Don't Be Fooled by Emerging-Market Comeback, Japan Fund Says

Emerging markets are recovering from a sullen 2018 that followed a dream run that took assets to multi-year highs.

(Bloomberg) -- Don’t be fooled into believing that the emerging-market rally fueled by a “patient” Federal Reserve will last throughout 2019.

Satoru Matsumoto, a fund manager at Japan’s Asset Management One Co., which oversees the equivalent of about $490 billion, said the economic slowdown in China followed by the U.S. amid trade tensions will weigh on assets.

While developing-nation stocks just completed their best month since March 2016, and currencies scored the biggest monthly gain in a year, only those that meet three key criteria -- solid growth, benign inflation and no significant political risks -- are worth chasing, he said. And that leaves him with countries such as Indonesia and Brazil.

“It’s going to be a year where you’ve got to be selective with your emerging-market bets,” Tokyo-based Matsumoto said in a phone interview. “A dovish Fed has given some leg to the recent emerging-market rally, but I don’t expect this to lead to the kind of Goldilocks environment we saw back in 2017.”

“Sure, the bears might have disappeared more, but I don’t think investors are going overweight aggressively,” he said.

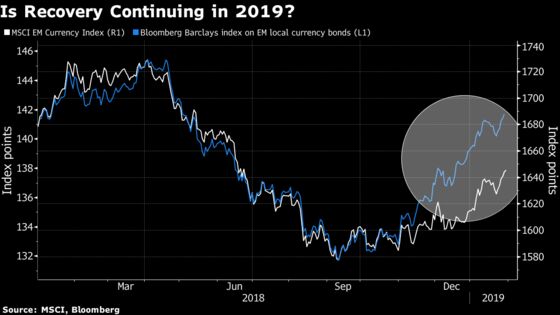

Emerging markets are recovering from a sullen 2018 that followed a dream run that took assets to multi-year highs. An MSCI index of developing-nation currencies gained 2.6 percent in January, while a measure of equities added 8.7 percent. The Bloomberg Barclays index of EM local currency bonds increased for a third month, rising 2.6 percent. The currency index fell 0.2 percent, while the equity measure declined 0.3 percent as of 2:34 p.m. in Singapore.

Below are other views Matsumoto shared in the interview the day after the Fed signaled it’s putting further rate hikes on hold:

Which markets are you most bullish in 2019?

- Matsumoto’s fund has been overweight on bonds and currencies of Brazil and Indonesia and plans to keep them.

- He’s is bullish on Indonesia because the economy will probably be able to sustain about 5 percent growth rate while inflation has been stable.

- Although Indonesia will hold an election in April, the current President Joko Widodo’s administration looks quite solid and political risks seem relatively low.

- The Fed may hike only once this year, giving some room for Bank Indonesia to cut its rate, so having an exposure to the rupiah and the bonds could be quite attractive.

- Indonesia has a current-account deficit, but the government and the central bank have worked to control the shortfall, such as by postponing some of the infrastructure projects.

- Brazil’s pension reform is where we’re focusing the most. While reforms may not come easy, we’re seeing signs that politicians are acknowledging the fact that they have to work on their fiscal conditions.

- Inflationary pressure in Brazil is not as strong as before, while the economy may continue to recover, which is a good combination for the currency.

Which markets are you bearish?

- His fund is underweight South Africa. China is its major trading partner and any slowdown in the Chinese economy would put a downward pressure on the African nation’s growth. With the risk of a credit downgrade, it makes it hard for the South African government to boost spending, therefore, options to support the economy may be limited.

- South Africa also faces political risks with elections scheduled for this year. The country’s current-account deficit isn’t decreasing even when the economic growth rate is low, and that makes the country vulnerable.

What is your view on India, which also will host an election?

- Matsumoto’s fund is underweight India as well, but only for the short term. The expectation is that Prime Minister Narendra Modi’s party is unlikely to get a majority by itself, and instead, it would be a coalition majority.

- Once the election is over, political risks would naturally ease; the economic growth rate remains high and inflation is low, which are all positive.

- We are temporarily reducing the exposure, but we eventually plan to bring our exposure back to at least neutral, or even to overweight.

To contact the reporter on this story: Yumi Teso in Bangkok at yteso1@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, Karl Lester M. Yap

©2019 Bloomberg L.P.