Deutsche Bank Sees ‘Distressed Debt Cycle’ Starting in China

Amid rising defaults and tighter liquidity for Chinese privately-owned firms, the nation’s banks are letting some companies fail.

(Bloomberg) --

Amid rising defaults and tighter liquidity for Chinese privately-owned enterprises, the nation’s banks are letting some companies fail, something Deutsche Bank AG says presents bigger opportunities for foreign investors in troubled debt.

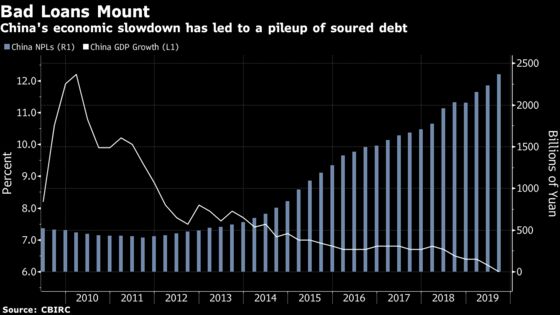

The German lender is an active distressed player in Asia Pacific and has bet on some of the biggest restructuring in the region, including commodities trader Noble Group Ltd. China is taking steps to allow more foreign investment into the country’s 2.37 trillion yuan ($344 billion) non-performing loan market. It will give U.S. investors direct access to the nation’s soured debt market as part of its trade deal.

“There are signs we are seeing the beginning of a distressed debt cycle in China,” said Amit Khattar, co-head of investment bank for Asia Pacific, in an interview. “Distressed debt in China is going to be really interesting.”

Read more: China further opens up soured loans market under trade deal

Defaults in China’s onshore corporate bond market hit a record in 2019 and troubles have continued in the offshore market as well this year. China state-backed Qinghai Provincial Investment Group Co. missed a coupon payment on a dollar bond due last week and there have been jitters over luxury clothing giant Shandong Ruyi Technology Group Co., whose unit missed payment on a loan facility last year.

During the global financial crisis, China distress “didn’t play out” because banks came to the rescue, but that isn’t happening at the same pace anymore as lenders refocus on asset quality and profitability, according to Khattar.

Soured Debt

China’s pile of bad debt is one area in which the firm potentially sees an opportunity. The nation’s asset management firms have dominated the market so far, but as defaults rise the pool of soured debt is increasing. Most of the onshore debt nonpayments have been for private companies.

“Traditionally, it’s been harder to buy secondary loans in China and we haven’t been particularly active in China NPLs,” said Khattar. “If the pace of distress creation goes up, then foreign firms will have a greater role to play.”

Deutsche Bank has also been active in India, its other main market for financing and distressed business in the region. It has deployed a “significant amount of capital” in India’s shadow banking sector and sees a strong “risk-reward” from lending to stressed companies, according to Khattar.

However, there have also been surprises for foreign investors, notably a court ruling last year on recovering funds in relation to Essar Steel India Ltd., one of the country’s so-called Dirty Dozen that were pushed into bankruptcy courts in 2017. That was resolved late last year, and the pace of distressed activity is likely to pick up with that, though there have been delays, Khattar said.

“The India bankruptcy process is highly complex and resolutions have been slower than expected,” said Khattar.

To contact the reporter on this story: Denise Wee in Hong Kong at dwee10@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum, Neha D'silva

©2020 Bloomberg L.P.