Crude Prices Right Now Offer Binary Recession Bet

OPEC+ cuts and unexpected disruptions will cut 2019 oil supply.

(Bloomberg) -- A recipe for New Year crude oil price weakness:

Take 2 parts trade-war worries, 1 part each of quantitative tightening and fear of a slowdown in Chinese growth. Add a dollop of credit default concern and a generous pinch of European Union chaos, seasoned with a dash of Brexit uncertainty and Italian budgetary angst. Blend and allow to simmer gently for several months.

This stew of broader economic concerns has done more than oil market fundamentals to undermine crude prices since early October. Oil’s 9 percent surge on Wednesday only brings it back to around the same price level it was at for the start of the week. The supply-demand balance for oil does not appear to support the dramatic slump in prices since then, and there are plenty of reasons to expect crude supplies to fall in the coming weeks and months.

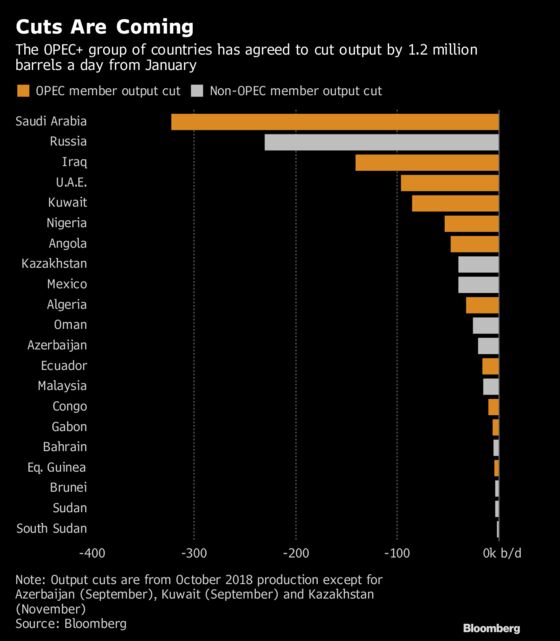

The OPEC+ group of oil-producing countries has pledged to remove about 1.2 million barrels a day from supply from January, with most countries using October 2018 as the baseline for their cuts. Expect them to do what they have pledged, even if it takes them a little time to get there.

Saudi Arabia has said it will cut output by even more than it promised, reducing supplies to 10.2 million barrels a day in January, compared with a a target of 10.31 million. That will more than make up for expected shortfalls from some other countries.

Add to that the likelihood of further declines from Venezuela, where oil production is still falling as a result of the exodus of workers and a lack of maintenance on essential infrastructure, and Iran, where sanctions will almost certainly be tightened when the current waivers expire in early May.

Then there is the possibility of a further downward drift in Angolan production -- new fields are no longer being brought into production fast enough to offset steep decline rates at deep-water offshore fields. There’s also potential for unexpected disruptions in Libya, Nigeria and Algeria, all of which are due to hold elections.

Even Kazakhstan, which was the biggest over-producer under the previous round of cuts, will find it easier to meet its commitment in 2019, having set the baseline for its cuts at it November level of 1.9 million barrels a day -- the most the Central Asian country has ever pumped.

Which brings us back to the economic stew that’s really driving this.

Bank of America Merrill Lynch published its last global fund manager survey for 2018 the week before Christmas. Its list of "tail risks" make up the ingredients for the recipe at the top of this article. Were one or more of those to disappear, global economic prospects could suddenly look a lot rosier.

In other words, what we have is an oil market that’s pricing in fear of recession rather than one that’s driven by an actual actual economic slump or supply surplus. If a recession were to happen, then that would obviously be very bearish. But if it didn’t, there would be reasons to be very bullish.

...

Note: Julian Lee is an oil strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

To contact the reporter on this story: Julian Lee in London at jlee1627@bloomberg.net

To contact the editors responsible for this story: Alaric Nightingale at anightingal1@bloomberg.net, Brian Wingfield

©2018 Bloomberg L.P.