Junk Bond ETFs Are Again Defying Doubters and Liquidity Fear

Dogged by Liquidity Worries, Junk Bond ETFs Just Aced a Big Test

(Bloomberg) -- On a day when the whole world seemed to be jettisoning junk bonds, Geof Marshall had a plan to buy.

The idea was that, as exchange-traded funds struggled to keep up with a wave of redemptions spurred by crashing oil and coronavirus fears, he was going to swoop in and buy bonds from the ETFs on the cheap.

Despite submitting multiple bids, Marshall didn’t get many nibbles.

“Aggressive down bids are not necessarily being met by panicked offers,” said Marshall, chief of credit at Toronto-based CI Investments. In other words, his hoped-for fire sale never arrived.

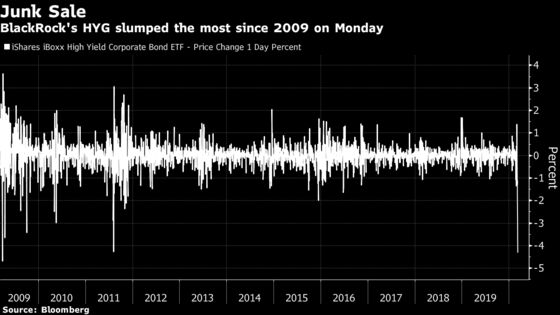

That was the welcome story across the ETF complex on Monday, as the biggest spread widening on a percentage basis for U.S. high-yield debt since 2001 did little to spur a cascade of redemptions in junk-bond funds. Despite claims that market makers were thin on the ground during the rout, the controversial products have once again defied naysayers warning of their imminent collapse.

“The ETFs have done much better than the underlying bonds,” said Mohit Bajaj, director of ETFs for WallachBeth Capital. “If you want to get in or out of HYG or JNK, the ETF held up.”

How well ETFs can survive a financial market downturn has spurred hand-wringing from regulators like the Financial Stability Board and Ireland’s central bank. The likes of Mohamed El-Erian of Allianz SE and Scott Minerd at Guggenheim Partners have suggested they could act as a potential destabilizing force in illiquid credit markets where they have an outsized trading share.

Monday’s session looked like a perfect storm. The prospect of an all-out price war in oil exacerbated market concern over the impact of the coronavirus on global growth, sending bid-offer spreads in the cash market as wide as 10 cents on the dollar.

But even on its worst-performing day since 2009, the iShares iBoxx High Yield Corporate Bond ETF, ticker HYG, traded 74 million shares and ended the session with a modest discount of half a percentage point to its net asset value. It actually added $409 million of inflows. The SPDR Bloomberg Barclays High Yield Bond fund, or JNK, ended the day with a chunkier 1.3 percentage point discount to net asset value, though that was only the largest since 2016.

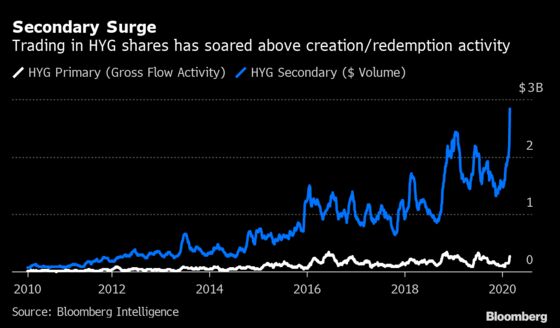

A major reason trading remained orderly was that virtually all of the action was happening in the secondary market, between buyers and sellers of ETF shares, according to Athanasios Psarofagis, an analyst at Bloomberg Intelligence.

“The way I see it, the behavior would have been the same even if the ETF didn’t exist,” said Psarofagis. “Now imagine it wasn’t here and all the transactions were on the primary. It could have been a messier situation.”

Trading in ETF shares, which acts as a liquidity valve in times of stress, has been soaring versus primary market activity, according to Bloomberg Intelligence. In February, the ratio for HYG jumped as high as 17-to-1. An active secondary market helps to keep the ETF itself relatively insulated from the mass redemptions that some say could pose problems.

Monday was “the first day that we’ve seen credit widen materially,” Nick Maroutsos at Janus Henderson said yesterday. “We haven’t seen any forced sellers or heard of any forced sellers yet.”

The fact that the ETFs are trading at modest discounts to their net asset value may even be a selling point. In a relatively illiquid market, the price of the fund may be the most accurate one the market has got.

“To the casual observer it might appear that they are trading at pretty steep discounts to NAV, but my opinion is that they are trading in line to where the actual underlying bonds will be trading either today or whenever the individual CUSIPS trade next,” said Will Wall, manager of trading and operations at Riverfront Investment Group.

“The ETFs tend to be the most accurate vehicle for price discovery in markets like this.”

To contact the reporters on this story: Cecile Gutscher in London at cgutscher@bloomberg.net;Claire Ballentine in New York at cballentine@bloomberg.net;Katherine Greifeld in New York at kgreifeld@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Yakob Peterseil

©2020 Bloomberg L.P.