hasn’t been enough to stop Conoco underperforming the S&P 500 this quarter. Still, a drop of 18 percent beats oil’s 28 percent slide (take your feelings where you can get them).

- Hess Corp. was also positive as of Monday’s close, up about 5 percent. That said, it has plunged around 31 percent since September, taking it back to roughly where it was before activist Elliott Management Corp. showed up almost six years ago. The company has been transformed since then, though it remains a mini-major whose chief appeal is its stake in Exxon Mobil Corp.’s phenomenal discovery offshore Guyana. The problem here is that Guyana’s riches are still several years away from being realized, leaving Hess looking light on cash payouts in the meantime.

- Fully 69 stocks, more than one in four, have lagged behind the S&P 500 both year-to-date and this quarter. That includes Exxon Mobil. While energy’s traditional safe haven has weathered the oil-price slide better than most — down 13 percent versus oil’s 28 percent since September — that still puts it slightly behind the broader stock market. Which raises, again, the question of why those seeking energy exposure (hello? anyone?) would target this stock, since there’s better leverage to oil prices elsewhere and there’s more defensiveness in simply owning the market. Exxon’s conspicuous lack of buybacks, its old calling card, compounds the issue. Especially as main rival Chevron Corp. now yields more on that basis — and, incidentally, has outperformed the S&P 500 this quarter.

In short, with very little love to go around, inducements like dollar payouts or a firm takeover offer go a long way. Numbers really do matter more than feelings, it turns out.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.