Currency Traders Finally Get a Whiff of Victory

The month of May ends on an unlikely happy note for the currency traders, how long would this happiness last?

(Bloomberg Opinion) -- Foreign-exchange traders are the market’s equivalent of the Gang That Couldn’t Shoot Straight. They have lost money in each of the past four years, and seven out of the eight, as measured by the Citi Parker Global Currency Index. The losing streak extended into 2019, with losses in each of the first four months. But with one trading day left in May, this month is shaping up to be one of the rare victories. Too bad it’s unlikely to last.

The Citi Parker Global Currency Index, which tracks nine distinct foreign-exchange investment styles, was up 1.09% for the month in late trading Thursday. To understand how rare a feat that is, consider that the index had a monthly gain exceeding 1% only four other times since the start of 2015. Traders have benefited from a few well-defined trends this month, including steady appreciation in the dollar and yen and a decline in the British pound and emerging-market currencies. What they didn’t benefit from was rising volatility, which generally provides greater opportunities to exploit wild market swings. Overall volatility in the foreign-exchange market as measured by a JPMorgan index is about the lowest since 2014. And that’s why May’s good results are unlikely to mark a turning point for long-suffering currency traders. With the global economy going from a synchronized recovery in 2018 to a synchronized slowdown this year, the main central banks have put a hold on their plans to normalize monetary policy. Even some Federal Reserve officials are talking about possibly cutting interest rates. This will likely continue to suppress volatility, depriving currency traders of a key ingredient for future gains since banking on the momentum in certain currencies to continue never ends well.

BOND TRADERS WAVER

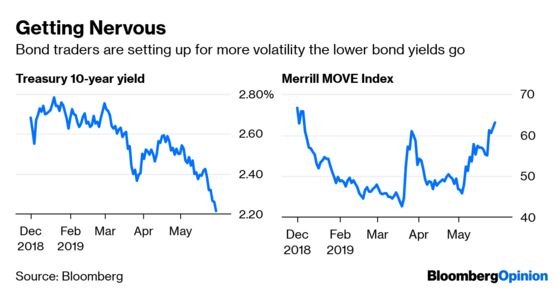

It’s only the end of May and already the world’s most important market is having its best year since 2014. The Bloomberg Barclays U.S. Treasury Index was up 1.71% this month through Wednesday, bringing its year-to-date gain to 3.57%. At 2.22% on Wednesday, the yield on the benchmark 10-year note is far below the 3.20% to 3.27% level that economists surveyed by Bloomberg News in December estimated it would be by now. In other words, the market has shocked. And it looks as if even bond traders are a little surprised, judging by Bank of America Corp.’s MOVE Index, which is a measure of anticipated implied volatility. The gauge rose this week to the highest since early January, which is not to be expected if bond traders had a lot of conviction in yields holding at these low levels for an extended period. About the only way yields at current levels make sense is if inflation continues to slow and the Fed cuts rates twice by the end of the year, as implied by money markets. While inflation is holding up its end, not everyone is ready to concede that the Fed will slash rates even once, even if it’s done as insurance against the possibility of deflation or even a recession. The rate cuts being priced in by the markets look “excessive” with the Fed signaling it’s preference to be “patient,”’ Citigroup economists wrote in a research note Thursday. “We do not believe in a monetary policy insurance cut.”

PIMCO VERSUS THE FED

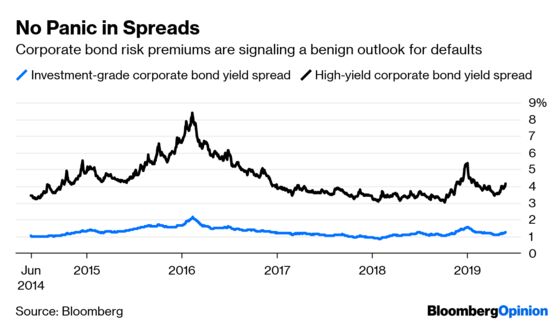

As one of the world’s biggest investors in fixed-income assets, when Pacific Investment Management Co. says something about the bond market it makes sense to pay attention. So it was this week when Scott Mather, the firm’s chief investment officer of U.S. core strategies, said in a Bloomberg Television interview on Wednesday that “we have probably the riskiest credit market that we have ever had.” History will determine the validity of that statement, but the Federal Reserve Bank of New York appears relatively sanguine about the risks. In a report Wednesday titled “Is There Too Much Business Debt?,” the central bank came up with plenty of metrics to show debt is not out of control. For one, although corporate debt as a percentage of GDP is a record 47%, it’s only 6% of all business profits, lower than during the 1980s and 1990s. Also, debt is 2.4 times cash flow, down from 3 times earlier in the recovery. Other metrics including debt to market capitalization, debt to book value and cash flow to interest expense are also benign. This helps to explain why relative yields on corporate bonds — which have widened this month as talk of an economic slowdown and possible recession have heated up — are still far below where they were during the market turmoil in December. “The Fed’s analysis is clearly meant to assuage concerns that corporate debt levels present a systemic risk,” DataTrek Research co-founder Nicholas Colas wrote in a note. But more important, Colas wrote, the report shows that the Fed “has painted itself into a bit of a corner. Corporate debt isn’t a problem as long as rates remain low and the U.S. economy continues to grow.”

OIL SEARCHES FOR A BOTTOM

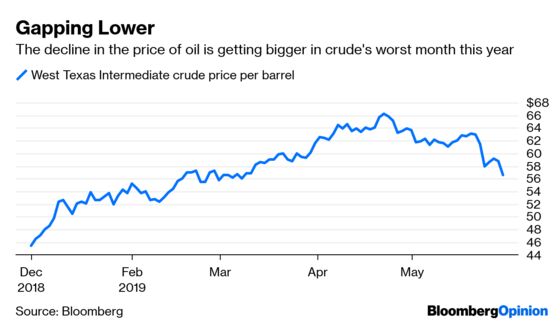

The market for crude is poised for its worst month since November, with futures tied to West Texas Intermediate oil dropping 11.7% this month. Prices dropped as low as $56.33 a barrel on Thursday after a smaller-than-expected withdrawal from U.S. storage facilities fueled worries that demand may be weakening faster than anticipated, according to Bloomberg News’s Alex Nussbaum. The obvious good news is that this should lead to lower gasoline prices, supporting consumers during the heaving summer driving season. But the obvious bad news is that corporate demand for oil is way down. As my Bloomberg Opinion colleague John Authers pointed out this week, shippers’ outlook for freight demand over the next six to 12 months has collapsed, falling to its lowest level since before 2012 as measured by Bank of America Merrill Lynch. At the same time, shippers’ view of available capacity is the highest since at least 2012. Put another way, truckers, railroads and others in the business of shipping goods have a lot of capacity to do just that, but scant customers. That’s not a good sign for the economy, let alone the oil markets. When it comes to oil, “the concern revolves around the demand side of the equation,” Nick Holmes, who helps oversee $16 billion in energy investments for Kansas-based money manager Tortoise, told Bloomberg News.

BITCOIN IS BACK

Escalating trade tensions on multiple fronts. A global synchronized slowdown. The worst sell-off in the stock market since December’s gut-wrenching slide. Clearly it’s a “risk off” environment — except cryptocurrency traders never received the memo. Bitcoin has put together an epic month, surging about 65% in May to mark its best performance in exactly two years and bringing its year-to-date gain to 135%. It briefly topped $9,000 on Thursday before easing back to about $8,650 in late trading (which is still a long way from the peak of almost $20,000 in December 2017). And it’s not just Bitcoin enjoying a renaissance. The Bloomberg Galaxy Crypto Index of various digital currencies is up 63% in May. It’s always almost impossible to clearly explain the moves in this market, but the performance this month will most likely have its backers talking up how it’s a new haven in times of turmoil. That may be going too far at this point, but the most high-profile investor in this market doesn’t see a pullback anytime soon. “On a go-forward basis, Bitcoin probably consolidates somewhere between $7,000 and $10,000,” billionaire investor Mike Novogratz, the chief executive officer of Galaxy Digital Holdings Ltd., said on a conference call Thursday discussing the company’s first-quarter financial results. “If I’m wrong on that, I think I’m wrong to the upside, that there’s enough excitement and momentum that it could carry through.”

TEA LEAVES

The U.S. government on Thursday revised down its estimate of gross domestic product growth in the first quarter to an annualized rate of 3.1% from 3.2%. On the surface, that’s a decent showing, especially for all the talk about an imminent slowdown. But the details provide plenty of reason for pause. As FTN Financial chief economist Chris Low noted, the headline number belied “the unrevised weak 1.3% rise in real private domestic final sales,” which is important because “this is the core of GDP, consisting of household and business consumption and investment, the driving force behind sustainable growth.” Market participants will get a sense of whether sales remained weak into the first month of the second quarter when the Commerce Department releases its report on April income and spending on Friday. The median estimate of economists surveyed by Bloomberg is that spending rose by just 0.2% after an unusually large 0.9% gain in March. Real spending, which takes into account inflation, is forecast to be flat.

DON’T MISS

Poker-Playing Hedge Fund Managers Have an Edge: Aaron Brown

Pimco Warns Central Banks Can’t Rescue Bonds: Brian Chappatta

We All Need to Calm Down About Rare Earths: David Fickling

Can We Stop Blaming the Trade War for Everything?: Daniel Moss

Introversion Makes Oil Companies Unpopular: Liam Denning

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.