Death of the Hedge Fund Has Been Greatly Exaggerated

Death of the Hedge Fund Has Been Greatly Exaggerated

(Bloomberg Opinion) -- Philippe Jabre’s plans to close three funds he personally oversees seems like an ominous omen for the $3 trillion hedge fund industry. Look more closely, and what’s happening is a Darwinian thinning of the herd. But that’s as much to do with fewer launches as it is with liquidations.

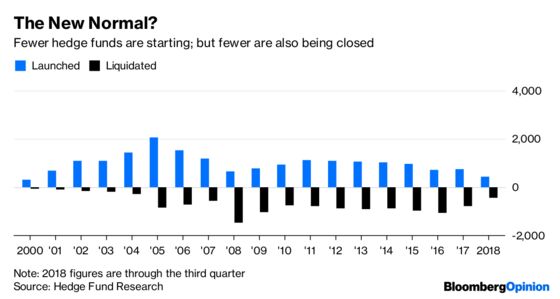

As the chart below shows, the number of new hedge funds starting this year is set to be at its lowest in about 18 years — if the trend of the first three quarters is repeated in the fourth.

As the industry has matured and the regulatory environment has become more vigilant, the cost of setting up shop has risen. Only truly outstanding managers with a strong track record can garner enough seed capital to start up in the first place. The economies of scale are acting as gatekeepers to keep out the riffraff.

Meanwhile, despite the recent run of big-name exits like Jabre, the number of firms giving up the ghost is also declining. Liquidations this year are on target to be at their lowest level this decade. This suggests that investors who have allocated capital to hedge funds are becoming more willing to weather periods of lackluster performance. While Hedge Fund Research’s Global Hedge Fund index is down about 6 percent this year — matching the decline in the MSCI World Index — there’s hope that more volatile markets in 2019 will create a trading environment conducive to managers who can generate alpha.

Indeed, there are still some industry names out there who are putting plans in place for the expected improvement in climate. Martin Taylor, who shut his $1.5 billion Nevsky Capital fund almost three years ago, plans to reopen for business next year as Crake Asset Management.

After delivering returns of more than 6,400 percent for investors in the two decades through 2015, Taylor got out after saying that the rise of computer-driven trading and geopolitical risks could produce “erroneous” market trends “which could then persist for far longer than we could take the pain.” In September, though, he announced plans to return. “There are ever fewer active participants to ensure price discovery,” he said. “There will be more opportunities for those active funds that remain.”

Elsewhere, Dharmesh Maniyar is spinning out his macro hedge fund from Tudor Investment Corp., and will start with more than $500 million of assets, Bloomberg News reported this week. The fund returned 3 percent in November, helping boost returns for the year through last week to 16 percent.

The catalog of funds closing or becoming family offices this year is striking, as this list compiled by my colleagues at Bloomberg News shows, featuring a long list of market veterans including Leon Cooperman, T. Boone Pickens and Dmitry Balyasny. But don’t rush to write off the industry just yet.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.