Election Rally Is Feeding the Duration Monster in Stock Markets

Election Rally Is Feeding the Duration Monster in Stock Markets

(Bloomberg) -- The frenetic election rally is turbocharging investing strategies tied to the cheap money era -- revitalizing some of the most hated trades of this bull market.

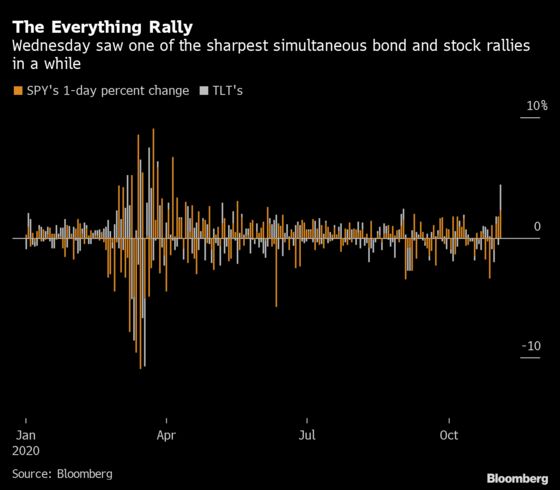

With 30-year Treasuries set for their strongest two-day rally since June, cross-asset trades seen as dangerous for their sensitivity to interest rate risk -- from growth stocks to long-maturity debt -- are getting another life.

In short, duration is back in vogue as Wall Street calculates that massive fiscal stimulus is off the table, and bets the Federal Reserve will double down on loose policies to battle the pandemic.

Growth stocks had their best day versus value since 2001 on Wednesday, defying countless warnings that the valuation gap was reaching levels seen in the dot-com bubble. The S&P 500 and long-end bonds staged their biggest combined jump since April -- boosting multi-asset portfolios that many fretted were running out of juice with yields already near historic lows.

Early trading on Thursday showed more of the same. An exchange-traded fund that bets against Big Tech, ticker SQQQ, was the most active as it plunged more than 7%. Treasuries edged higher, building on their surge from a day earlier.

“An expansion of monetary policy measures will be no substitute for a decent fiscal stimulus package,” Eleanor Creagh, a strategist at Saxo Bank, wrote in a note. “However, the Fed may be left with few options if lawmakers cannot put their differences aside. This is certainly not the best outcome for the real economy, but as we know risk assets love liquidity.”

As strategists digested a tighter-than-expected race for Joe Biden and dwindling odds for Democrats to win the Senate, speculation for more Fed support grew. Creagh said policy makers might boost stimulus as soon as next month, including purchasing longer-maturity assets.

The central bank is expected to stand put at Thursday’s meeting, though it could hint at further easing down the road.

In the stock market, the resurgent duration trade is dealing another blow to the embattled value strategy as investors pile into tech shares beloved for their long-term earnings prospects. The fading threat of tighter regulations under a Democratic government also helped.

Growth equities tend to do better with low bond yields, since their long-term cash flows can be discounted at lower rates and are often less tied to the business cycle. Think Facebook Inc. rather than Exxon Mobil Corp.

The value rotation was crushed, “as markets pivot back towards a future state resumption of lower interest rates, flatter curves and disinflationary pressures that we have already operated under for much of the past five, ten years,” Charlie McElligott, a strategist at Nomura Holdings Inc., wrote in a note.

While the dominance of so-called FAANG stocks in U.S. indexes flatters performance, that belies weakness beneath the surface. The equal-weighted S&P 500 underperformed the capitalization-weighted one by more than 2 percentage points on Wednesday, the biggest gap since 2009. Many investors had counted on a stimulus package exceeding $2 trillion from Democrats to benefit a larger swath of stocks, including many battered by the pandemic.

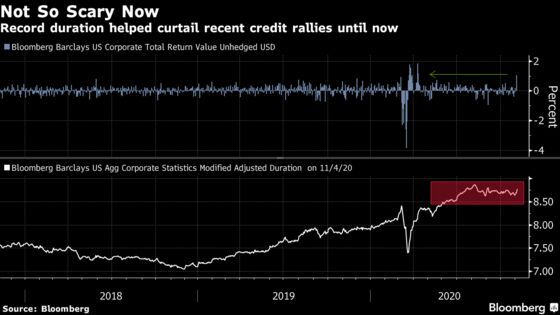

In credit, all the hallmarks of an extended Fed put are emerging. The biggest junk-bond ETF, ticker HYG, saw its largest inflow since June on Wednesday while its peer, JNK, attracted the most since July.

A gauge of investment-grade bonds jumped the most since April. The duration risk of U.S. corporate debt rose to the highest in two months. That has left sensitivity to rate changes once again near a record high -- approaching the level reached in summer, when the credit rally started to fade.

That looks like no barrier as long as investors have faith in the Fed. And low-for-longer trades may have further to go. Ten-year Treasury yields could drop to 0.6-0.65% from 0.76% on Thursday, putting flattening pressure on the two- and 10-year portion of the curve, ING strategists led by James Knightley wrote in a note.

“We are still keen on credit and mortgages on Fed support,” said Gregory Perdon, co-chief investment officer at Arbuthnot Latham in London. “The system has been backstopped and we think it will be difficult to lose money in that asset class.”

©2020 Bloomberg L.P.