Earnings Days Rapidly Becoming the Stock Market's Biggest Hazard

One of the worst things that can happen to an investor this year is finding out how her companies are actually doing.

(Bloomberg) -- One of the worst things that can happen to an investor this year is finding out how her companies are actually doing.

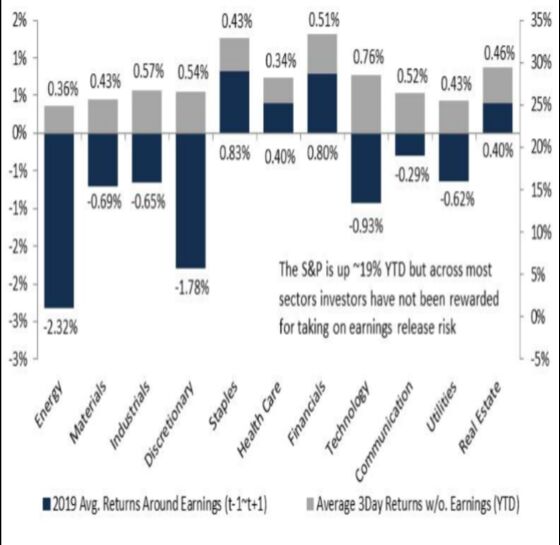

So says Evercore ISI, whose strategists have been measuring the performance of individual stocks in the period before, during and after earnings days. For seven of 11 industries in the S&P 500, it’s basically the only time returns have been negative.

It says a lot about 2019, in which equity gains come hand-over-fist. So powerful has been the promise of fresh stimulus from Jerome Powell’s Federal Reserve, that even persistently bearish reactions to earnings have barely dented a market enjoying one of its best rallies in two decades.

“The market’s going up until companies open their mouths,” Dave Lafferty, chief market strategist at Natixis Investment Managers, said by phone “When you actually look at those periods where people are focused on company by company results, and not this warm, fuzzy macro environment of the Fed’s 180, I guess it doesn’t surprise me that those days have seen more pain.”

By this point, pretty much everyone is aware that an “earnings recession” is a risk as estimates for profit growth hover precariously near nothing. Bloomberg Intelligence has referred to hopes of a strong recovery as possibly “nothing more than a pipe dream.”

But rather than fret, investors have been focused on the positives -- a still relatively steady U.S. economy and above all a dovish Fed, with markets calling for a rate cut as soon as this month.

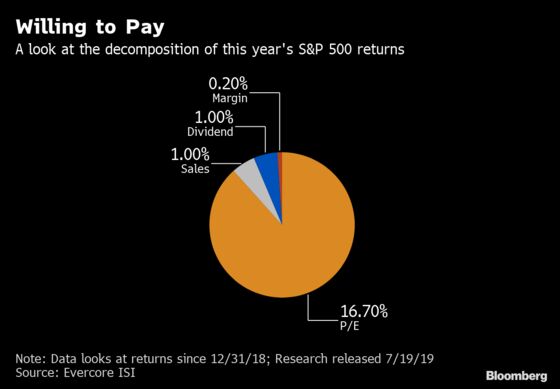

Evercore ISI estimates that as of Friday, 16.7 percentage points of the market’s 18% return was the result of multiple expansion -- investors paying more for the same earnings -- with the 12-month forward price-earnings ratio rising from 14 in January to 17 now. Growth in sales, dividends, and margins have each contributed less than 1%.

“Companies have tended to suffer around earnings releases even as the overall market has moved higher,” Dennis Debusschere, the firm’s head of portfolio strategy, wrote in a research note. Investors have been “punished for taking on release risk.”

Only consumer staples, health-care, financials, and real-estate stocks have been rewarded when disclosing results, the firm found. The other, mostly cyclical industries have all been punished. Energy stocks have taken the largest hit, down 2.3% on average in the days before and after reports. Consumer discretionary stocks have stumbled 1.8%, and technology companies have fallen nearly 1%.

On the other hand, every S&P 500 sector has seen positive returns on days without earnings reports, according to Evercore ISI. Tech stocks have gained the most throughout the quiet periods. Industrials, consumer discretionary, and communications shares are the next best performers. That’s driven these four areas to become the best performing sectors this year.

The pattern is playing out again in the current season. Since Citigroup Inc. kicked off the second quarter earnings season on July 15, the S&P is down 0.3%, a number that was worse prior to the biggest rally in three weeks on Tuesday. There’s still plenty of time to go with three-quarters of the benchmark yet to report, but as it stands, companies that miss earnings estimates are being punished more than those that beat are being rewarded.

In the 24-hours after releasing earnings, firms that have missed profit forecasts have fallen 1.9% on average, according to data from Wells Fargo Securities. That’s more than the 1.2% gain those that beat have been rewarded with. The pattern of investors being rewarded during earnings season for prescient picks has receded over the years.

Evercore ISI holds that as portfolio managers and analysts have grown more knowledgeable and machine-powered quant strategists have proliferated, it’s been difficult to gain a competitive edge and generate excess returns during earnings season. The team of strategists cited a 2017 paper titled, “Time to Change Your Investment Model,” to show that even if you were able to predict precisely which companies would beat or miss on earnings, it wouldn’t matter much.

“The average gain from using a ‘perfect prediction model’ has fallen to almost zero,” Debusschere wrote. “Even if you knew the results of all earnings reports ahead of time, generating alpha with that data would still be difficult.”

To contact the reporter on this story: Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.