Desperate Need for Yield Pushes Investors Into Frontier Debt

Desperate Need for Yield Pushes Investors Into Frontier Markets

(Bloomberg) -- It says a lot about the state of global financial markets when countries such as Ghana, Senegal and even Belarus are being touted as the best places for investors to pick up returns in 2021.

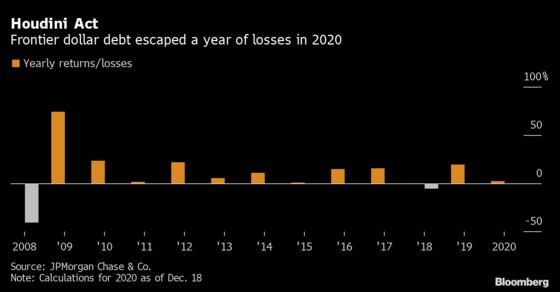

But, with the latest signal from the Federal Reserve that U.S. rates will stay lower for longer, the highest-yielding -- and riskiest -- corners of the world’s bond markets are being tipped as a top investment choice for the coming year. And this, after likely clocking up their smallest annual gain in five years.

The willingness of bond-buyers to move up the risk ladder would underscore how rising U.S. Treasury rates will do little to dim the appeal of developing-nation debt as long as an $18 trillion pile of negative-yielding debt hangs over markets and central banks remain accommodative. Even among developing economies, spreads on bonds from lower-risk borrowers have narrowed so much that investors are being forced to go further into junk territory for better returns.

“It’s a matter of time before investment-grade markets run out of spread,” said Leo Hu, lead fund manager for frontier-market debt at NN Investment Partners in Singapore. “The next one they can look at is indeed frontier markets. There is nowhere they can invest to get decent yields.”

Listen to a podcast on the topic, here.

The recovery may already be under way. JPMorgan Chase & Co.’s Next Generation Markets Index, which tracks the sovereign dollar debt of countries seen as emerging economies of the future, has rebounded to pre-Covid levels. The gauge, which includes the likes of Belize and Angola, is near the highest price since March relative to the mainstream emerging-market index, which is already at a record.

By removing the prospect that massive easing will be wound back anytime soon, U.S. policy makers meeting last week gave developing nations the breathing space to cut interest rates, or at least keep them lower for longer, at a time when Treasury yields are rising at their fastest pace in four years.

The external environment is turning conducive for frontier-market debt, too. Joe Biden’s U.S. presidential win has reduced risks to global trade, while the roll-out of vaccines has brought a global economic recovery nearer. That makes bond buyers confident enough to embrace next-generation markets where yields average about 7%, compared with the 4.4% average rates from emerging markets.

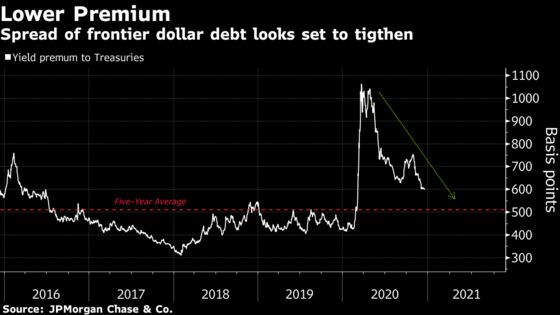

For NN Investment’s Hu, the combination of yield and market gains will hand investors in frontier-market bond returns of about 13% in 2021. The average frontier risk spread -- currently 600 basis points -- may tighten by about 100 basis points in the first half alone, he said.

The hunt for yield means investors putting money in some of the remotest corners of the world’s bond markets. Investors are touting Belarus, which was this year slapped with sanctions by the European Union as a result of President Alexander Lukashenko’s crackdown on protesters following the country’s disputed election in August. Senegal, among the low-income nations in Africa that got a waiver on bilateral debt payments, is also being touted by Aberdeen Standard Investments among others. Ghana, the world’s second-largest cocoa producer, also has its backers despite political turmoil after the Dec. 7 elections.

Belarus’s 2030 dollar bonds yield about 6%, Senegal’s 2033 bonds at about 5%, while Ghana’s 2032 notes is at 7.3%, according to data compiled by Bloomberg.

Below are some money managers’ trend-spotting and best picks for 2021:

Bryan Carter, head of global emerging markets debt at HSBC Global Asset Management in London:

- “2021 will likely be an inequitable year for emerging markets, with the rollout of the vaccine spurring strong economic recovery in many regions, but a large portion of the world could still be living with challenges we’ve seen in 2020.”

- “Secondary to the health care crisis is a debt crisis. Many frontier markets required some financing to fund their 2020 fiscal deficits. It is not yet clear how this level of financing can be repeated in another large deficit year. We could expect many debt restructurings to happen again in 2021.”

- HSBC Global prefers those frontier markets on the path to a ratings upgrade and is overweight on Ukraine, Egypt and Dominican Republic in both hard and local currencies.

- “We generally found the frontier markets unattractive entering this year, due to a combination of fundamentals and valuations. Post Covid, we see much more interesting valuations.”

Kevin Daly, investment director for emerging-market debt at Aberdeen Standard in London:

- “We are expecting to see continued inflows into emerging markets amid a low global yield environment, which should bode well for the high-yield component of the asset class.“

- “While there’s a risk of further frontier defaults in 2021, most low-income countries now have access to the Eurobond market, which will reduce default risk over the next year.”

- Good value is seen in African hard currency debt such as Kenya, Nigeria, Ivory Coast and Senegal.

- He sees default risk in Angola over the next several years lower than what the ratings imply because the nation has been given some breathing room with the debt relief from China.

- Ghana also offers an attractive return potential albeit with a higher risk profile than Kenya and Nigeria.

- He’s also been adding Belarus in his portfolio amid the election noise given its moderate debt level and manageable financing needs in 2021.

Jean-Charles Sambor, head of emerging markets debt at BNP Paribas Asset Management in London:

- “2021 will be a year of bottom-up alpha opportunities while 2020 was a beta year on the way down and on the way up. Many frontier markets have high public debt and external debt levels. Some of them might have to restructure their debt. The G-20 initiative might not be enough in itself. Deep dives on debt sustainability will be key.”

- “We are reasonably constructive on Sri Lanka. We think that policy makers are willing to keep good relations with bondholders and willingness to pay is strong.”

- In Africa, we are still constructive on Ghana, Senegal and Ivory Coast. Fiscal stance is relatively weak but likely to improve next year.

- The company also see some opportunities in small central American countries. Dominican Republic should benefit from the tourism recovery and Suriname is attractive at this level.

NN Investment’s Leo Hu:

- “We have seen decent interest since especially the vaccine news” on the company’s dedicated frontier fund.

- Within the frontier market, we normally like the credits with a reform story, or the credit with an IMF program. For example, we like Egypt and Ukraine.

©2020 Bloomberg L.P.