Cross-Asset Volatility Surges at Fastest Pace Since 2008 Crisis

Cross-Asset Volatility Surges at Fastest Pace Since 2008 Crisis

(Bloomberg) -- The sell-off may be taking a rest but the volatility is still at work.

On Tuesday, S&P 500 futures hit their trading limits after rising too fast. A day earlier, stocks fell so quickly they also triggered curbs. The raging equity swings underscore how volatility is engulfing every region and asset class at a pace unseen since the dark days of the global crisis.

The Bank of America Merrill Lynch GFSI Market Risk indicator, a measure of expectations for turbulence in stocks, rates, currencies and commodities worldwide, hasn’t risen this fast since the collapse of Lehman Brothers.

The gauge has now surged to the highest since 2011 as investors grapple with the shock of an oil price war alongside the coronavirus outbreak.

It’s a roller coaster that looks set to continue. Equity futures are pointing to a huge jump at the open on Wall Street as assets of all stripes retrace Monday’s extreme moves.

“Implied volatility levels are a now at least in the vicinity of the other market shocks in the past decade,” according to Jim McCormick, the London-based global head of desk strategy at NatWest Markets. “The risk now is volatility remains around current levels as central banks’ abilities to suppress it is now much diminished.”

Here’s a look at the extreme gyrations across major assets:

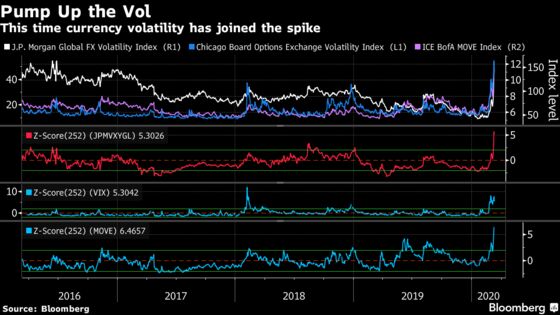

FX Calm Shatters

In a sign of how deep current macro fears run, spiking volatility is on display beyond just the equity or commodity markets. After years of relative calm, even as stocks endured various bouts of turbulence on trade wars or tightening monetary policy, the FX market is finally joining in.

A JPMorgan Chase & Co. index that uses options to measure expected price swings rose to the highest since 2016 on Monday, the biggest one-day net jump since 2008.

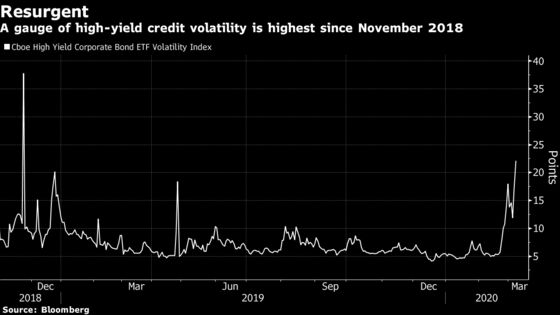

High Yield Warning

Even before it became clear Saudi Arabia and Russia were headed toward an all-out oil price war, credit markets were suffering. They recorded their worst day in a decade on Friday as the global spread of the virus raised concerns about companies’ ability to repay debt. That got worse on Monday as energy prices collapsed, heaping pressure on typically junk-rated issuers in the industry.

The Cboe High Yield Corporate Bond ETF Volatility Index has nearly trebled since Wednesday to the highest since November 2018.

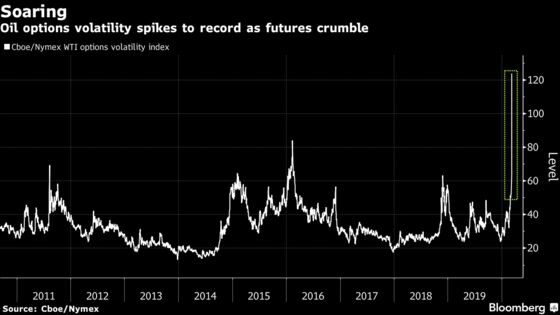

Epic Oil Swings

The biggest oil plunge since 1991 had traders paying up for options, particularly those covering against further price drops. The Cboe/Nymex Volatility index -- a measure of the cost for West Texas Intermediate crude options -- soared Monday to the highest level in data going back to 2010. Volume in Brent options reached a record high.

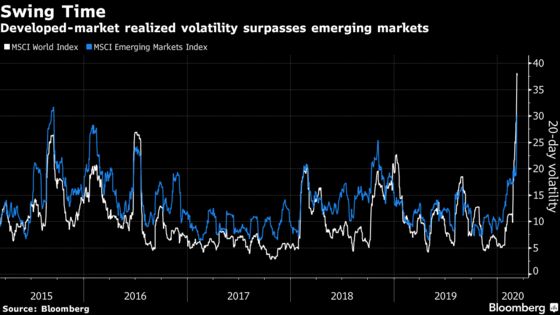

Developing Problem

The developed world is the epicenter of market stress. Realized volatility for developed-market stocks has outstripped that of their emerging-market peers. Typically the former is seen as more stable and lower risk.

On a 20-day basis, covering the bulk of the recent turmoil, the spread between the two this week hit the highest since 2008.

--With assistance from David Marino and Joanna Ossinger.

To contact the reporter on this story: Sam Potter in London at spotter33@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2020 Bloomberg L.P.