Credit Set for Worst Year Since 2008 as Crashes Roil Market

Credit markets are set for the worst year since the global financial crisis as investors abandon hope of a late-2018 rally.

(Bloomberg) -- Credit markets are set for the worst year since the global financial crisis as investors abandon hope of a late-2018 rally.

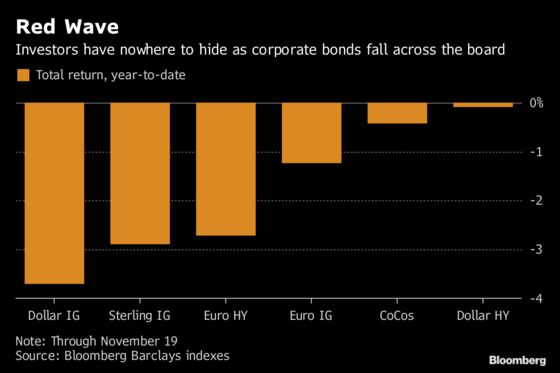

High-yield and investment-grade notes are headed for losses in both euros and dollars, the first time all four asset classes have posted negative total returns since 2008, based on Bloomberg Barclays indexes. It’s been a exceptionally volatile month, with headlines on companies including CMC di Ravenna SC and Nyrstar NV triggering the biggest weekly jump in euro high-yield spreads in almost seven years, while dollar investment-grade spreads are at a two-year high amid a sell-off triggered by General Electric Co.’s woes.

“Most people have buried hopes for a year-end rally,” Marco Stoeckle, head of corporate credit strategy at Commerzbank AG, said in a telephone interview. “This whole defensive mindset is rather entrenched.”

November’s string of blow-ups, also including the arrest of Renault-Nissan head Carlos Ghosn and a slump in Vallourec SA notes, has unnerved credit markets that are also adjusting to higher U.S. borrowing costs and the looming end of European Central Bank stimulus measures. Investors are switching focus toward avoiding losses rather than chasing yields, with high-grade fund managers paying greater attention to individual companies’ financial health rather than riskier notes that helped boost returns last year.

The credit rout, which extends to sterling notes and high-coupon contingent-capital bank bonds, has particularly hit dollar investors as they have suffered wider spreads and higher Treasury yields. U.S. investment-grade bonds have posted negative total returns of 3.71 percent in 2018, compared to a 2.9 percent loss in sterling and 1.2 percent in euro, according to Bloomberg Barclays indexes.

“Investors have to go back home -- back to their benchmark -- by removing some of the tourist money,” said Mohammed Kazmi, portfolio manager at Union Bancaire Privee SA in Geneva. “This is having a big impact on the market, especially as liquidity is drying up near the end of the year.”

Credit default-swaps tied to European high-yield corporate bonds are also on the worst run since 2011, with the Markit iTraxx Europe Crossover index widening for a ninth day on Tuesday. The gauge has reached the highest in almost two years at more than 330 basis points.

| Issue (all bonds in EUR) | Nov. price drop | Reason |

|---|---|---|

| CMC di Ravenna 6% 2023 | -66.3% | Not paying coupons on the bond |

| Vallourec 6.375% 2023 | -29.1% | 3Q cash outflow |

| Nyrstar 6.875% 2024 | -25% | Debt restructuring speculation |

| GE 1.25% 2023 | -7.7% | Sudden loss of investor confidence |

| Barclays 1.5% 2023 | -1.7% | Concerns about May’s Brexit deal |

| Renault 0.5% 2023 | -1.5% | CEO Carlos Ghosn arrested in Japan |

Central Banks

Central banks could provide some support if bad economic news forces a policy rethink. U.S. Federal Reserve Vice Chairman Richard Clarida has noted “some evidence” of slowing global growth, suggesting he doesn’t favor aggressive rate hikes. In the U.K., interest rates may depend on how the country manages its departure from the European Union.

The ECB should also remain very “pragmatic” and be able to adapt its monetary policy to economic data, Banque de France Governor Francois Villeroy de Galhau said Monday in Tokyo. It should only reduce the pace of reinvestments from bond holdings after a rate increase, even if new purchases will “very probably” end in December, he said.

Still, with net asset purchases likely to finish, bondholders and borrowers will be more focused on individual names rather than second-guessing central bankers and surfing marketwide gains.

“There will be a bit more differentiation between companies and they’ll be more incentivized to protect their ratings,” said Gordon Shannon, portfolio manager at TwentyFour Asset Management, which oversees 14 billion pounds ($18 billion).

To contact the reporter on this story: Tasos Vossos in London at tvossos@bloomberg.net

To contact the editors responsible for this story: Hannah Benjamin at hbenjamin1@bloomberg.net, Neil Denslow

©2018 Bloomberg L.P.