Doom Postponed: Credit Is Merely Playing Catch-Up to Stocks

Doom Postponed: Credit Seen Merely Playing Catch-Up to Stocks

(Bloomberg) -- Lashed by trade wars, monetary angst and the tech wreck, besieged stock investors could be forgiven for seeing enemies wherever they look. Right now they’re fretting one that has a track record of presaging economic gloom.

But for all the mounting anguish over corporate bonds screaming a warning on growth, there’s scant evidence this is “the big one” for global markets, according to a string of investors and analysts. They argue credit is simply moving in sympathy with febrile sentiment in stocks, while default rates and risk premiums remain in check.

“We see this as a buying opportunity,” wrote Mark Holman, the chief executive officer of TwentyFour Asset Management, who is pouncing on the sell-off to add shorter-dated debt. “We don’t believe the end of the cycle is upon us just yet.”

That will be a welcome message for beleaguered equity markets, where investors have been navigating the fallout of higher rates, a correction in once red-hot technology shares and aggressive U.S. trade policies. The alternative -- a sustained debt move -- would be a reality check for Corporate America’s post-crisis debt binge, tightening broader financial conditions along the way.

Outlook Intact

Investment-grade bonds are now on track for their worst year since 2008, after spreads for companies with both the strongest and weakest balance sheets widened by the most since 2016 this week.

Yet U.S. growth remains above its longer-term trend and “spreads have widened only moderately,” Goldman Sachs Group Inc. analysts including Jan Hatzius wrote in a Nov. 20 note. And while absolute debt loads remain high, companies are still making more than enough money to service their debt.

“I don’t care how smart it sounds to say ‘credit is leading the way,’ ” Peter Tchir, head of macro strategy at Academy Securities, wrote in a note this week. “It just isn’t correct.”

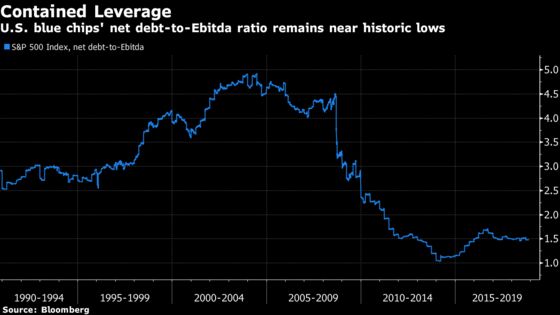

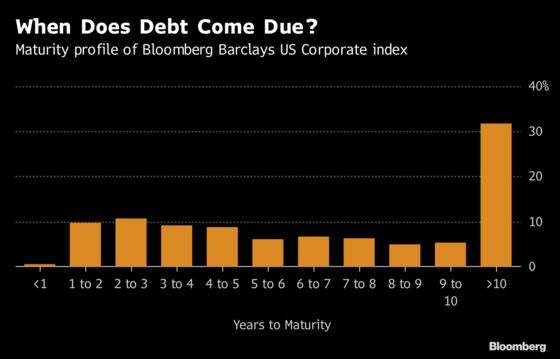

Instead, the take-away in this week’s market action may be more prosaic: That once-submissive credit buyers are finally telling Corporate America to rein-in its post-crisis debt binge. Companies have jumped on the post-crisis debt boom to term out debt, reducing refinancing risks in the near term.

The message echoes that of stock investors, who have punished the weak and rewarded the strong even as junk investors were happy with slim premiums. S&P 500 companies with healthy balance sheets have gained about 2.7 percent, compared with a loss of about 2.9 percent for companies with feeble financial ratios, according to baskets compiled by Goldman Sachs Group Inc.

Equities defied the recent turmoil on Wednesday, with the S&P 500 rising 0.9 percent as of 1:50 p.m. in New York.

‘Overdone’

U.S. junk bonds are now finally coming back to earth after risk premiums relative to their high-grade counterparts hit levels that recall the pre-crisis bubble and the peak in 1997. That’s another hint recent moves reflect the credit market playing catch-up -- rather than paving a bearish course for other risk assets.

The recent sell-off looks momentum-driven, rather than real-money investors placing bearish wagers with conviction. Macro traders who failed to get aboard the bearish bandwagon in time are likely selling corporate bonds this time around for fear of missing out, according to Tchir.

“I think momentum in all areas -- be it in credit, on the equity side -- has been the dominating trade,” Christian Hille of DWS Investment told Bloomberg TV. “We don’t see a recession, we see positive developments on the macro-economic side. This is to a certain extent overdone.”

Investor Angst

Barclays Plc also reckon risk premiums are widening in sympathy with stock volatility and a slew of local drivers, including the oil-price correction, the free-fall in General Electric Co. and drama over Brexit.

“We do not think they indicate a broad increase in contagion risk and rather view the events of the past month more as idiosyncratic risks that happen to be flaring up at the same time,” strategists Bradley Rogoff and Shobhit Guptawrote wrote in a recent note.

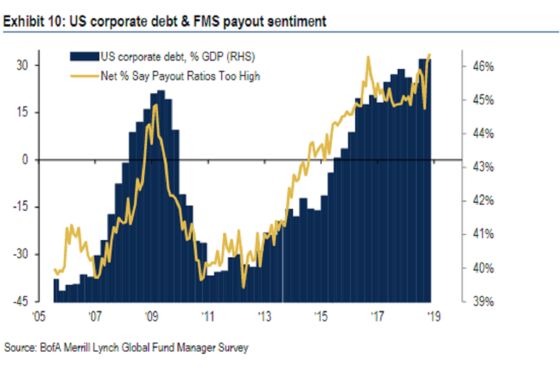

Another sign equity markets are driving fears about corporate balance sheets: Stock-investor angst that companies are saddled with excess leverage has risen to a post-crisis record in tandem with ballooning debt burdens, according to this month’s Bank of America Corp. survey of global fund managers with a combined $513 billion.

The equity market worries over corporate leverage may be a blessing in disguise for debt investors, if treasurers use excess cash flows to beef up balance sheets at the expense of dividends and buybacks.

All the same, it may be hard to shake the fear. The so-called smart money invested in high yield has historically provided a reliable barometer on prospects for a slowdown, suggesting investors who dismiss signals from the asset class do so at their peril.

“Credit and equities are caught together in a vicious cycle,” said Geof Marshall, who oversees C$40 billion ($30 billion) of assets at CI Investments’ Signature Global Asset Management in Toronto. “Higher spreads, volatility and poor sentiment all drive financial conditions tighter which will slow economic growth and impact corporate earnings, which will eventually lift the default rate.”

--With assistance from Tasos Vossos and Sebastian Boyd.

To contact the reporters on this story: Samuel Potter in London at spotter33@bloomberg.net;Sid Verma in London at sverma100@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Cecile Gutscher

©2018 Bloomberg L.P.