Credit Markets Ignore Equity Rally With Fear Gauges Flashing Red

Credit Markets Ignore Equity Rally With Fear Gauges Flashing Red

(Bloomberg) -- Need a reason to stay cautious? Look no further than the credit markets.

Measures of investor fear in the U.S. investment-grade and high-yield corporate bond markets shrugged off the rally in stocks Monday amid another session marked by pulled loans and little new-issue activity.

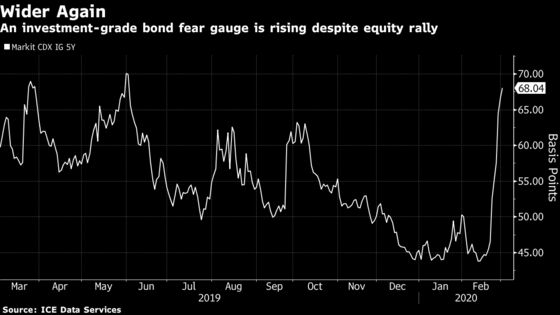

The cost to protect a basket of blue-chip securities in the credit default swaps market rose for an eighth day to about 67.9 basis points, according to ICE Data Services. A similar index for speculative-grade debt, which trades on price, was also in the red much of the day while the S&P 500 jumped as much as 2.9%.

The divergence underscores bond buyers’ continued caution in a corner of the market that many investors say still looks expensive. Risk premiums in the investment-grade corporate credit market jumped the most since the financial crisis on a percentage basis last week, but still offer just 1.22 percentage points of pickup over Treasuries.

“The investment-grade market is being very conservative around how it looks at and prices risk,” said Lon Erickson, a portfolio manager at Thornburg Investment Management. “We’re not wholeheartedly jumping in right now.”

The U.S. investment-grade new-issue market was shut again Monday, extending a week-long issuance drought. Outside of typical August and December seasonal slowdowns, it was the first week with no new deals since July 2018. Investors yanked a record $2.02 billion from the largest exchange-traded high-grade bond fund in the five days through Friday.

In the high-yield market, Cleveland-Cliffs Inc. is the sole issuer testing the waters after making structural tweaks to appeal to more investors. New leveraged loans have also struggled. PPD Inc. postponed a planned $4.1 billion sale, following a decision from Bausch Health Cos. to delay an $8 billion financing package last week. Risky loans lost 1.3% in February for their worst showing since December 2018.

UBS Group AG analysts led by Stephen Caprio wrote in a note Monday that there are reasons to be cautious.

A “severe virus with persistently high reinfection rates” hasn’t been ruled out yet, and could drive U.S. high-yield defaults north of 5%.

So far, much of the pain in the junk bonds has come from energy companies. That debt has sunk more than 6% in the past week, compared with the broader market’s 2.6% drop.

“We expect a very volatile path ahead, but would not panic,” the analysts wrote.

Read more: Corporate bond sale freeze unswayed by central bank support

BlackRock Inc. is also turning more careful toward credit. The world’s largest asset manager said in a note Monday that it was cutting its view on corporate debt worldwide to neutral from overweight and is “on the lookout for any signs of a liquidity crunch or deterioration in financial conditions.”

Investors uncertain about the ultimate impact of the virus are waiting for more economic and earnings data, said Nichole Hammond, a senior portfolio manager at Angel Oak Capital Advisors.

“The market is looking for some stability in equities, especially for high yield,” Hammond said. “Risk markets have calmed down from last week, but there is still a fair amount of uncertainty over what this actually means for the global economy over the coming quarters.”

--With assistance from Olivia Raimonde and Paula Seligson.

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Boris Korby, Christopher DeReza

©2020 Bloomberg L.P.