S&P 500’s Earnings Miracle Is Failing to Take Hold in the Second Half

While second-quarter results have been a bit better than expected, estimates for the third and fourth are moving the wrong way.

(Bloomberg) -- Behind the scenes of another middling earnings season is evidence that analysts are deceiving themselves when they predict things will be much better by Christmas.

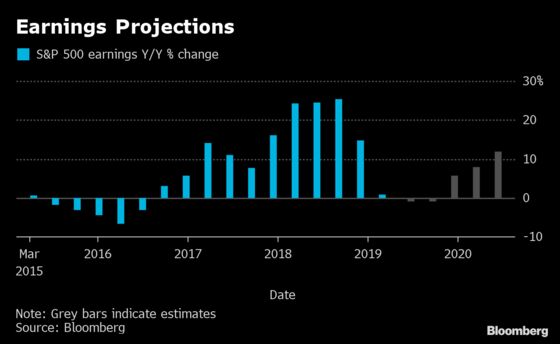

While second-quarter results have been a bit better than expected, estimates for the third and fourth are moving the wrong way, worsening over the last two weeks. Companies that are beating estimates now are refusing to raise guidance -- effectively lowering the outlook for the second half.

That’s worrisome news for anyone hoping Jerome Powell’s Federal Reserve will be able to solve all their problems. Investors just lifted the S&P 500 to its best start to a year since 1997. Signs the current earnings malaise is more than temporary are unwelcome.

“This whole market rally is based on sentiment and increasing multiples in absence of earnings growth,” said Ryan Nauman, market strategist at Informa Financial Intelligence. “Eventually investors are going to get complacent and aren’t going to be willing to pay these prices, so we’ll need earnings growth -- something more on the fundamental side than sentiment-driven based on the Fed and trade and so on.”

Before Citigroup Inc. kicked off the second-period reporting season two weeks ago, analysts expected earnings to fall 0.2% in the third quarter and rebound 6.4% in the fourth. Now, after more than a third of S&P 500 companies have reported, those estimates have corroded. Wall Street expects earnings to fall 0.8% this quarter and rise 5.8% in the next, according to Bloomberg Intelligence data.

The picture is getting muddled as worries that have existed all year intensify. Slowing global growth, erratic commodity prices, heightened trade and geopolitical tensions -- all are starting to weigh. While many are counting on the Fed and other central banks to help smooth things out, the more earnings estimates decay, the harder that thesis gets to believe.

“It really is an uncertain time. With respect to the equity markets, monetary policy is going to be the significant driver of investor sentiment and investor confidence,” Nancy Perez, senior portfolio manager at Boston Private, said by phone. “If those numbers do start to come down and the Fed becomes more aggressive, and you see global monetary policy becoming more aggressive, then the question is, will it be enough?”

Of companies that have reported results so far, about 78% are exceeding their profit estimates -- in line with the average. While the strong results are reassuring, a growing number of those firms aren’t raising their full-year outlooks.

Take bellwethers like Caterpillar Inc. and United Parcel Service Inc., which give investors insights into multiple corners of the economy. UPS reported better-than-expected second-quarter earnings, topping the highest forecasts. But the company left full-year estimates unchanged. Caterpillar’s second-quarter profits and revenue rose compared with the year-ago period but the company said it expects profits will come in at the low end of its forecasts for the year.

Since mid-2018, full-year growth estimates have been slipping at a rate worse than what has happened historically, according to RBC. In fact, the bank found that a majority of companies that have issued third-quarter guidance so far have been negative.

As those estimates come down, a growing number of analysts are warning that it may not be enough. The trade war could drag on, a resurgence in the dollar or a pickup in wage growth could put pressures on margins, and tensions with Iran could worsen. The list goes on.

Projections for the second half of this year, as well as next, are “still materially too high,” wrote Morgan Stanley strategists in a recent note. Bloomberg Intelligence warned that forecasts for improvement in the quarters ahead will come under intense scrutiny. Strategists at Deutsche Bank expect continued downgrades or disappointing results. For RBC’s Lori Calvasina, the “big problem” is the hockey stick-like rebound investors expect in the fourth quarter.

At stake is the stock market’s stellar performance so far this year. If earnings continue to deteriorate, further upside could be hindered. For Morgan Stanley, that’s worrying. Fed cuts shouldn’t be celebrated if they’re accompanied by earnings or an economic recession, wrote chief equity strategist Mike Wilson in a recent note.

“History is clear on this one. If this is the beginning of a full-blown rate-cutting cycle by the Fed in an attempt to ward off a recession a la 1990, 2001, or 2008, stocks typically don’t do well after the first cut,” he said.

To be sure, even if an earnings recession happens in the coming quarters, it’s possible it could be shallower than the one that occurred between 2015 and 2016, according to Strategas’s Jason DeSena. “Using that period as a guide would suggest that the market is due for a breather while valuations catch up to Index levels followed by a resumption of the bull market,” he wrote in a recent note.

Yet, it’s not just this year that’s unsettling. Some strategists are worried double-digit gains in 2020 won’t happen. Downward revisions today challenge expectations for a grand recovery into next year. And the market hasn’t yet taken that into account.

"It’s not 2019 earnings that’s going to trip up the market. It’s those numbers basically in the neighborhood of low double-digit earnings growth for the next two years, that just looks a little optimistic to me,” said Dave Lafferty, chief market strategist at Natixis Investment Managers. “What I’m watching is when does the market start to discount those out years? And you just haven’t started seeing it yet.”

--With assistance from Wendy Soong and Elena Popina.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.