Credit World’s Top 2022 Play Is ‘Stock Picking’ as Risks Rev Up

Credit World’s Top 2022 Play Is ‘Stock Picking’ as Risks Rev Up

(Bloomberg) -- Credit investors are going to be picky about what they buy next year in expensive U.S. and European debt markets.

Amundi SA, Newton Investment Management Ltd., Western Asset Management and Vanguard Group Inc. are drilling down into balance sheets, looking at how companies make their money, gauging profit margins and weighing how well they can cope with rising interest rates and slowing global growth. And that’s in addition to stretched valuations, the prospect of fewer central-bank asset purchases and a new coronavirus strain the market knows little about.

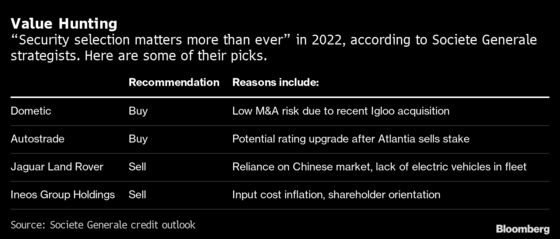

“Investors will need to do more stock picking,” said Gregoire Pesques, head of global credit at Amundi, Europe’s largest asset manager. “There’s less overall value in the market as a whole. But it’s also because specific risk is going to grow, so you’ll be more rewarded if you spend more time on name selection.”

As the Federal Reserve weighs removing pandemic support at a faster pace, companies have to “stand on their own fundamentals” for the valuations they command, said Arvind Narayanan, co-head of investment-grade credit at Vanguard, which oversees about $8.4 trillion globally. Narayanan and his team are singling out companies and industries best positioned to navigate supply-chain disruptions and inflation headwinds.

“It’s things like that that we are really spending a lot more of our time on,” Narayanan said.

It’s a shift from the past two years, where virtually all corners of credit rallied after central banks and governments stepped in to provide unprecedented support during the pandemic. But the vast stimulus unleashed to support economies following periodic lockdowns has fueled inflation. And the prospect of higher interest rates will push up borrowing costs, albeit from historic lows.

“There’s going to be divergence within credit, and within geographic regions,” said Paul Brain, head of fixed income at Newton Investment Management. “Credit analysts are really earning their salaries now.”

Next Chapter

Another area of focus is capital expenditures, which are booming as firms dip into the war chests they accrued earlier in the pandemic, according to Bank of America Corp. strategists, led by Barnaby Martin.

In a research note dated Nov. 12, the strategists recommended buying the debt of companies that spend heavily in areas promising sustainable, high-quality, top-line growth. Transport, tech and retail are among the sectors with the strongest year-on-year capex growth, according to their analysis. But the same sectors are also grappling with supply-chain bottlenecks, underlining the need to be selective.

Another is deal-making, which can have mixed outcomes for bondholders, according to Western Asset Management’s head of non-U.S. credit, Annabel Rudebeck. Case in point: the bonds of Telecom Italia SpA and U.K retailer Marks & Spencer Group Plc dropped last month on reports of private equity buyouts, since this can saddle companies with more debt.

Rates Risk

Until recently, the vast pandemic-era stimulus has served as a lifeline supporting the weakest companies. An extension of that support, should the pandemic enter a dangerous new chapter, could foster another broad-based rally. That would make being selective when buying bonds less vital.

Even with a new virus strain spreading globally, Federal Reserve Chair Jerome Powell said last week that asset purchases could end sooner than planned given inflation. And should central banks ease monetary stimulus, companies that have weathered price pressures so far may start to see their margins sag in 2022.

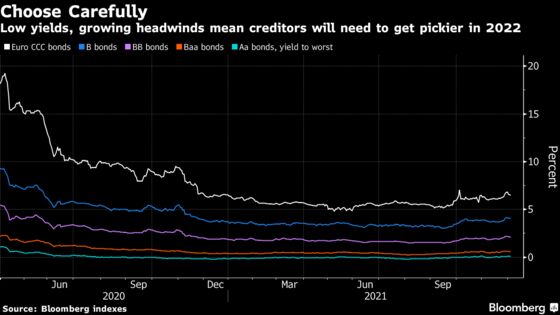

“Jump forward to the middle of next year, you’ll have tightening of monetary conditions at a time of higher costs,” Newton Investment’s Brain said, adding that one of the gaps that may open up is between CCC rated bonds, the lowest rung of junk, and BB rated bonds if default rates start to creep higher. “Credit markets may start to have a serious wobble at that point.”

‘Smart and Short’

But backing the right companies isn’t enough: investors will also need to look out for the right debt structures, said Gina Germano, head of high-yield bonds and syndicated loan investments at Hayfin Capital Management.

Inflation and central-bank tightening concerns make floating-rate instruments such as leveraged loans and collateralized loan obligations attractive, she said.

Investors can also significantly reduce duration risk by picking notes that benefit most from roll-down, the natural spread compression that occurs as bonds approach maturity, said TwentyFour Asset Management portfolio manager Pierre Beniguel. Three-to-five-year bonds will tend to offer the best gains as the short end of the curve steepens, so long as they provide enough spread to absorb anticipated rate rises.

The bottom line is that “2021 hasn’t exactly been the hardest year to be a credit analyst,” said Beniguel. “Credit exposure should be smart and short in 2022.”

Elsewhere in credit markets:

Americas

Merck & Co. started marketing a jumbo U.S. high-grade corporate debt sale on Tuesday to help fund the $11.5 billion acquisition of Acceleron Pharma Inc. Five other borrower are also looking to sell, including JPMorgan Chase & Co. and Mexico’s state oil giant Petroleos Mexicanos

- U.S. dollar high-yield bond issuance may be pared by a third next year, Bloomberg Intelligence’s Noel Hebert writes in a Tuesday note. Sales may slow toward $350 billion gross ($125 billion net) -- plus or minus $25 billion -- as rising rates favor floating-rate funding and change the economics of early redemptions. M&A should see some retracement, alongside refinancing, with the average coupon at a record low of 5.67% and the share of actively callable debt lower

- The cost of credit default swap index options has increased sharply during the recent bout of volatility, JPMorgan strategists wrote Tuesday. “The most notable increase in option costs was seen for out-of-the-money put options,” strategists led by Eric Beinstein wrote

EMEA

Orange SA, Canadian Imperial Bank of Commerce and Westpac Securities NZ offered bonds on Tuesday. Monday’s deals got a strong reception, including the first euro non-financial high-grade corporate sale since Nov. 25, from Nippon Telegraph & Telephone.

- Euro high yield has had a decent 2021 with 2.8% total returns; Bloomberg Intelligence strategists including Mahesh Bhimalingam expect 2022 to be below that, yet positive, at just above 2%, according to their outlook for next year

- European Central Bank Governing Council member Robert Holzmann supports decoupling any decision to increase interest rates from the institution’s use of asset purchases, according to an interview with Handelsblatt

- Volkswagen AG signed its first loan linked to sustainability goals, a 1.8 billion-euro ($2 billion) facility meant to help fund projects to reduce the German industrial giant’s carbon footprint

Asia

Some China Evergrande Group bondholders had yet to receive overdue coupon payments by the end of a month-long grace period, signaling a possible default by the developer as it prepares for one of China’s largest-ever debt restructurings.

- A group of Kaisa Group bondholders have sent the beleaguered property firm a formal forbearance proposal, which may buy some time and help it avoid a default on $400 million dollar bonds due Tuesday

- More Chinese developers are at risk of defaulting due to a liquidity crunch despite recent measures by the authorities to free up some funds, according to S&P Global Ratings

- As Chinese economic policy makers shift toward easing mode, the question on traders’ minds is how far the government is prepared to go

©2021 Bloomberg L.P.