Duration Danger Is Making Europe’s Ultra-Long Bonds a Hard Sell

Duration Danger Is Making Europe’s Ultra-Long Bonds a Hard Sell

(Bloomberg) -- After seizing on the lowest rates in history to extend debt maturities into the next century, Europe’s safest issuers have hit an impasse.

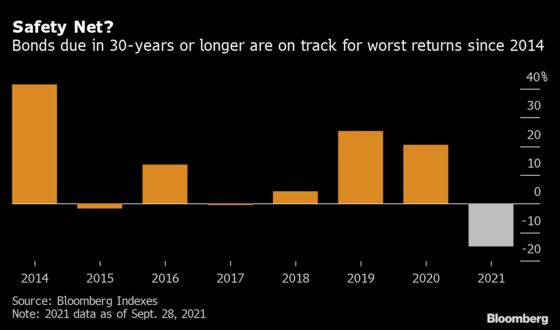

Ultra-long debt is on pace for its steepest declines in more than seven years, as rebounding growth and inflation prompt investors to dump the safest debt that’s most sensitive to interest-rate risk.

With investors suddenly wary of duration risk, even bankers acknowledge long-dated debt is going to be a hard sell from now on.

“Everyone understands that the market now is a bit more fragile than it was at the beginning of the year,” said Ioannis Rallis, JPMorgan Chase & Co.’s head of public sector debt capital markets. “It’s unlikely we see much ultra-long debt issuance at a very large scale.”

Losses on Europe’s highly-rated government bonds maturing in 30 years or longer are far outpacing those on medium-term debt: down 15% versus 2.35% on securities due in seven to 10 years, according to Bloomberg index data. The dismal performance contrasts with a gain of 20% last year.

In the U.S., demand for long-dated high-grade corporate debt has been resilient, boosted by overseas buyers hunting for yield. That’s allowed companies like Blue Owl Capital Inc., which is selling bonds due in 30 years on Thursday, to extend maturities.

The 20-year and 30-year part of the curve have been “almost as strong” as the middle and the front end, according to Chris Forshner, head of high-grade finance at BNP Paribas SA. “That may change over time if we start to see some of these inflationary measures persist over a long period of time, say in the next nine to 12 months,” said Forshner in an interview this week.

Europe’s resistance to long-term debt marks a stark reversal from most of this year, when safety was paramount as Covid-19 tore through global economies, central banks pledged almost limitless support and rate hikes looked far off.

Investors looking to escape a sea of negative yields snapped up some of the longest-maturity debt on offer -- and they were amply rewarded. Just look at Austria’s 2117 bonds, which returned a whopping 44% last year.

For issuers, the buoyant market proved irresistible, spurring a sales spree of almost 84 billion euros ($98.3 billion) of ultra-long bonds so far this year, according to data compiled by Bloomberg, comprising about 13% of raised in the region’s public debt markets. Just this month, when Greece sold 1 billion euros of bonds due in 2052, demand came in above 9 billion euros.

“Until now, issuers were funding from five all the way up to 100 years,” said Damien Carde, who heads the frequent borrowers group in debt capital markets at NatWest Markets. “Funding past 30-years might become a bit more difficult.”

That’s not to say pockets of demand won’t endure. Life insurers that match fund long-term liabilities, for example, should continue to seek out ultra-long debt, according to Deutsche Bank AG.

“For issuers there is always a price,” said Neal Ganatra, the bank’s EMEA head of debt capital markets, SSA syndicate. “Are we going to continue to see the massive 50-years transactions like the ones we have seen earlier this year? Probably not, but there will still be some issuance.”

Elsewhere in credit markets:

Americas

Three companies are selling bonds in U.S. primary high-grade. The market has weathered the week’s macro volatility, selling over $22 billion fresh debt so far. The tally is in line with the consensus forecast of around $20 billion, with supply likely to exceed projections after today’s session.

- In high yield, two new deals were announced on Thursday while Medline Industries is set to wrap up its jumbo, multipart junk-bond sale after shifting $1.5 billion from one tranche into other components of its buyout financing package

- At least eight more borrowers are racing to price bonds to take the monthly tally to about $44 billion, the second busiest September on record

- Money managers that put together collateralized loan obligations are scrambling to get deals done before early next year, when the market undergoes a potentially messy transition to a new benchmark rate

- Meanwhile, a CLO ETF loaded with loans rated BBB or lower is on the way

- Exela Technologies is planning to sell as much as $250 million of shares to repay secured debt, according to a regulatory filing

- JPMorgan promoted Josh Younger to head of asset and liability management analytics and strategy

- S&P Global Ratings warned that inflation and high corporate debt taken on during the pandemic are the two biggest threats facing credit markets in the U.S. and Canada

- For deal updates, click here for the New Issue Monitor

- For more, click here for the Credit Daybook Americas

EMEA

Seven issuers sold 4.7 billion euros ($5.4 billion) of bonds in Europe’s primary market on Thursday, pushing monthly sales above 200 billion euros for the first time since January.

- Adler Group’s bonds extended declines, while the cost of protecting the German landlord’s debt hit a record

- The company’s 300 million-euro bond due April 2026 fell a further 2.6 cents on Thursday to its lowest price on record after losing 3.4 cents Wednesday

- CVC Credit Partners is seeking 2 billion euros for its third European direct-lending fund, as the firm looks to expand in private credit

- The fund will provide senior debt financing to sponsor-backed lower and middle-market companies across Europe, according to a document associated with Wednesday’s meeting of the New Jersey State Investment Council

Asia

A rising dollar is adding to headaches for emerging-market bonds.

- Losses on dollar notes from developing economies have accelerated to 1.6% this month, Bloomberg indexes show, after hawkish comments from the Federal Reserve pointing to tighter monetary policy

- An MSCI emerging-markets currency index has lost about 1% against the dollar so far in September

- The bonds and the currency index have both plunged the most on a monthly basis since the pandemic engulfed markets in March last year, and Treasury yields have surged

- China Evergrande Group’s debt crisis is making it harder for fellow real estate firms from the nation to sell dollar notes as borrowing costs soar

- Mainland developers with junk-level or no credit ratings have sold $6.43 billion of such notes since July began, down from $8.35 billion between April and June, marking the weakest showing since late 2017, according to Bloomberg-compiled data

- Two holders of a China Evergrande Group dollar bond with a coupon due Wednesday said they hadn’t received payment as of 8am Hong Kong time Thursday

- Evergrande owes $45.2 million in interest on the note due 2024, according to data compiled by Bloomberg

- There’s a 30-day grace period before any default could be declared

©2021 Bloomberg L.P.