Election Volatility Is Short Trade of a Lifetime for the Brave

Election Volatility Is Short Trade of a Lifetime for the Brave

(Bloomberg) -- For volatility professionals who get it right, the American presidential election could go down in history as the short trade of a lifetime.

Yet betting that calm -- not chaos -- will take hold on Wall Street is proving easier said than done.

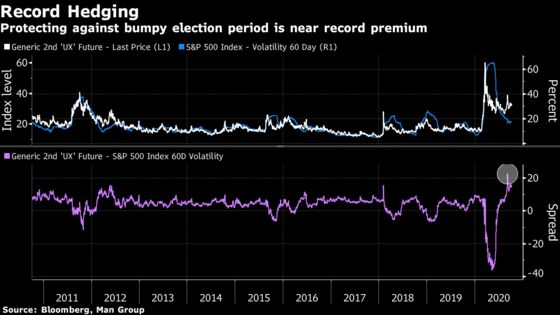

As one of the most-expensive event risks on record, investors who place a wager on muted stock swings in the aftermath of the Nov. 3 vote could net riches, if history is any guide. But a tumultuous campaign for the White House is spurring many of these specialized traders to hold fire.

Funds like Dominice & Co. and Ambrus Group say there’s good reason for investors to load up on stock hedges in record numbers. But their peers from Aegea Capital to Volaris Capital see a lucrative opportunity to sell protection in the derivatives market.

All in, the volatility landscape offers rich premiums for the brave but it’s looking dangerous out there.

“Some brave vol traders will try to take advantage,” Nomura Holdings Inc. strategist Charlie McElligott wrote in a note. “Could be a career ‘maker or breaker’ with the potential to see monster returns.”

Among the short-sellers is Cem Karsan, founder of Aegea Capital Management LLC, a volatility fund in Chicago. He’s selling implied volatility in December and January, using Cboe Volatility Index and S&P 500 options, on the expectation that the concern over a heavily-contested election is overinflated.

“When events conclude, regardless of the outcome, event volatility declines,” Karsan said. While his conviction was already strong prior to President Donald Trump’s Covid diagnosis, it’s only strengthened after the president was hospitalized over the weekend.

In the latest Wall Street Journal/NBC poll released Sunday and conducted after the Sept. 29 debate, Biden’s lead over Trump had widened to 14 percentage points. The former vice president’s growing dominance, along with extensive early voting, has some strategists saying a disputed outcome is becoming less likely.

Yet there are good reasons why volatility markets are pricing in political fireworks well beyond November, from Trump issuing an extraordinary refusal to say whether he’d accept the election result if he loses, to his wild campaign more generally.

Then there’s the pandemic-lashed business cycle. Volatility shorts were hammered earlier this year when the VIX spiked to a record during the Covid crash, with fewer systematic options sellers having returned to the market since then.

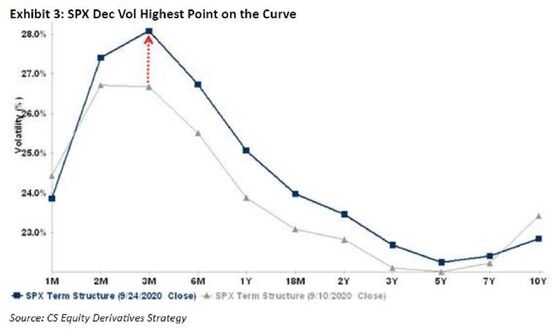

All that means investors have been bidding up the price of hedges to historic highs. As of Oct. 1, options on the S&P 500 Index were pricing in an implied move of 3.5% on election day, according to UBS Group AG’s Stuart Kaiser. Yet, time and again the election aftermath has proved less disruptive than markets have anticipated, according to Credit Suisse Group AG’s Mandy Xu.

She calculates an average one-day election move of 1.4%. Fears tend to deflate quickly after the vote, too.

Given the tendency of investors to demand higher compensation for future uncertainty compared with what actually comes to pass, known as the volatility-risk premium, short-sellers can find good reason to pounce.

Volaris Capital, the hedge fund founded by ex-Credit Suisse Group AG trader Vivek Kapoor, sees potential “selling opportunities” around the election period, according to quantitative trader Margaret Sundberg. The firm evaluates opportunities to trade S&P 500 options in part by looking at Sortino ratios, which measure risk-adjusted returns similar to Sharpe ratios.

Others are treading carefully. At Ambrus, a New York-based volatility fund, Kris Sidial is long December volatility and cautious overall. “You’ve got the election, the pandemic, the earnings cycle. You toss in all these things, and as a trader, why would we be short?” he said.

Dominice & Co., a Geneva-based manager with volatility strategies, doesn’t see a ‘golden’ opportunity’ to go short either.

The difference between the volatility implied by options prices and actual market swings “is high but not the highest it has ever been,” said Pierre de Saab, a partner at the firm. “During the summer we saw similar spreads that did not even include the event risk of the elections.”

Meanwhile, traders like Colton Loder at alternative investment firm Cohalo are watching and waiting. The Washington-based fund manager has been focused on the front end of the VIX futures curve but is prepared to short longer-dated volatility futures as election day nears.

“Of late it has been interesting to play up the ‘lengthening’ of the election premium,” he wrote in an email. “Could there be an opportunity to position for the ‘shortening’? I’ll be watching it, for sure.”

©2020 Bloomberg L.P.