Derivatives Are Replacing Bonds as Some Fund Managers’ New Hedge

Derivatives Are Replacing Bonds as Some Fund Managers’ New Hedge

(Bloomberg) -- Derivatives helped trigger some of the most disastrous episodes in the history of finance. Now risk-averse institutional investors are increasingly turning to them for protection amid a perilous time for global debt markets.

All manner of complex solutions, from put options to receiver swaptions, are gaining traction as a way to overcome the drawbacks of bonds as a hedge after debt failed to insulate portfolios at key moments last year. Throw in the glaring threat of fixed-income losses as the economy rebounds, and the likes of pensions, university endowments and sovereign wealth funds are tapping asset managers specializing in derivatives to help solve these woes.

Of course, options have long been used to insulate bond portfolios at the margins, but now they’re winning more backers as a small sliver of a large, diversified portfolio. About 60% of the $15 billion overseen by Ardea Investment Management involves derivatives-based strategies -- up from 10% three years ago -- and the firm is touting a strategy that uses interest-rate derivatives to generate returns. Capstone Investment Advisors has a way to use swaptions to counter the risk that yields drop back toward record lows. And Universa Investments promotes an approach that uses put options against the S&P 500 Index to help bypass bonds as a hedge.

There are plenty of risks to protect against right now. There’s been talk of a bubble in stocks, and global fixed income is getting punished as the reflation trade revs up. All in all, many managers who were already questioning the role of bonds in the traditional 60/40 approach to a balanced portfolio are now desperate enough to try something new.

“People used to rely on fixed income for hedging and yield, and right now it is potentially providing neither,” said Brandon Yarckin, chief operating officer of Universa. “If anything, bonds are more ‘risk’ than ‘risk mitigation.’ That’s why people are looking at derivatives.”

Even a roughly 20% gain over the past year for a model portfolio deploying the time-honored allocation of 60% stocks and 40% bonds has failed to head off the quest for fixed-income alternatives -- ranging from currencies and convertible bonds to utility shares, royalties and real estate investment trusts. Some even point to cryptocurrencies.

Derivatives are just another choice. Their purpose is to boost returns or limit losses when an underlying asset fails to perform -- taking up the role, to some extent, that bonds have typically played. While it remains to be seen whether they’re a prudent alternative, these tactics are mainly available to big, sophisticated investors. So, a far cry from the retail-driven speculative options frenzy that roiled equities in recent weeks.

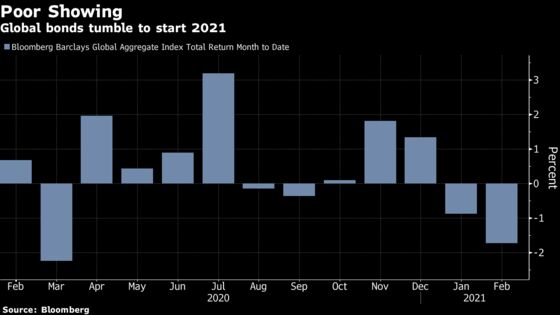

The key now is the growing debate about using bonds for diversification and income after 10-year Treasury yields reached a one-year high of 1.61% last month -- leaving some traders braced for even more pain. The ascent may have lured investors, but it produced mark-to-market losses for anyone already holding those securities at the start of the year.

“Investors really have to start preparing for the day, if they haven’t already, for when bonds are no longer protective enough,” said Jason Goldberg, a Los Angeles-based senior portfolio manager at Capstone. “The return on 60/40 last year was great. But do you want to invest through a rear-view mirror or do you want to be more forward thinking?”

The firm, which counts institutional investors as clients and built its business around global derivatives and volatility trading, has seen assets rise more than 40% since 2019, to $8.9 billion.

For the company’s advisory business, Goldberg recommends derivatives for 60/40 portfolios. Specifically, he says it makes sense for some to sell part of their fixed-income holdings and buy receiver swaptions, or an option on interest-rate swaps. It can pay off, for instance, in the event rates fall back below a specific level, meaning they act as a hedge for falling yields.

Skeptics Abound

Granted, skepticism abounds about derivatives as a substitute for the stability of bonds. After all, the instruments amplified the risk from subprime mortgages, and helped spur the crisis surrounding hedge fund Long-Term Capital Management in 1998. More recently, they’ve fueled turmoil for at least one U.S. mutual fund.

“In no way, shape, or form should options-based strategies alone be seen as acting as a ballast in a portfolio to balance the risk profile,” said Neil Azous, founder and chief investment officer of Rareview Capital in Las Vegas. Besides being risky and hard to execute, he says, derivatives fail to provide guaranteed income and “are just one of many possible solutions, none of which is a be-all-end-all.”

Azous says a better solution would be to move from nominal bonds into inflation-linked debt and commodities, or to combine a fixed-income strategy with closed-end funds to produce high income with measured risk. Rareview offers two exchange-traded funds that serve the latter purpose.

The good news is that regulators worked to make derivatives less dangerous after the 2008 financial crisis, making them more palatable for some investors.

‘Mindset Shift’

“We are seeing a mindset shift among even the most conservative investors,” said Gopi Karunakaran, Ardea’s Sydney-based co-chief investment officer. “Rather than simply grouping all derivative-based strategies under the same ‘highly risky’ label, more people are seeing them as effective risk-management tools.”

Ardea uses interest-rate derivatives in its most derivatives-heavy fund to generate returns while reducing volatility and correlation risks. One approach involves using short positions in interest-rate futures and swaps to neutralize the duration risk of holding certain government bonds.

Universa, in Miami, works with large institutional investors to provide a long-term alternative to the 60/40 approach, creating a strategy that allows more investment in stocks and other risk assets, by hedging with put options.

In that strategy, far out-of-the-money puts can often make up less than 3.3% of a portfolio to protect against a dramatic drop in the S&P 500 by a certain date, while the remainder stays in stocks. The derivatives cost a fraction of the potential returns and if the index rises instead of falls, the option simply expires.

Correlation Questions

Historically, bonds and stocks have been inversely correlated. But in times of market turmoil, that’s broken down: In March 2020, for example, there was a dual decline in stocks and Treasuries, in which 10-year yields soared amid a flight to cash.

On top of that, investment-grade corporate bonds also now offer leaner protection, with inflation-adjusted yields hovering at next to nothing. Investors have been turning to riskier debt, briefly pushing the average yield on junk bonds below 4%, a first.

Harvest Volatility Management’s Rick Selvala says his firm uses strategies that involve buying or selling of puts and calls on major equity indexes and related options to generate premium and incremental returns, while managing downside risk -- in much the way bonds would.

That need only grows “when the absolute sources of yield and the outlook for yields are so low,” said the New York-based chief executive.

©2021 Bloomberg L.P.